Table of Content

Summary

Less than 15.5% of seed-funded startups raise a Series A within two years (Cambridge Associates 2025)

In Europe, the conversion rate is closer to 10%. This is not a funding climate where strong products get funded by default.

[01]

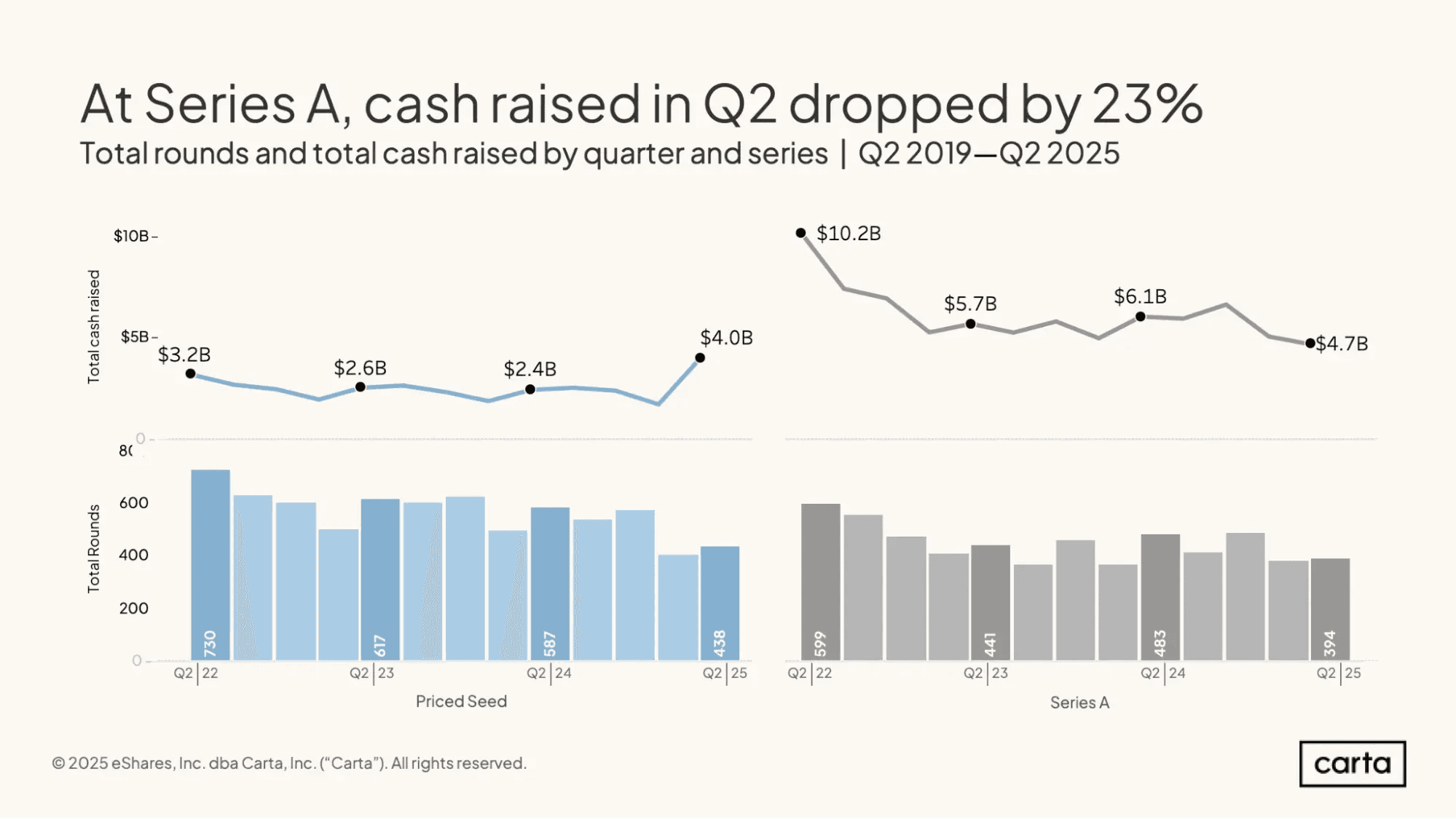

The ARR floor for a competitive Series A in 2026 is $3M, confirmed by Carta

2.$2M ARR is the minimum threshold, not the aspiration. Raising below $2M positions founders in the bottom quartile of competitive rounds.

