Table of Content

Summary

A legal shield for every capital raise

A PPM discloses terms, risks, and management details to prospective investors in a private securities offering. It protects the company if the deal goes sideways.

[01]

Securities laws apply from dollar one

You need a PPM whenever you sell securities, even to friends and family. The $500K handshake round is where most legal problems start.

[02]

Professional drafting costs $15K to $75K+

Skipping proper counsel or using a cheap template leads to rescission exposure, personal liability, and cleanups that cost multiples more.

[03]

506(b) vs 506(c) determines everything

Most private placements use Regulation D. Choosing the wrong exemption path can invalidate the entire offering. Decide before drafting.

[04]

The INVEST Act could widen investor access

Passed by the House in December 2025, the bill adds an exam-based pathway to accredited investor status, potentially expanding the pool of eligible capital.

[05]

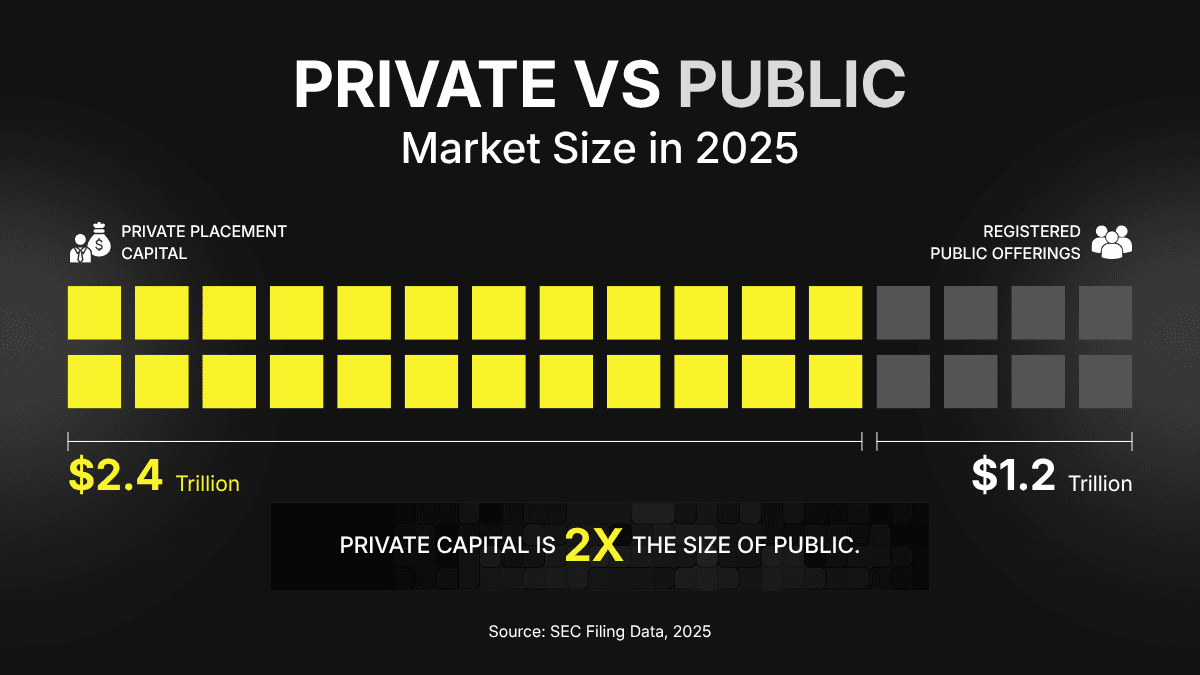

The private placement market is now larger than the public securities market. When more capital flows through private channels than public ones, every transaction carries more scrutiny, more regulatory attention, and more legal exposure, which means the documentation behind each deal matters more than it ever has.

In 2025, 34,553 Regulation D offerings raised $2.4 trillion in capital, according to SEC filing data. Registered public offerings raised roughly $1.2 trillion in the same period. Private capital didn't just catch up to public markets. It left them behind.

And at the center of almost every one of those transactions sits one document: the private placement memorandum.

I work on private placements regularly. At spectup, we structure capital raises for companies and funds raising $2M to $50M+. That means I see PPMs from every angle: the companies drafting them for the first time, the fund managers updating them for a second vintage, and the investors pulling them apart during due diligence. The patterns of what works and what kills deals repeat with alarming consistency.

