Table of Content

Summary

Understand five DD categories

Financial, legal, operational, commercial, and tax due diligence each examine different risks. Investors use all five to validate assumptions before capital deployment.

[01]

Prepare data months before capital raising

Organize cap table, financials, contracts, and IP docs in a secure data room. This signals founder discipline and accelerates the 30-60 day due diligence timeline.

[02]

Red flags trigger deeper investigation

Management churn, high burn multiples, customer concentration, and NRR below 100% aren't automatic kills, but all require proactive explanation and mitigation evidence.

[03]

Commercial DD often wins or loses rounds

Market validation, customer defensibility, and competitive positioning often matter more than strong financials. Weak commercial evidence kills Series A even with good metrics.

[04]

Transparency builds investor confidence

Hiding problems until investor diligence surfaces them erodes trust. Founders who address challenges upfront with evidence of corrective action get second looks.

[05]

After running investor due diligence on 200+ capital raises across four continents, I've seen one pattern emerge: the companies that get funded aren't always the ones with the best technology or the biggest markets. They're the ones prepared for scrutiny.

Founders who enter investor due diligence with organised data rooms, transparent narratives, and proactive red flag disclosure are 3x more likely to close on favourable terms within 60 days. Success in investor due diligence starts with preparation.

This is a comprehensive, often gruelling examination.

It covers your financials, team, market opportunity, competitive positioning, legal status, and operational readiness. It's not a single conversation or a checkbox exercise.

Some firms complete this process in 30 days

Others take 60 days or more for complex deals

Either way, it's the step between "we're interested" and "we're investing."

Here's what separates processes that actually catch risk from checkbox exercises: scope clarity, documentation readiness, and, critically, honesty about what you don't know yet. Most founders scramble when it starts.

The best ones prepare for it before they need capital.

What is investor due diligence? The short answer is a systematic investigation where investors examine your company's financials, team, market opportunity, legal status, and operational health before committing capital.

This process typically takes 30-60 days and is the final step before a term sheet.

What is investor due diligence?

Investor due diligence is a systematic investigation of your financial, operational, legal, and commercial health before capital commitment.

It's risk assessment by another name, but the stakes are real: founders who organise their data and narrative in advance close deals 3x faster and on better terms.

For detailed guidance on what this entails, you can review FINRA's investor guidance and LSEG investment resources on frameworks.

From the investor's perspective, this process answers a core question:

Is this company worth the risk, and at what price?

Investors deploying capital they're accountable for (to LPs, boards, or their own funds) conduct thorough examinations to uncover hidden liabilities, misaligned incentives, team risks, and market validation gaps.

That's exactly the kind of systematic scrutiny that spectup provides for every capital raise.

From the founder's perspective, this investigation is the proving ground. Investors are testing whether your narrative matches your metrics, whether your team can execute what you're claiming, and whether your market opportunity is real or inflated.

Aspect | Investor Side | Founder Side |

|---|---|---|

Main Goal | Verify valuation, minimize risk | Prove readiness, secure capital |

Timeline | 30-60 days standard | Preparation begins months ahead |

Scope | Broad: financials, team, market, legal, ops | Comprehensive: everything they ask for |

Success Signal | Clear risk map, informed decision | Smooth process, fewer surprises |

Failure | Missing critical risk, overvaluation | Data gaps, legal issues surface late |

The distinction matters because founders often focus solely on the investor side, showing strength, when they should also prepare for the investee side: anticipating questions and organising documentation before the pressure intensifies.

Financial metrics investors examine

Due diligence conversations rely on financial and operational shorthand. Understanding investor due diligence mechanics requires fluency in these metrics. If you don't speak this language fluently, you'll sound unprepared.

Financial metrics investors examine: Understanding these metrics is critical because they're the language of fundraising. Working with a consultant fundraising expert helps you not just calculate these numbers but also prepare narratives around them that address investor concerns proactively.

ARR (Annual Recurring Revenue): Base revenue from subscription contracts over a year.

Growth-stage companies live and die by ARR. Investors compare your ARR to your burn rate to calculate runway.

CAC (Customer Acquisition Cost): Total sales and marketing spend divided by new customers acquired in a period.

High CAC (>12 months to recover via customer LTV) is a red flag for repeatability.

LTV (Lifetime Value): Total profit expected from a customer over their relationship with your company.

LTV-to-CAC ratio (target: 3:1 or higher) signals efficient unit economics.

NRR (Net Revenue Retention): Growth from existing customers (including upsells and cross-sells, minus churn).

NRR above 100% means you're growing revenue from your current customer base, not just adding new logos.

Burn Multiple: Monthly cash burn divided by monthly ARR.

Burn multiples above 3x signal inefficiency; below 1x signals strong unit economics.

Runway: Months of cash on hand at current burn rate.

Investors want to see a minimum 18-24 months' runway.

Deal-specific terms include DPI (Distributions to Paid-In Capital), MOIC (Multiple on Invested Capital), and IRR (Internal Rate of Return).

During investor due diligence, investors scrutinise your responses to these metrics. Investors grade your response to these metrics:

If you can't explain your NRR breakdown, your CAC payback period, or why your burn multiple exceeds peers', you signal inexperience or hidden problems.