[02]

Burn multiple (ARR generated / cash burned) has become a more common evaluation metric.

In my experience, most Series A investors cite targets around 1.5x-2.0x.

[03]

AI companies raise at a 40% valuation premium over non-AI peers at Series A

Non-AI founders raising in 2026 need a different preparation framework entirely, centered on capital efficiency and AI disruption resilience.

[04]

The median time from seed to Series A has stretched to 616 days

Preparation for a successful round starts on day one of seed deployment, not six months before outreach begins.

[05]

Less than one in six seed-funded startups in the US makes it to Series A. In Europe, the number drops to roughly one in ten. I have been in enough IC rooms and enough pitch preparation sessions to know that the capital raising gap between the companies that close and those that do not is rarely about the quality of the product.

It's about preparation and timing. It is specifically about whether founders understand what structurally changed.

I advise founders that while preparing for Series A, you should check out the criteria as per 2026. It's a structurally different market and different criterias are there.

As per Bain Global PE Report 2025, distributions as a share of NAV hit their lowest point in more than a decade in 2024.

Similarly, if we look at a broad scope here, the number of VC funds that successfully raised capital collapsed from 4,430 globally in 2022 to just 823 in 2025, an 81% decline (SeedScope), and the median time from seed to Series A has stretched to 616 days (Carta 2025).

Quick self-assessment - Are you ready to prepare for Series A?

I have added this quick checklist for founders so, they can assess whether they should be preparing for Series A round or look forward to modifying their metrics before proceeding ahead. If you answer NO to three or more of these questions, you are likely not yet ready for investor outreach.

I have compiled this checklist after checking out the successful raises and these represent structural requirements for most founders, though exceptions exist (top-tier repeat founders, or founders with exceptional user engagement metrics, might raise despite missing one or two metrics). For the majority of growth-staged founders, here is what competitive Series A investors are looking for:

Do you have $2M+ ARR? (Or credible path to $2M in less than 6 months?)

Is your NRR above 100%? (Do existing customers generate more revenue than they lose?)

Is your burn multiple below 2.5x? (Are you generating new ARR without burning through cash unsustainably?)

Can you document a repeatable sales motion? (Do you have 8+ customers from the same ICP acquired through the same channel?)

Is your cap table clean? (No dead-weight equity, all shares documented, vesting clear?)

What your Investor no's actually mean?

If you have:

Four or five NOs, plan for 6-12 months of focused operational work before investor outreach.

Two to three NOs, you are 3-6 months away from Series A readiness (depending on which metrics are missing).

If all your NOs are in one category (e.g., GTM), that is more fixable than scattered gaps.

Use the timeline to sequence your preparation work, and remember that venture capital rewards exceptions, if you have one exceptional strength, it can sometimes offset one weakness.

They are structural changes in the LP-GP-founder chain, and they reshape exactly what a VC needs to see when preparing for Series A.

Now, I have covered all mechanics that you should consider while preparing for Series A:

The macro forces driving investor behavior right now

The actual metric thresholds by sector

What the due diligence process looks like from the inside

The 12 to 18 month operational sequence founders need to follow before going to market.

I have drawn all these frameworks from my live deal experiences with founders and VCs across seed, Series A, and growth stage capital raises.

Why is the Series A funding environment different in 2026?

Three structural forces are reshaping how you prepare for Series A, in ways that look fundamentally different from any prior cycle. I'm not talking about trends here. These are real compounding mechanics that directly shape how a VC evaluates your company in those first 20 minutes of a process.

The LP distribution drought has entered its fifth year.

LP re-ups aren't automatic anymore. In 2026, capital is quite specific and cash velocity's now replaced growth narratives as the primary selection criterion. As per one McKinsey's 2025 LP survey, 2.5 times more LPs now rank DPI (distributions paid to investors) as their most critical metric versus three years ago. Right now, only 30% of LPs are actively seeking new manager relationships. Capital is not scarce. It is just concentrated, and the concentration is accelerating.

Cambridge Associates' 2025 report found that 15.5% of seed-funded startups in their dataset raised Series A within two years.

If you are a Series A founder, you should understand:

The GP writing your check is under direct pressure from their own LPs to show that investments convert to exits.

This is not just some paper markups, instead this is directly impacting your round.

VCs are underwriting exit likelihood from the moment they see your deck.

If your pitch doesn't make the exit path legible, it's just not going to close the deal.