Key terms you should know

Private placements come with their own vocabulary. Before we get into the details, here are the terms that will keep coming up throughout this guide.

PPM: Private Placement Memorandum, the legal disclosure document given to prospective investors in a private securities offering.

Regulation D: The SEC framework that exempts private placements from full registration requirements. Most private capital raises use Rule 506(b) or 506(c).

Accredited Investor: An individual with income above $200,000 ($300,000 with spouse) or net worth above $1 million excluding primary residence. Also includes certain licensed professionals and entities.

Form D: The SEC notice filing required within 15 days of the first sale of securities in a Regulation D offering.

Rescission: An investor's legal right to demand a full refund if the offering violated securities laws or contained material misrepresentations.

General Solicitation: Public advertising or marketing of a securities offering. Allowed under Rule 506(c), prohibited under Rule 506(b).

Why private placements matter more in 2026 than any year before?

The Fed is holding rates at 3.5% to 3.75% with only one cut projected for the rest of 2026. LP selectivity is rising even as headline fundraising numbers look strong.

Q1 2026 M&A hit a record $813.3 billion in deal value, but deal volume fell, creating a K-shaped recovery where mega-deals dominate and mid-market companies fight for attention.

What does this have to do with your PPM?

Everything.

When capital is abundant and cheap, investors write checks fast and ask fewer questions.

When rates are higher, exits are harder, and LP pressure is building, investors slow down.

They read documents more carefully. They send their counsel through your offering materials line by line. The scrutiny on private placement memorandums is higher now than at any point since 2022.

I've watched this shift in real time. A biotech client of ours started their $15M raise in late 2025. In the first three months, investor meetings moved quickly and diligence was light. By February 2026, after the Iran conflict pushed oil past $120 a barrel and the Fed signaled one cut instead of two, the same investors started requesting updated risk factors, stress-tested financial models, and revised use-of-proceeds sections. The PPM went from a document they skimmed to the document they scrutinized.

The days of investors glancing at a PPM and wiring money are over. In this rate environment, your offering documents are doing more work than your pitch deck. Act accordingly.

That shift creates a problem for companies that treated documentation as an afterthought. But it's also an opportunity for companies that get it right, because most of the competition still doesn't.

What is a private placement memorandum, and why does it exist?

Last month, a founder called me in a panic. His angel investor's attorney had sent a letter requesting the subscription agreement from a $1.2M friends-and-family round closed eighteen months earlier.

There wasn't one. There wasn't a PPM either.

The founder had raised on handshakes and term sheets, assuming that because everyone knew each other, the formalities didn't matter.

Now they did. The investor wanted out, and the founder had no documentation establishing the terms, the risks disclosed, or the investor's acknowledgement of those risks.

That's what a private placement memorandum prevents.