Reviewing resources like our Series A traction metrics guide helps founders communicate effectively during capital raise phases.

Why does this process matter: real failures and what was missed?

Theranos: The $700M disaster from fraud. Elizabeth Holmes founded Theranos in 2003 with one promise: a device that runs 200 blood tests from a single finger prick.

By 2014, Theranos had raised $700M on the strength of that promise, with a $9B valuation and Holmes on magazine covers as the "next Steve Jobs".

The reality: the machines didn't work. Holmes faked the data. Investors who did thorough technical due diligence would have caught it immediately; most didn't ask the right questions.

Theranos collapsed in 2016, and Holmes was convicted of fraud in 2022.

When the Wall Street Journal finally published investigative reporting in 2015, the fraud unraveled within weeks. Investors lost over $700 million.

WeWork: $47 billion valuation collapse to $10 billion in months. Adam Neumann founded WeWork in 2010 as an office-sharing startup. By 2019, the company was valued at $47 billion, and Neumann was a billionaire on paper.

But investors who looked closely at the financials saw that WeWork was haemorrhaging cash, with unit economics that never improved.

The company's path to profitability was unclear. When the public markets got a chance to see the S-1, they immediately rejected the IPO.

Valuation cratered. By 2022, WeWork was bankrupt. Investors who skipped the detailed financial analysis paid dearly.

FTX/Alameda: $8 billion missing due to concealed conflict of interest. Sam Bankman-Fried founded FTX as a crypto exchange in 2019. By 2022, it was valued at $32 billion, and Bankman-Fried was the world's youngest self-made billionaire.

But a simple conflict-of-interest check would have revealed that Alameda, the trading firm Bankman-Fried also owned, was borrowing billions from FTX customer deposits.

This is a direct violation of financial controls and disclosure. When investigators looked closer, $8 billion in customer funds had vanished.

Bankman-Fried was arrested in 2023. This wasn't complicated to find; it required asking the question, "Where did the money go?"

The pattern across all three: The review process was either skipped, superficial, or deliberately hidden. This is why due diligence exists: not to block every risky investment, but to catch cases where founders misrepresent reality or hide governance problems from investor scrutiny.