Capital has bifurcated into AI and everything else

For the first time in history, AI and ML investments now account for 52.7% of total global VC deal value in 2025. Five companies alone, OpenAI, Scale AI, Anthropic, xAI, and Project Prometheus, raised a combined $84 billion. That's 20% of all global venture capital flowing into just five organizations.

I want you to sit with that for a moment before we move on.

We're living through a concentration of capital that has no historical precedent, and what I'm seeing in our own pipeline reflects exactly that. Founders who can't articulate where AI sits in their core operations, not as a feature, not as a bolt-on, but as something structural to how they deliver and scale value, are losing rooms they used to win.

This transition is not because investors have changed their taste; it is because the benchmark has shifted underneath everyone's feet.

The harder part is the valuation gap. Non-AI companies are now raising at 30 to 50% lower valuations than AI peers with comparable revenue and growth metrics. I've watched this across deals where the fundamentals were nearly identical.

With same ARR and same metrics, non-AI companies have meaningfully different outcomes at the term sheet stage.

It's structural gap, and it's already priced in.

What should you do as a Non-AI Native startup?

If you are not building an AI-native company, your Series A preparation requires two things your 2021 counterpart did not need:

A defensibility narrative that does not rely on AI sentiment

A capital efficiency story that is watertight.

The bar for what counts as interesting in a non-AI Series A pitch in 2026 is the bar that used to unlock a Series B.

The seed-to-Series A conversion funnel has a structural bottleneck:

There has been a 33% increase in reported seed rounds alongside a 9.6% drop in reported Series A rounds.

More than 1,000 startups are getting stranded between seed and Series A each year (Scaleup Finance).

Series A deal volume was down 18% year-on-year in 2025, with total capital invested down 23% (Pitchwise).

Last year was surprising for everyone in the capital sector, as we saw fewer deals were closing on more capital. It clearly portrayed that investors are not seeing fewer good companies. They are seeing fewer companies whose growth they can trust and whose exit path they can underwrite. You need to understand the mechanics before raising capital.

What revenue and traction do Series A Investors actually require?

Among the founders I've worked with, $3M ARR correlates with successful Series A closures. This data is also confirmed in Carta Q2 2025 report.

The 25th percentile was $1.8M, the 75th was $5.1M. This means roughly 1 in 4 closed below $2M.

If you're below $1.5M, closing is harder but not impossible, it just shifts the conversation to other metrics (product-market fit signals, founder pedigree, market size).

This shows the value of ARR in booking meetings with the investors. These Benchmarks Are Most Reliable For: B2B SaaS Raising $10-20M from Institutional VC in US/EU

For other founders, here are the ARR metrics:

Founder-led Teams with Exceptional Prior Exits

ARR floor: $400K-$1.2M (investors underwrite the founder, not revenue).

Key metric: Product-market fit signals (viral coefficient, net churn) over absolute ARR.

Deal killer: Still closing 80%+ of deals personally at $2M ARR, signals you can't scale the team.

Niche/Vertical Markets with Small TAM

ARR floor: $800K-$1.5M; NRR >120% required (you're burning addressable market, so expansion is existential).

More important: market share % and TAM penetration.Deal killer: Can't articulate TAM expansion path (vertical expansion, geographic rollout). Investors know you can't hit $100M in one segment.

Horizontal Products with Horizontal Churn Risk

ARR floor: $3M-$4M (higher than vertical).

Non-negotiable: NRR ≥110%, net logo retention ≥85%.

Churn is dangerous in horizontal markets; retention matters more than new logos.

Deal killer: High revenue growth hiding low expansion and high churn.

Revenue quality: what investors are actually slicing?

When an investor looks at your ARR number, the first thing they do is disaggregate it. They want:

Gross revenue retention

Net revenue retention

Logo retention by cohort.

Aggregate ARR that hides churn underneath is one of the most consistent deal-killers I've seen across live due diligence processes. Founders present a clean top-line number and genuinely don't anticipate what comes next. The number isn't the conversation. Investors are looking beyond numbers.

What healthy revenue retention looks like at Series A stage?

GRR at Series A:

GRR measures the percentage of revenue you're retaining from existing customers, excluding any expansion. Just the base contract value held.

Above 80% means your core product is sticky enough that customers aren't actively leaving. That's your floor.

NRR expansion for growth-staged startups:

NRR includes expansion revenue from those same customers like upgrades, add-ons, additional seats.