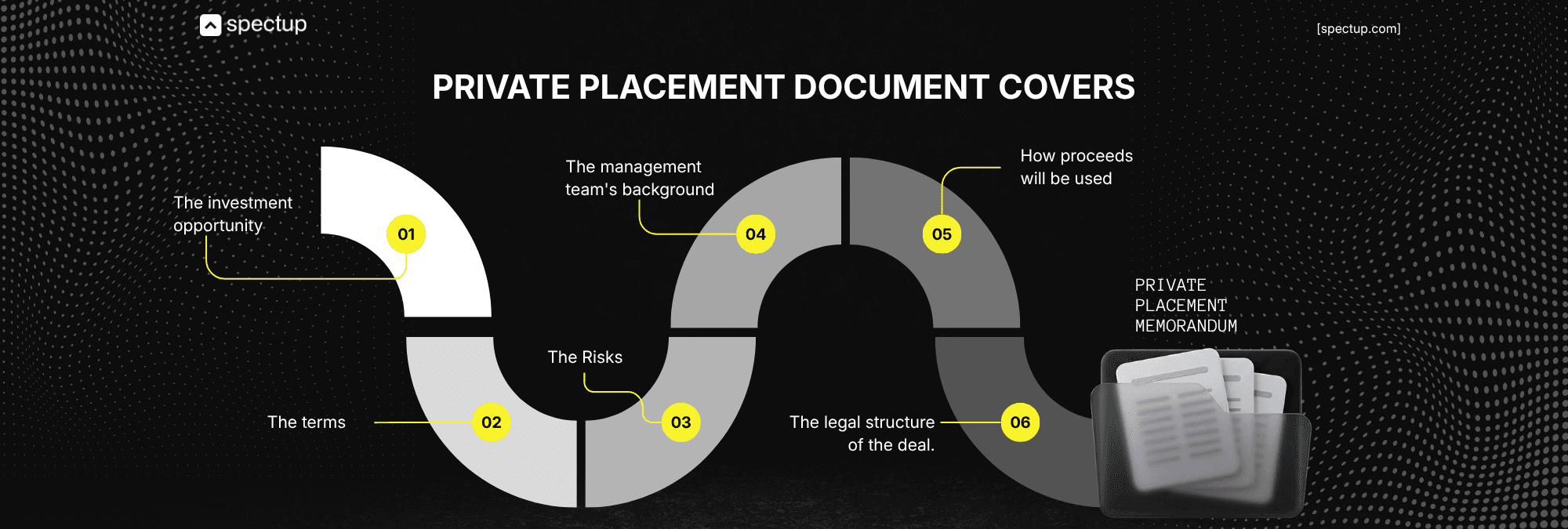

What a private placement memorandum covers?

It's the core legal document in any private placement offering, provided to prospective investors when a company or fund raises capital through a private securities sale. It covers:

The investment opportunity

The terms

The risks

The management team's background

How proceeds will be used

The legal structure of the deal.

Think of it as the anti-pitch deck.

A pitch deck tells investors why they should be excited.

A PPM tells them everything that could go wrong, and protects the company when it does. Both are necessary.

Confusing the two, or treating the PPM as an afterthought, is how raises come apart.

The PPM exists because of a simple legal reality: when you sell securities, whether equity, convertible notes, debt, or fund interests, you're subject to federal and state securities laws.

Those laws require full and fair disclosure of all material facts. A well-drafted PPM satisfies that requirement. A missing or sloppy one creates exposure that can follow a company for years.

I tell every founder and GP the same thing: the PPM isn't paperwork. It's your liability shield. The time to care about it is before you take the first dollar, not after an investor's lawyer sends a letter.

When do you actually need a private placement memorandum?

Far more often than most founders think.

The situations that trigger a PPM are broader than most founders realize:

Any capital raise from outside investors:

- Accredited investors

- Family offices

- Institutions

- Friends and family.

Securities laws apply regardless of your relationship with the buyer.Regulation D offerings under Rule 506(b) or 506(c): the SEC doesn't technically mandate a PPM for Reg D, but recognizes a properly drafted memorandum as an effective compliance tool.

Running a Reg D offering without one is like driving without insurance: legal until something goes wrong.

Investment fund raises: VC funds, PE funds, hedge funds, real estate syndications.

LPs expect it. Their legal counsel will ask for it before writing a check.Any offering where you're selling a security: equity, convertible notes, SAFEs (in many jurisdictions), debt instruments, or fund interests.

Founders assume the PPM is only for large institutional rounds. In reality, I've seen raises as small as $500,000 create serious rescission exposure because the founder treated the friends-and-family round as informal.

One company I worked with had raised $1.8M from 12 investors over 14 months with nothing more than a term sheet and a handshake. When two investors wanted their money back after a pivot, the company had zero documentation to protect its position. The legal cleanup cost more than the PPM would have.

That story isn't unusual. It's the pattern.

But here's the part that should concern you more: the regulatory environment is shifting in favor of more private placements, not fewer.

The INVEST Act, passed by the House in December 2025, would expand the accredited investor definition through an exam-based pathway. More eligible investors means more private offerings, which means more PPMs drafted, and more opportunities for badly drafted ones to blow up.