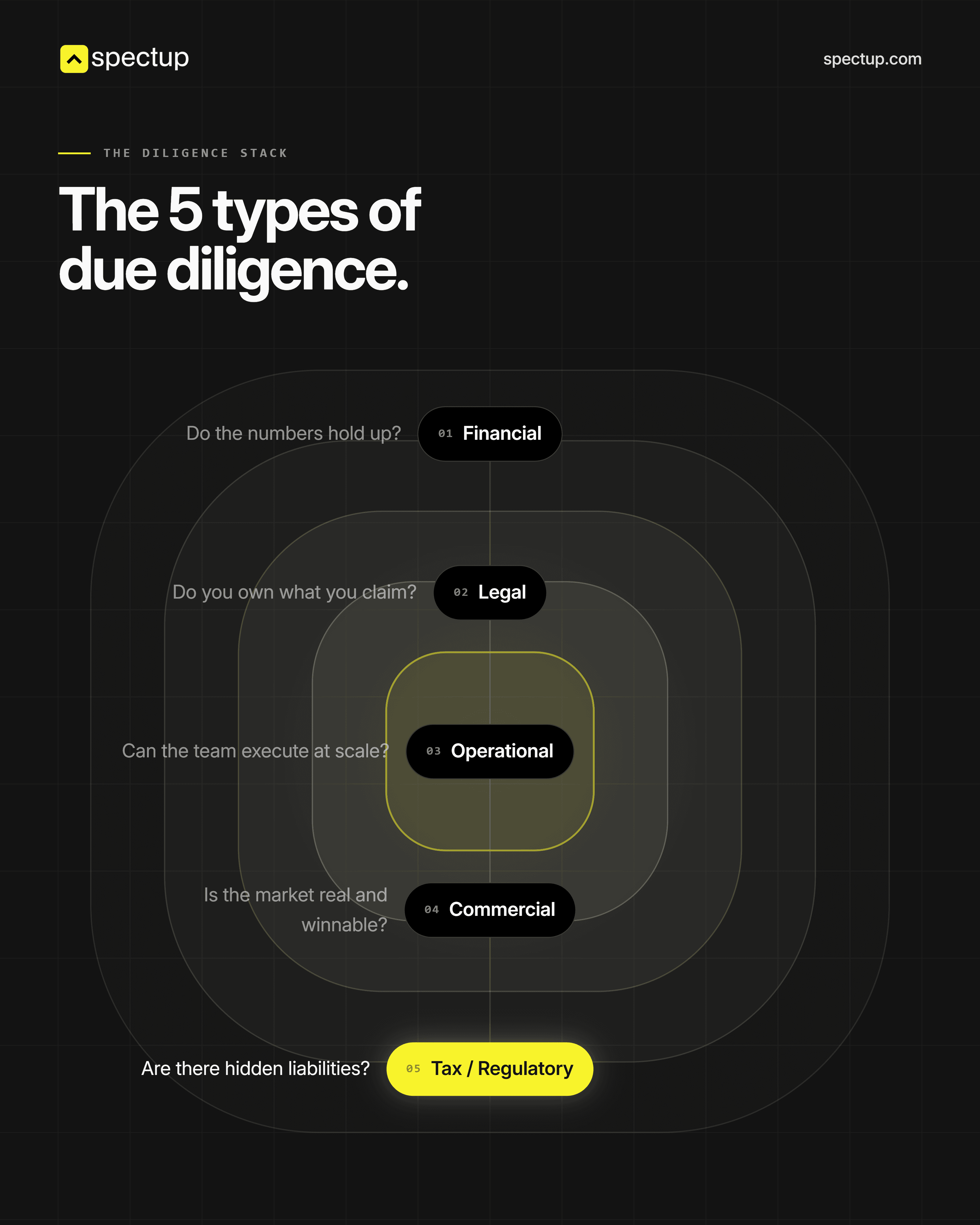

The five types of investor due diligence

Most founders I talk to prepare for one type and get blindsided by four others. Professional investors segment this process into five distinct categories, each uncovering different risks and requiring different expertise. Understanding each category, as detailed in resources like due diligence in private equity, helps founders prepare for comprehensive scrutiny during capital raises.

Financial Phase:

The scope includes:

Historical statements (P&L, balance sheet, cash flow)

Revenue quality

Gross margin trends

Burn rate

Projections

Capital efficiency metrics.

Red flags include revenue concentration (>30% from single customers), declining gross margins, and accounting irregularities.

This investment due diligence component focuses on past performance.

Legal Due Diligence:

Covers:

Cap table

Shareholder agreements

Contracts (customer, vendor, partnerships)

IP ownership

Litigation history

Regulatory compliance

Employment agreements

Red flags include disputed IP ownership, pending litigation, and customer contracts with termination clauses triggered by acquisition.

Operational Due Diligence:

Examines organisational structure:

Team backgrounds and track records

Key person risks

Vendor dependencies

Technology architecture

Data security practices

Scalability bottlenecks

Red flags include founder dependency, high engineering turnover, and inadequate data security.

Commercial Due Diligence:

Validates:

Total addressable market (TAM)

Competitive positioning

Customer validation (reference calls, retention data)

Market trends

Product-market fit indicators

This phase often reveals execution gaps that financial metrics alone miss and often determines whether investors proceed with a capital raise.

Tax and Regulatory Due Diligence:

Reviews tax compliance history

Regulatory exposure

ESG risks

Jurisdictional issues

Red flags include audit adjustments, tax disputes, and regulatory violations.

Type | What It Covers | Key Question | Red Flags |

|---|---|---|---|

Financial | Statements, margins, burn, unit economics | Do the numbers hold up? | Revenue concentration, margin decline |

Legal | Contracts, IP, cap table, litigation | Do you own what you claim? | IP disputes, customer exit clauses |

Operational | Team, processes, tech, dependencies | Can the team execute at scale? | Founder dependency, high turnover |

Commercial | Market size, competition, customer retention | Is the market real and winnable? | TAM inflation, customer churn |

Tax/Regulatory | Compliance, ESG, jurisdictional | Are there hidden liabilities? | Tax disputes, regulatory violations |