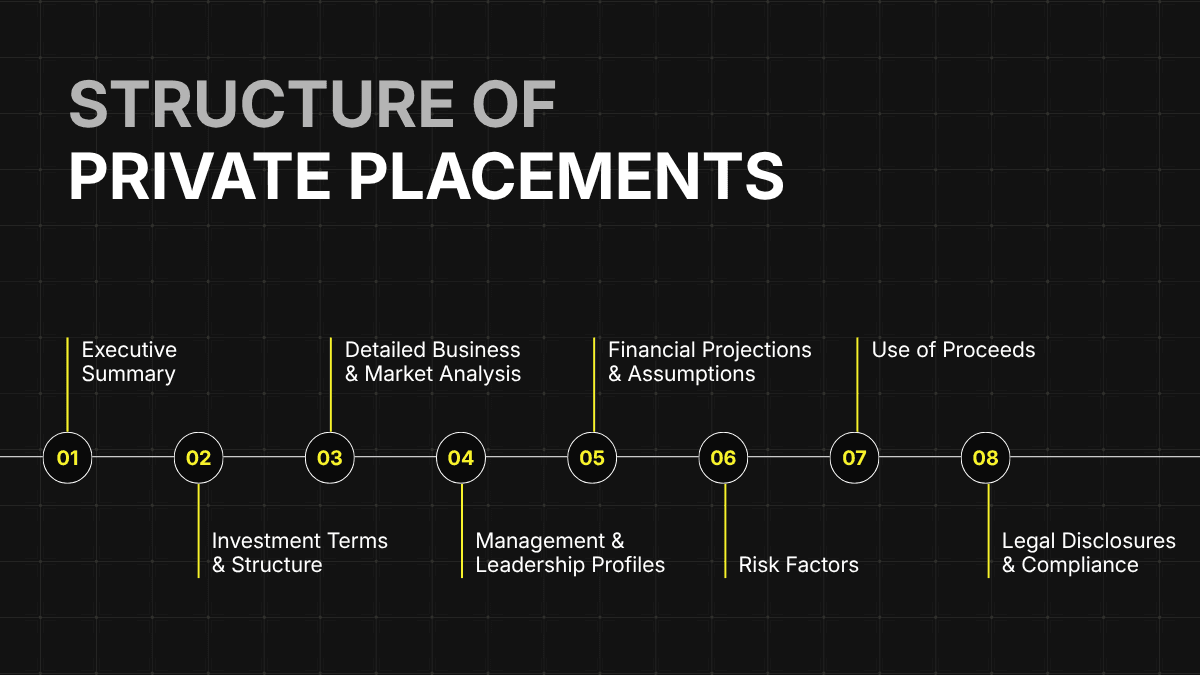

What actually goes into a private placement memorandum?

A few months ago, I reviewed a data room for a fintech company raising a $5M seed round. The PPM was there. The pitch deck was there. The financial model was there. But the subscription agreement referenced a different share class than the PPM described.

The investor questionnaire didn't match the exemption the company was using. And the use-of-proceeds section in the PPM contradicted the allocation slide in the pitch deck.

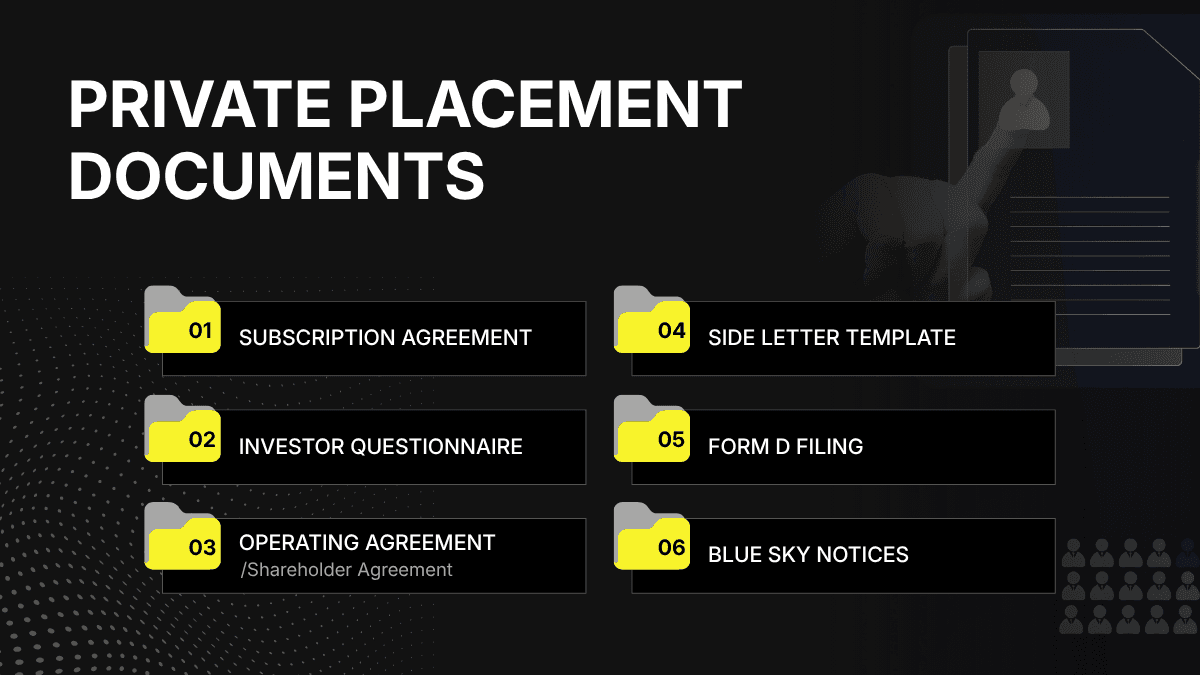

Three documents, three different stories. That's what happens when companies treat the PPM as a standalone file instead of the centerpiece of a document stack of 6 to 10 interlocking pieces.

The full stack for a standard private placement typically includes:

The PPM itself (terms, risks, management, use of proceeds)

Subscription agreement (the contract investors sign to commit capital)

Investor questionnaire (accreditation verification and suitability)

Operating agreement or shareholder agreement

Side letter template (for institutional investors with specific terms)

Form D filing and blue sky notices

The PPM covers the territory you'd expect: an executive summary, the specific terms (price per unit, minimum investment, security type, total offering size), a detailed use of proceeds, and management background. Those sections matter, but they're table stakes.

The sections that actually protect you are the ones companies rush through.

Risk factors are the backbone of your legal defense. Not boilerplate copied from a template. Specific risks tied to your business, your market, and your offering.

If your company depends on a single key executive, that's a risk factor.

If your industry faces pending regulatory changes, that's a risk factor.

I've seen PPMs with 15 risk factors and PPMs with 60. Look at any private placement memorandum example from a well-run institutional raise and you'll find 30 to 50 detailed risk factors.

The right number depends on your business, but the direction should always be toward over-disclosure, not under-disclosure.

Financial information is where credibility lives or dies.

Historical financials

Projections

The assumptions behind them.

The projections must be reasonable and clearly labeled as forward-looking. Overpromising here isn't just a credibility problem. It's a legal one.

I reviewed a raise where the pitch deck projected $50M in revenue by year three while the PPM's financial section showed a more conservative path. That mismatch is potential securities fraud.

And then there's the subscription agreement, the contract investors actually sign to commit capital. The investor questionnaire verifies accredited status and suitability. Under Rule 506(c), this verification is mandatory and must meet the SEC's "reasonable steps" standard.

Expect institutional investors to run their own due diligence process alongside reviewing your PPM, and they'll cross-reference every document against every other document.

Miss one piece in your private placement memorandum, and you create a gap. Gaps are where lawsuits start.

Rule 506(b) vs. Rule 506(c): which path fits your raise?

Most founders pick their Reg D exemption by accident. Someone tells them to "file a 506" and they nod. The difference between 506(b) and 506(c) isn't academic. Choosing the wrong one can invalidate the entire offering.

Feature | Rule 506(b) | Rule 506(c) |

|---|---|---|

General Solicitation | Prohibited | Allowed |

Accredited Investors | Unlimited | Unlimited (all must be accredited) |

Non-Accredited Investors | Up to 35 (with disclosure requirements) | None allowed |

Verification | Self-certification / reasonable belief | Must take reasonable steps to verify |

Fundraising Amount | Unlimited | Unlimited |

Typical Use | Relationship-driven raises | Marketed offerings, online platforms |

Rule 506(b) is the workhorse. It accounts for the vast majority of Regulation D offerings.

You can raise an unlimited amount from accredited investors, plus up to 35 non-accredited investors (though including them triggers additional disclosure requirements).

The catch: you can't use general solicitation or advertising. Every investor must come through a pre-existing relationship or direct referral.

Rule 506(c) allows general solicitation. You can publicly market the offering:

Advertise online

Present at pitch events

Post on social media

But every investor must be accredited, and you must take reasonable steps to verify that status. Self-certification isn't enough. You need documentation: tax returns, bank statements, or third-party verification letters.

Most companies raising $2M to $20M from known investors and their networks should default to 506(b). Simpler, faster, lighter compliance burden. If you need to cast a wider net or you're raising through an online platform, 506(c) gives you that flexibility, but the verification cost is real.