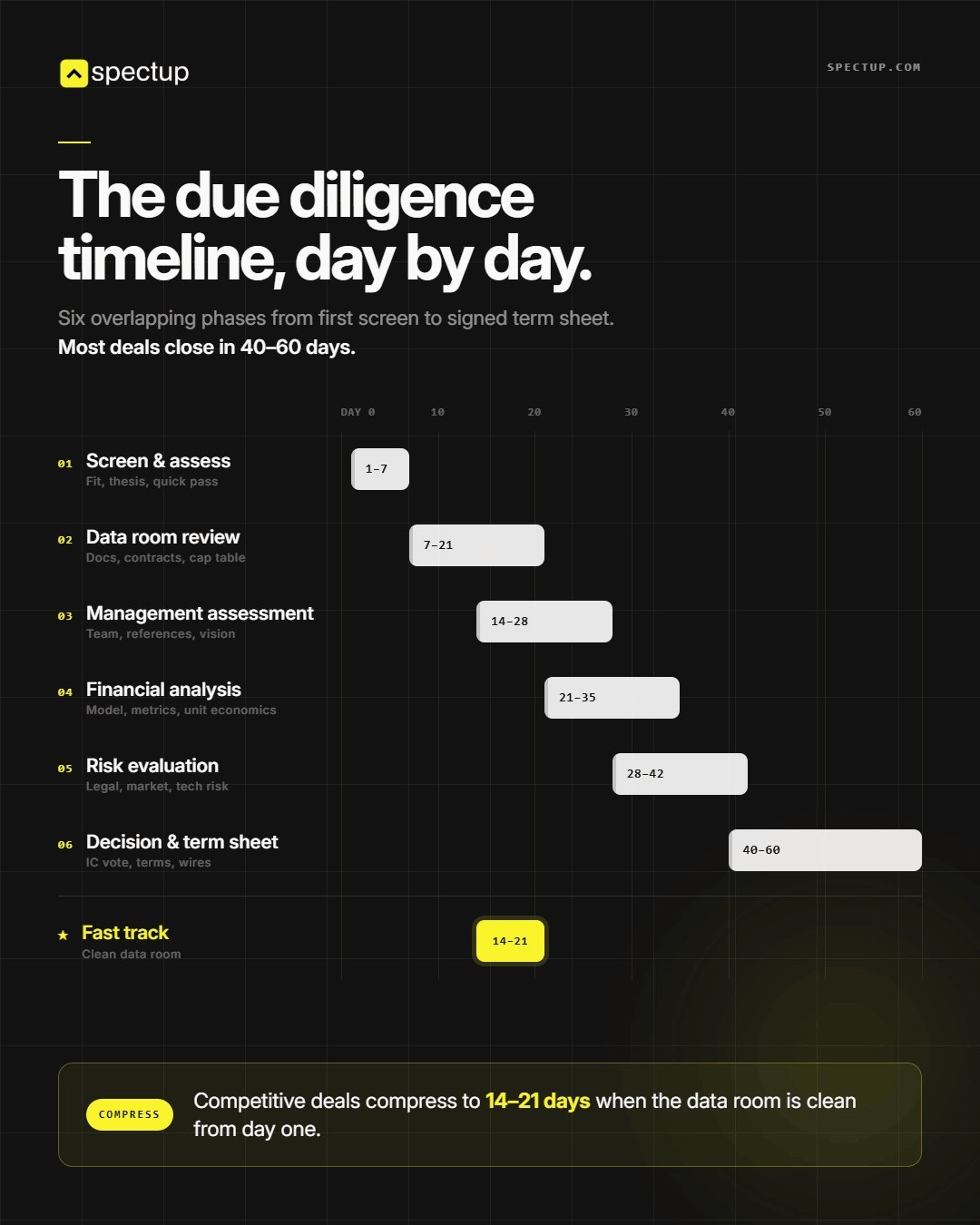

The investor due diligence process: six steps

A rough timeline: you get a term sheet with 30 days of exclusivity, due diligence starts the moment you sign, and founders who drag their feet on data requests are the ones who watch their deals slip.

The due diligence timeline compresses and expands based on deal heat, investor appetite, and company complexity. Most institutional processes follow a six-step sequence. For a detailed breakdown, review this investment timeline and capital raise guide.

Step 1: Screen and Assess (Days 1-7). The investor team reviews the pitch deck, financials, and your previous funding rounds. They assess market size, team pedigree, and initial red flags.

If you pass screening, the investor formally requests materials and assembles a team: financial analysts, legal counsel, and operational specialists.

Step 2: Collect and Review Documents (Days 7-21). Your data room goes live. You provide cap table, financial statements, customer contracts, employment agreements, IP documentation, and legal opinions.

Investor counsel reviews every document. This is where missing contracts or unclear IP ownership surfaces.

Step 3: Assess the Management Team (Days 14-28). Investor meets with founders and key team members. They ask about prior exits, operational mistakes, and key person dependencies.

For reference customers, they request permission to call them. This step answers the question:

Do we trust this team to execute even when market dynamics shift?

Step 4: Analyse the Financials (Days 21-35). Financial analysts model your business under different scenarios. They validate assumptions against market benchmarks and stress-test cash runway.

They examine CAC payback, LTV-to-CAC ratio, and gross margin trends. This step answers the question:

Does this company have sustainable unit economics?

Step 5: Evaluate Potential Risks (Days 28-42). All teams identify risks and flag decision gates. Legal surfaces pending litigation, finance flags burn rate concerns, and operations highlight team gaps.

Commercial assessment determines market validation level. This step answers the question:

What are the top 5 risks we need to address?

Step 6: Make Final Decision and Negotiate (Days 40-60). The investment committee votes to proceed, pass, or request additional review. If approved, the term sheet is issued.

Negotiations begin. Final legal documentation is drafted.

Total timeline: 30-60 days, though competitive deals compress to 14-21 days when investor appetite is high and data is clean. Having a comprehensive due diligence checklist ready beforehand speeds this process significantly.

Investment due diligence checklist: what investors examine

This due diligence checklist reflects what institutional investors examine across all five categories. Use it as a preparation framework. From my experience running hundreds of due diligence processes, early-stage investors focus primarily on cap table clarity, financial cleanliness, and founder credibility.

Financial Metrics & Health:

ARR or annual revenue, growth rate YoY, and monthly recurring revenue visibility

Gross margin trend over 36 months

CAC and payback period (months to recover CAC via profit margin)

LTV and LTV-to-CAC ratio (target 3:1+)

NRR and customer churn cohort analysis

Burn multiple (monthly burn / monthly ARR)

Runway at current burn rate (ensure 18-24 months minimum)

Revenue concentration: % from top 3 customers

Historical vs projected cash flow under stress scenarios

Customer & Market Validation:

. Customer reference list with 5-10 willing to speak confidentially

. Win/loss analysis: Why do prospects choose you vs competitors?

. Market research: TAM estimates with bottoms-up and top-down validation

. Competitive analysis: Positioning vs 3-5 direct competitors

. Retention cohort analysis: By vintage, what % remain after 12 months?