The choice needs to be made before the private placement memorandum is drafted, because the disclosure requirements, investor qualification sections, and subscription documents differ between the two. If you're unsure how these exemptions intersect with term sheet negotiations, get your counsel involved early.

And here's a wrinkle most founders don't know about: the INVEST Act would change the general solicitation rules so that presenting at certain sponsored events (universities, angel groups, accelerators) wouldn't count as "general solicitation" under 506(b).

Right now, a founder who presents at a demo day without careful structuring risks converting their 506(b) offering into something that requires 506(c) compliance. Structure your documents with flexibility.

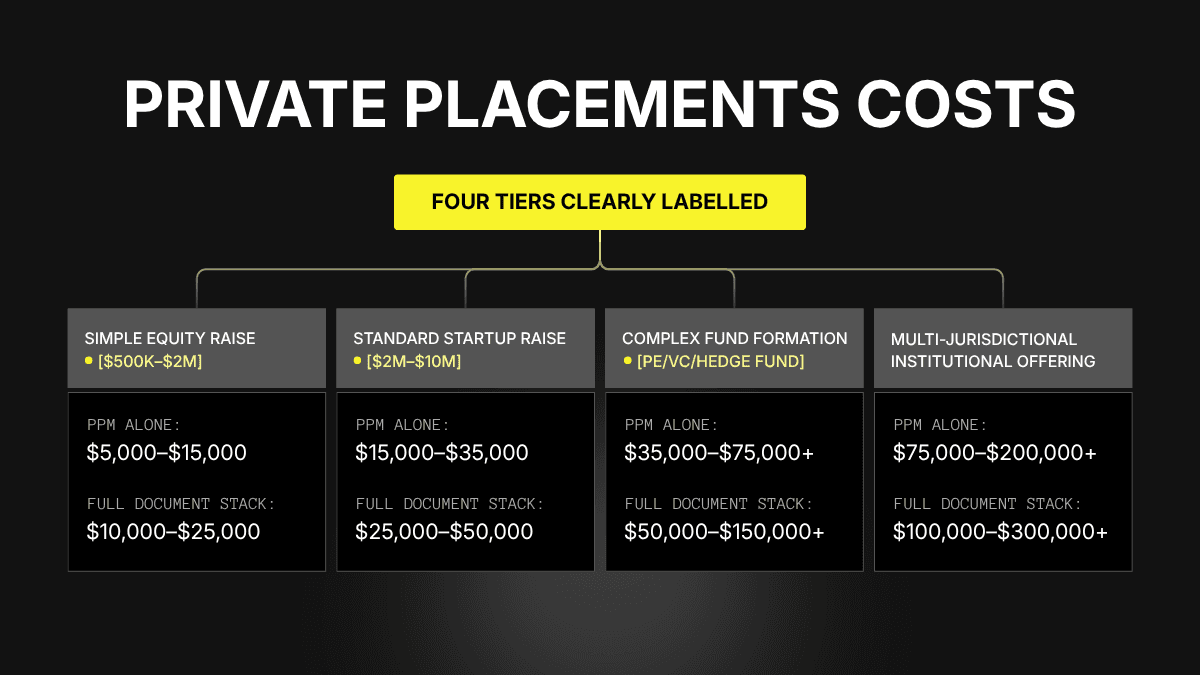

How much does a private placement memorandum cost?

Every founder asks this first. The honest answer is uncomfortable.

Offering Type | Typical PPM Cost | Full Document Stack |

|---|---|---|

Simple equity raise ($500K-$2M) | $5,000-$15,000 | $10,000-$25,000 |

Standard startup raise ($2M-$10M) | $15,000-$35,000 | $25,000-$50,000 |

Complex fund formation (PE/VC/hedge fund) | $35,000-$75,000+ | $50,000-$150,000+ |

Multi-jurisdictional institutional offering | $75,000-$200,000+ | $100,000-$300,000+ |

Source: Aggregated from ContractsCounsel lawyer bid data and industry pricing.

The biggest cost driver for a private placement memorandum isn't the size of the raise. It's the complexity of the structure. A clean equity offering for a single entity with one class of stock is relatively simple. A multi-entity fund with carried interest, management fees, clawback provisions, side letter rights, and cross-border investors is not.

Founders assume cheaper is better. One company I advise tried to save money with a template PPM purchased online for $2,500. Six months into the raise, an investor's counsel called with a problem: the subscription agreement didn't match the offering terms in the memo, and three risk disclosures were missing entirely.

The company had to pause the capital raise, hire securities counsel to rebuild everything from scratch, and re-circulate to existing investors. Two investors walked during the pause.

Total cost of the "savings": roughly $45,000 in legal fees, three months of lost momentum, and a reputation hit with the investor network they'd spent a year building.

A properly drafted PPM from experienced securities counsel typically runs $15,000 to $50,000 for a standard offering. Not cheap. But it's a rounding error compared to what a defective document costs when things go sideways.

The question isn't whether you can afford a PPM. It's whether you can afford the consequences of not having one.

What are the five mistakes that kill private placements?

After structuring capital raises across 150+ clients at spectup, these are the patterns I see destroy deals. All of them are preventable.

Founders assume friends and family don't need a PPM

This is the single most common mistake. A founder raises their first $500K to $1M from friends, family, and former colleagues. Everyone trusts each other. Nobody asks for paperwork.

Then the company pivots.

Or burns through the capital faster than projected.

Or simply struggles, as most startups do.

The investor who was your college roommate now wants to know what his rights are. The angel who's also your wife's business partner starts asking questions you can't answer because the answers were never written down. The rescission exposure from an undocumented round can unwind the entire capital structure.

Securities laws apply to every offer and sale of securities, regardless of the relationship between the parties. The friends-and-family round is exactly where PPM problems create the most damage, because when it goes wrong, it goes wrong personally.

Founders assume risk disclosures are boilerplate

Risk factors aren't filler. They're the section that stands between you and personal liability.

Generic risk disclosures copied from a private placement memorandum template provide minimal protection. Effective risk factors are specific to your business, your market, and your offering.

A securities attorney I work with regularly puts it simply: "If a reasonable investor would want to know this before writing a check, it needs to be in the risk factors."

Under-disclosure is where lawsuits start.

Fund managers assume a PPM template covers their structure

Fund formation is where template PPMs fail most spectacularly. A VC fund, a PE fund, a real estate syndication, and a hedge fund all have fundamentally different structures, fee arrangements, waterfall provisions, and regulatory requirements.

I worked with a first-time GP launching a $25M venture fund who started with a template PPM designed for a real estate syndication.

The carried interest provisions were wrong.

The distribution waterfall was wrong.

The clawback language was wrong.

The LP counsel for their anchor investor caught it during diligence, called the GP's attorney, and the conversation was apparently brief and unpleasant.

The GP had to rebuild the entire document stack, delaying the first close by two months and burning through $40,000 in additional legal fees.

For fund managers, the PPM isn't a one-time cost. It's the foundation of your LP relationships. At spectup, when we help GPs prepare their pitch deck and LP materials, the PPM is always the first document we align with the fund narrative, not the last.

Companies assume the PPM and pitch deck can tell different stories

The pitch deck says "we're going to 10x." The PPM says "you could lose everything." Both need to be accurate, and they need to be consistent with each other.

I've reviewed raises where the numbers simply didn't match. One company's pitch deck projected $50M in revenue by year three. The PPM's financial section showed a more conservative growth path. That inconsistency isn't just sloppy. It's potential securities fraud.

If an investor relies on the pitch deck's projections and later claims they were misled, the mismatch between the two documents becomes Exhibit A.

The fix is simple:

Align every number

Align your projections

Align all your claims across all investor-facing documents before they go out.

Companies assume Form D filing is optional

Regulation D requires issuers to file Form D with the SEC within 15 days of the first sale of securities. State-level "blue sky" filings may also be required depending on where your investors are located.

Missing the Form D deadline doesn't automatically void your exemption, but it creates a compliance gap that regulators and investor counsel will flag.

I've seen this bite companies during follow-on raises, when the new investors' counsel reviews the prior private placement and finds incomplete filings from the earlier round. That's a conversation nobody wants to have during their diligence.

What the INVEST Act changes for private placements

The regulatory ground is shifting, and most founders haven't noticed.

In December 2025, the House passed the INVEST Act (H.R. 3383) by a vote of 302 to 123. It's now with the Senate Banking Committee. Three provisions matter for anyone using private placements.

The accredited investor definition is about to get wider. The current thresholds ($200K income, $1M net worth) haven't changed since 1982. The INVEST Act would add an exam-based pathway:

Pass a free, SEC-administered test proving financial sophistication, and you qualify regardless of wealth.