. Customer acquisition channel breakdown and unit economics per channel

Team & Governance:

. Founder and key executive backgrounds: Prior exits, operational experience

. Organizational structure and reporting with clear org chart

. Key person dependencies and knowledge transfer documentation

. Board composition and meeting frequency

. Advisor credibility and contribution level

Cap Table & Legal:

. Cap table: All shareholders, shares, and valuation history for past 3 rounds

. Shareholder agreements and liquidation preferences

. IP ownership: All code, patents, trademarks assigned to company

. Customer contracts with termination clauses and renewal terms

. Vendor agreements and exclusive relationships

. Litigation history and resolutions

. Employment agreements with vesting schedules

. Option pool percentage and exerciseability

What each metric combination reveals: High NRR (>110%) but low CAC payback (>12 months) signals revenue is growing from existing customers, but new acquisition is inefficient. Strong revenue growth but declining gross margins indicates a cost structure problem.

High customer concentration (>30% from 1 customer) kills institutional investor appetite regardless of strong metrics elsewhere. For comprehensive frameworks, consult the MaRS investor due diligence framework and the ILPA due diligence questionnaire.

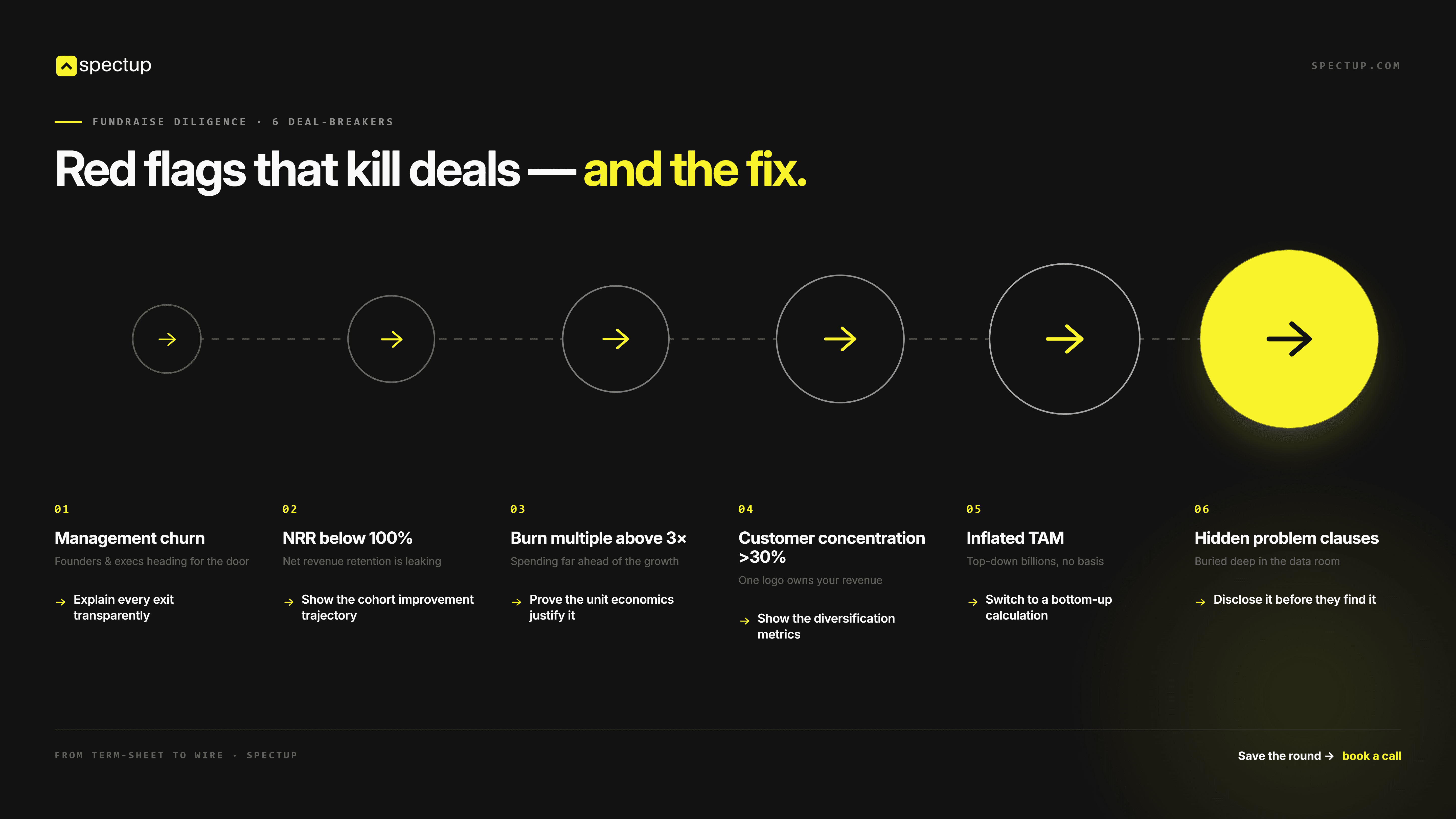

Red flags that trigger deeper due diligence

Certain patterns cause investors to dig harder, slow down timelines, or pass entirely. Recognising these red flags early, before investor due diligence surfaces them, gives you time to address them proactively. Know which are critical and how to address them.

How long does investor due diligence take?

Standard institutional timelines typically span 30-60 days

Though competitive situations compress to 14-21 days

Complex companies with red flags extend to 90+ days or longer.

Timeline depends largely on data organisation quality and how proactively founders address issues during the due diligence process.

Management Team Churn. The CFO left 6 months ago. The CTO left 12 months ago.

Only the founder has been constant. Investors see this pattern as execution risk.

What it signals: Either the company culture is broken or the business is struggling, and talented people see the exit.

How to mitigate: Be transparent about why people left.

Honest explanations and smooth transitions signal founder strength.

NRR is below 100%. Your base revenue is shrinking even as you add new customers.

What it signals: Product-market fit is questionable. You're in a "leaky bucket" scenario.

How to mitigate: If NRR is improving cohort-to-cohort, share the trajectory. Show what changed: new features, pricing adjustments, and better onboarding. Investors want to see you're aware of the problem and solving it.

Burn Multiple Greater Than 3x. You're burning $2M/month on $600K ARR, which means for every dollar of ARR, you're burning $3.30.

How to mitigate: If this is by choice (aggressive growth investment),

Show strong unit economics (CAC payback <12 months, LTV >$200K, gross margin 80%+).

By Series B, investors expect improvement toward 2x burn multiple.

toward aLarge Customer Concentration (>30% of Revenue). One customer is 40% of your ARR. If they leave, your growth narrative collapses.

How to mitigate: Show contract terms and retention strength. Invest in smaller customer diversification through metrics like "Our new cohort is averaging $20K ARR and growing at 40%."

Founder-Investor Misalignment on Governance. The founder wants a 10-year vesting period and super-voting rights. The investor wants standard 4-year vesting.

How to mitigate: Compromise early. Standard terms matter less than alignment on values. Find middle ground on what matters most to both sides.

Unsubstantiated Market Claims: "TAM is $50B. We'll capture 5%." No research to support it.

How to mitigate: Start with bottom-up TAM. "We surveyed 50 prospects. 80% are willing to adopt at $50K/year."

"That's 5,000 addressable customers × $50K = $250M TAM." Bottoms-up is far more credible than top-down projections from industry reports.

Understanding the difference between TAM, SOM, and SAM, and how to calculate each defensibly, is covered in our TAM, SOM, and SAM guide.

All these red flags are addressable. What kills fundraising is hiding them until the due diligence process surfaces them. Transparency builds trust. The cap table best practices start well before investor scrutiny begins.

Preparing for due diligence: the founder perspective

Founder due diligence preparation should start months before you raise capital. Most founders wait until an investor requests materials to begin organising. By then, you're playing defence in investor due diligence. The best founders prepare months ahead.