For companies running 506(b) or 506(c) offerings, this could meaningfully expand the pool of eligible investors.

Qualifying VC funds get more room. The bill increases the qualifying VC fund size limit from $10 million to $50 million and raises the investor cap from 250 to 500. For emerging managers, that's a significant widening of the regulatory runway.

Demo days stop being a legal minefield. Presenting at sponsored events (universities, nonprofits, angel groups, accelerators) would no longer constitute "general solicitation" under 506(b). Right now, a founder presenting at a demo day without careful structuring risks blowing their exemption.

Whether or not the INVEST Act passes the Senate, the direction is clear. The SEC under Chairman Atkins is pursuing a pro-capital-formation agenda that includes fast-tracking semiannual reporting and raising the small entity RAUM threshold from $25M to $1B. The regulatory tailwind for private placements is the strongest it's been in a decade.

For companies running a private placement offering now, the practical move is this: structure your PPM and offering documents with flexibility. If the accredited investor definition expands, you want to be able to accept a broader range of investors without rebuilding your document stack.

The PPM comes first, not last

Here's something I consistently see at spectup that costs companies months: they treat the PPM as the last item on the checklist.

Pitch deck first

Financial model second

Investor meetings booked

And then, almost as an afterthought, someone says "we should probably get a PPM."

That ordering is backwards. The private placement memorandum defines the terms of the offering, the rights investors receive, and the legal framework of the deal. Everything else should be consistent with it.

The sequence that works:

Define the offering structure with your securities counsel

Draft and finalize the PPM and subscription documents

Build the pitch deck and financial model to align with those terms

Prepare the data room with all supporting documents

Begin outreach with a complete, consistent document package

I've seen companies spend $30,000 on a pitch deck and financial model, then discover during PPM drafting that their proposed offering structure doesn't work for the exemption they want to use. Rebuilding investor materials after the legal review is twice as expensive as getting the legal framework right before you start.

For companies navigating different stages of startup funding, the PPM becomes relevant earlier than most founders expect. If you're raising from anyone beyond co-founders and you're selling a security, you should be thinking about formal disclosure documentation.

My direct assessment

The private placement memorandum is the least sexy document in any capital raise. It's also the one that keeps you out of court.

I've worked on raises where the PPM saved the company. A biotech client was raising a $15M round when a major trial result came in below expectations. Two institutional investors wanted to exit. Their counsel called our client's attorney on a Friday afternoon, and the conversation could have gone very badly. But the PPM's risk factors specifically addressed clinical trial uncertainty.

The subscription agreement included clear lockup provisions. The investors' counsel read the documents, called back Monday, and said they'd honor the terms. Without that documentation, it would have been litigation.

I've also seen the opposite. An enterprise software company raised $3.2M from a mix of angels and family offices without a private placement memorandum or any meaningful documentation. Eighteen months later, they needed a bridge round. The new investors' counsel asked for the subscription agreements from the prior round.

There were none. The cap table was unclear. Prior investor rights were ambiguous. The bridge round took four months longer than necessary because everything had to be reconstructed from emails and term sheets that didn't quite match.

Here's what I tell founders who push back on the cost: you're not paying for a document. You're paying for the right to say "read section 4.3" when an investor's attorney calls with a problem. That's worth more than any pitch deck.

How spectup helps with private placements

We're not a law firm, and we don't draft PPMs. What we do is structure the entire capital raise around the offering, making sure the pitch deck, financial model, investor narrative, and outreach strategy all tell the same story as the legal documents.

For companies and funds raising $2M to $50M+, spectup acts as your private placement agent, handling investor targeting using 80+ timing signals, institutional-grade materials, and structured campaigns that generate 8 to 25 investor meetings monthly. We work alongside your securities counsel to make sure every document in the stack is consistent.

If you're preparing a private placement and want a fundraising consultant who treats your raise as a disciplined process, not a prayer circle, book a call.

Frequently Asked Questions

Is a private placement memorandum legally required?

No federal law mandates a PPM for Regulation D offerings. But the SEC recognizes a properly drafted private placement memorandum as an effective compliance tool, and the practical consequences of raising without one (rescission exposure, personal liability for misrepresentation) make it effectively mandatory for any serious capital raise. Most securities attorneys strongly recommend a PPM for any offering above $250,000.