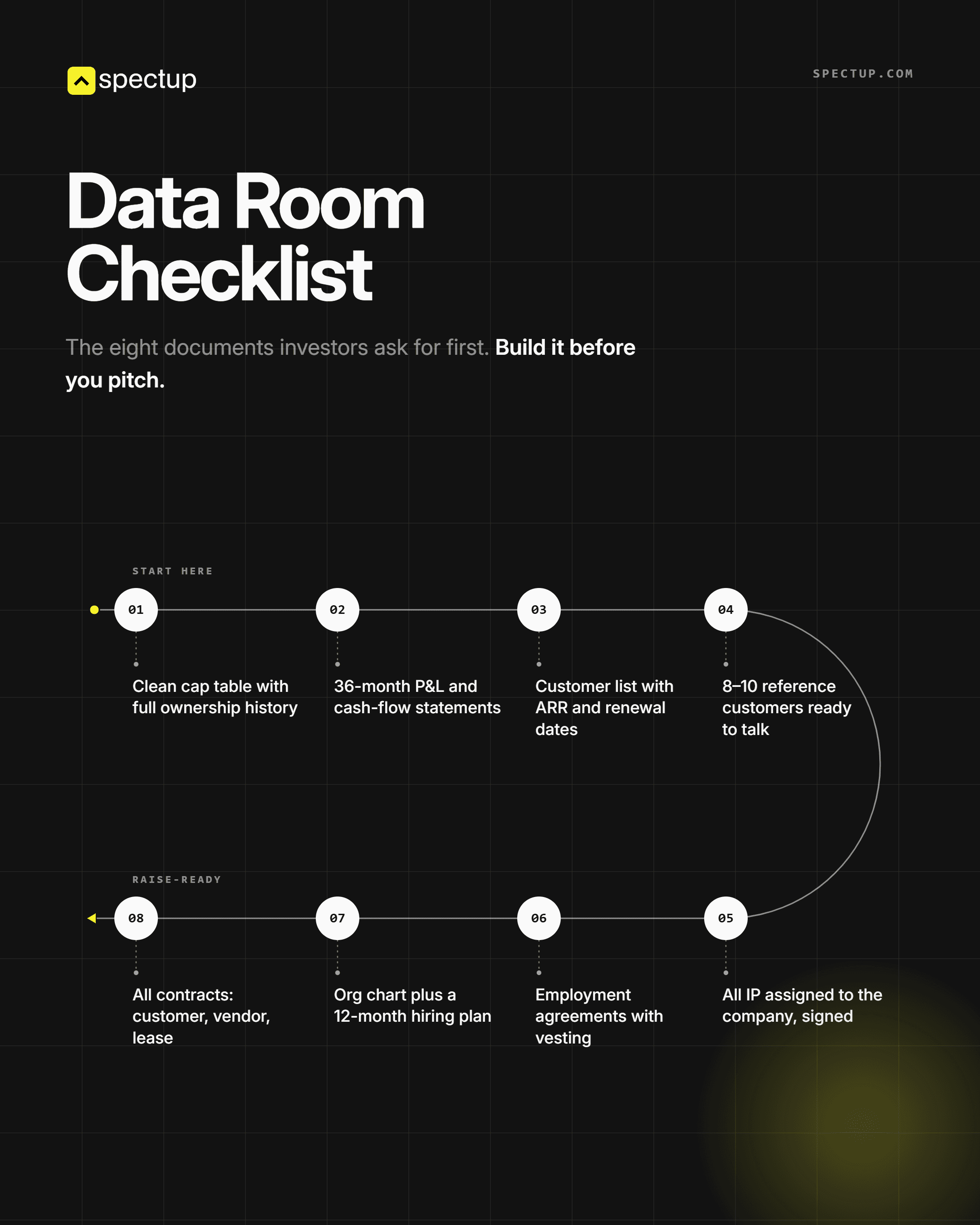

Data Room Setup (Months 2-3 before raise): Create a secure, organized investor data room (Carta, Box, or Intralinks).

Structure it by category: Capitalisation & Governance, Financial Documents, Contracts, Operations, Commercial, IP & Legal, and Due Diligence Materials.

Fully populate the data room before any investor sees it.

Document Preparation Checklist:

Cap table: all shareholders, share count, exercise price for options, vesting schedules

36-month P&L and cash flow with actuals and monthly detail

Customer list: name, ARR, contract start date, renewal date, key contacts

Customer reference availability: 8-10 willing customers for investor calls

Org chart with key roles and hirings planned for next 12 months

All contracts: Customer, vendor, lease, partnership

IP documentation: Proof that all code and IP is assigned to company, not founders

Employment agreements with vesting schedules, cliffs, and acceleration provisions

Timeline Planning: Once you enter due diligence:

Day 1, data room fully populated

Days 1-5, investor team reviews materials and submits first round of questions

Days 5-14, your team responds quickly (48-hour turnaround signals preparedness)

Days 14-30: management interviews, customer calls, and financial analysis continue in parallel

Days 30-45, the investor team synthesizes findings and identifies top risks

Days 45-60, negotiation and term sheet finalisation

Anticipate Investor Questions:

Why is revenue concentrated in 1-2 customers?

Why did that VP leave?

Why are customer cohorts retaining at lower rates than last year?

Have rehearsed, truthful answers.

If your company is public or considering it, familiarise yourself with SEC EDGAR filings to understand regulatory transparency expectations.

Assign a single founder as the primary point of contact for investor questions. If you have a CFO or COO, they can handle financials and ops questions. But founders should be visible for strategy, team, and market questions.

Investors want to assess founder credibility directly. Respond to written questions quickly (48 hours), schedule management meetings within a week of request, and make customer references available. This signals a well-organised company.

Red Flag Avoidance: Don't hide documents. If a contract has a problematic clause, disclose it. Don't misrepresent revenue or oversell team capability.

Don't sidestep difficult questions. Founders who come across as evasive or dishonest trigger deeper digging. Transparency builds investor confidence.

Commercial due diligence: the often-overlooked category

Many founders focus obsessively on financial due diligence (ARR, growth rate, burn) while neglecting commercial due diligence, a critical investor due diligence category that often determines whether your round closes.

Commercial DD has become increasingly rigorous as investor sophistication has grown and market conditions have tightened.

Financial due diligence answers:

Do your numbers hold up under stress?

Commercial due diligence answers:

Will customers keep buying this product at scale?

Understanding cohort-based retention analytics is critical for passing this stage.

Is there real competitive defensibility?

Are you capturing a real market opportunity?

What Commercial DD Examines: Market Validation (TAM estimates backed by bottoms-up research, not spreadsheet projections). Competitive Positioning (direct competitor comparison on features, pricing, and customer segments).

Customer Concentration and Churn (an investor calls your top 5 customers to assess defensibility)

Unit Economics at Scale (Does CAC remain constant as you scale, or does it spike?)

Defensibility (what prevents a bigger competitor from building your product and bundling it?).

Common Commercial DD Failures: The founder claims TAM is $5B but the actual addressable customers are 1,500. At $100K ACV, real TAM is $150M. The founder claims a strong NPS, but customers reveal they're switching at the next renewal.

The founder claims 200 customers at $50K, but 50 are on 6-month free trials with much lower real value. These hidden gaps often kill deals if not surfaced proactively.

How to Prepare for Commercial DD:

Provide 10-15 customer names willing to speak with investors.

Create a competitive matrix (your product vs 3-5 direct competitors) with feature parity, pricing, and differentiators.

Show both bottom-up (customer count × ACV) and top-down TAM estimates; bottom-up is more credible.

Prove unit economics scale: show CAC, LTV, and gross margin trends as you grow.

Commercial due diligence is the hidden killer of Series A rounds. Founders with strong financial metrics but weak commercial evidence get passed by institutional investors. Fix this before you fundraise.

Financial due diligence and cap table clarity: a founder story

A healthtech founder raising Series A had $1.2M ARR and strong unit economics. In the first week of due diligence, the investor's counsel asked for cap table history across all rounds. What arrived was a spreadsheet with conflicting numbers – three different versions of total shares outstanding.

Options had vesting cliffs she'd forgotten to track. One employee's grant was never actually formalised. It took her team five days to audit and rebuild the cap table correctly.

During those five days, the investor's diligence team sat idle. The deal narrative shifted from "let's accelerate" to "We need assurances this team can execute," and the timeline stretched from 30 days to 52 days.

Had she organised her cap table three months before pitching, DD would have closed in the first 30-day window. Instead, she lost weeks and negotiating momentum. The deal still closed, but at a lower valuation – the investor adjusted for execution risk.

Commercial due diligence and customer reference calls: another founder story

An AI SaaS founder preparing for Series B had impressive metrics: $3.1M ARR, 150% NRR, strong growth. But during the investor's commercial DD, the investor called her three largest customers. One of them revealed they'd nearly cancelled twice in the past year due to product instability, staying only because a workaround had been built just for them.

Another customer mentioned they were "exploring alternatives" with a competitor. The founder hadn't known this was happening. These calls surfaced churn risk she hadn't anticipated.

This forced a deeper customer concentration analysis and a complete rethinking of her retention narrative. Due diligence stretched from a planned 40-day close to 68 days while she reorganised her customer health metrics and drafted a remediation plan.

The lesson: investor customer calls often surface gaps that your own metrics hide. She closed the round, but it cost her two months and required new commitments on product stability.

Why does preparing months ahead actually matter?

I've watched founders close Series A in 6 weeks because their cap table was clean, their financials modelled, and every IP assignment was signed. I've also watched founders take 90+ days because they scrambled to organise their company while investors waited.

The difference isn't the quality of their product or their market opportunity. It's whether they treated due diligence preparation as a project that begins months before fundraising or as something that happens to them when an investor asks for materials.

Here's my direct assessment: The founders who raise fastest aren't the ones with the best products. They're the ones who had their data room built 6-8 months before they started pitching. Transparency, organisation, and proactive red flag disclosure build investor confidence faster than any pitch deck ever will.

I predict that in the next 18 months, founders without institutional-grade data rooms and clean cap tables will find it increasingly difficult to raise at speed.

Investor diligence timelines are tightening. Sloppy documentation that used to cost 2-3 weeks will cost 4-6 weeks. Founders who treat due diligence as an afterthought will lose deals to competitors who didn't.

The question isn't whether you'll go through due diligence. The question is whether you'll be ready when it starts.

My direct assessment of founder preparation

"Due diligence preparation isn't 4 weeks of scrambling. It's 12 weeks of getting ahead of investor questions."

I worked with a Series A founder in February who organised her cap table, financial model, and customer references 12 weeks before her first investor meeting. When the VC finally asked about cap table complexity, she had a 40-page IP assignment document ready. She closed in 35 days.

Her comparable, raised 6 weeks earlier, ignored prep and spent 110 days answering investor questions she could have pre-answered.

The pattern is consistent: founders who treat due diligence as a 12-week project close 2x faster. The difference isn't luck. It's whether you build institutional-grade materials before investors ask or scramble after.

How spectup helps founders prepare for investor due diligence

Most founders I work with don't realise that due diligence conversations are negotiable. You can shape investor focus, highlight your strengths, and get ahead of red flags – but only if your materials are organised and your narrative is airtight months before investor scrutiny begins.

That's where we help. spectup works with founders to build institutional-grade data rooms, prepare defensible financial narratives, and anticipate the toughest investor questions before diligence starts. Our pitch deck design services and fundraising consulting are built around the same principle: preparation beats reaction every time.

Take a B2B SaaS founder who came to spectup four months before fundraising. We helped her audit her cap table, model three financial scenarios for investor stress-testing, and prepare customer reference strategies that highlighted strengths rather than surface-level metrics. When diligence started, she handed investors a completely organised data room and responses to every common question investors ask at her stage.

Result: Due diligence closed in 34 days. No delays, no surprises, no renegotiation. She closed her Series A at her target valuation and timeline.

The pattern across 150+ clients is consistent. Founders who prepare their due diligence materials in advance – not during fundraising – close 30% faster and on better terms.

Concise Recap: Key Insights

Due diligence spans five distinct categories

Financial, legal, operational, commercial, and tax each examine different risks. Most founders focus on financial metrics while neglecting commercial validation, which often determines whether you raise.

Prepare your data room months ahead

Organize cap table, financials, customer contracts, and IP docs before any investor asks. Fast, complete responses during DD signal founder discipline and accelerate timelines by 2-3 weeks.

Red flags are addressable if explained proactively

Management churn, high burn multiples, customer concentration, and weak competitive defensibility aren't automatic kills if you acknowledge them and show corrective action. Hiding problems erodes trust permanently.

Frequently Asked Questions

What is the main purpose of investor due diligence?

The main purpose is risk identification and mitigation. Before committing capital, investors systematically examine your financial health, team capability, market opportunity, and legal position. Due diligence uncovers hidden liabilities, governance issues, retention problems, and competitive weaknesses that could affect returns.