Above 110% tells an investor that customers are scaling their usage over time, which signals genuine pricing power.

Above 120% is exceptional.

Below 100% is a deal-killer.

I want to be direct about why here. It means you're acquiring new customers to replace losses from existing ones. That's a treadmill. This impacts your deal directly as investors are here for business deal and if they saw the revenue going down, they would hesitate to take a risk.

Does revenue metrics differ for AI and SaaS startups?

Yes and I want you to pay close attention, if you're building in AI.

AI-native SaaS products are averaging 40% GRR right now.

Traditional SaaS sits at 82%.

That gap is enormous, and it means the category itself carries a churn stigma that you will have to address before it gets raised against you. If you're building an AI tool, retention scrutiny isn't a question of whether it comes up. It's a question of how prepared you are when it does.

If you're traditional SaaS with sub-80% GRR, your Series A conversation needs to start with retention improvement, not customer expansion. Investors will underwrite your raise assuming you stay at your current GRR. They are not pricing in the improvement you believe is coming.

Typical Series A parameters in 2026:

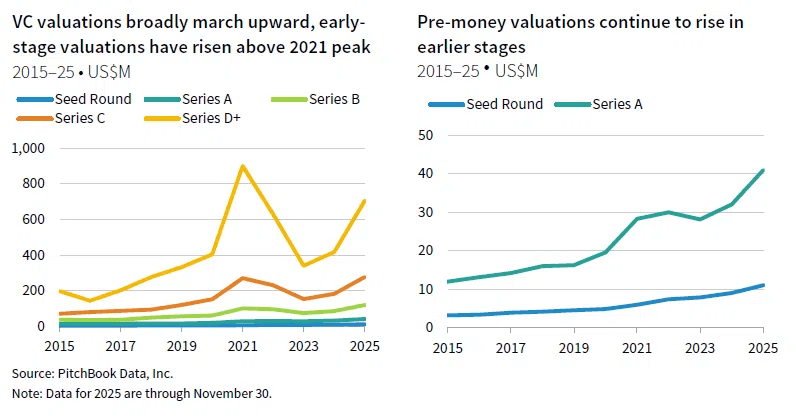

A standard Series A in 2026 raises $10M to $20M, with a median around $12M. Pre-money valuations typically fall between $25M and $50M, with the median sitting at approximately $45M for primary rounds (Pitchwise).

The average funding amount in Q3 2025 was $18.1M. That number is useful context, but I'd caution against treating it as a target or a benchmark for what your round should look like.

These are parameters, not guarantees. Where a company actually lands within that range comes down to two things I watch closely in every raise we work on:

How well the process is architected

Whether you've built genuine competition among investors.

Valuations get optimized by the founder who controls the room.

What does a repeatable go-to-market motion look like to Series A investors?

This is the section most founder pitches skip, and it is where the most confident rounds fall apart in live investor due diligence.

The investor question at Series A is whether someone other than the founder can get customers at a repeatable cost.

Top-performing Series A companies are closing:

4 to 6 new deals per month at an ACV above $50K.

This is something I don't see discussed enough, that behind every successful raise, there's a pull built into the system.

A defined ICP

A consistent channel

A documented sales cycle

A pipeline that does not collapse when the founder stops making calls personally.

What kills deals in GTM due diligence?

When an investor asks a founder to walk through the last five closed deals, the answer that kills rounds is:

Five different entry points

Five different buyer personas

Five different closing processes.

If I were an investor, I would also take is as fiver experiment plan, rather than a sales motion and that creates a scaling risk.

The second kill that I have observed is lengthening sales cycles.

If the average cycle was 30 days in January and is 60 days now, that signals either a wrong ICP or a changing buyer.

A Series A investor reads that as evidence the go-to-market motion is not holding under scale conditions.

What to do before going to market?

Before any startup I work with goes to market, I walk them through the same checklist. This is not a formality, I take this as a serious checklist because the gaps it surfaces are almost always the gaps that stall a raise mid-process, and by the time an investor finds them, you've already lost negotiating position.

I go through this myself on every founder call, before we talk strategy.

Run an audit of the last 20 closed customers.

Map ICP consistency, channel source, sales cycle length, and who closed the deal.

If the pattern is incoherent, there is no repeatable motion yet. That is a 60 to 90 day repair project that creates a liability.

I advise founders to model CAC by channel.

Founder-led sales CAC is artificially low. Show investors what the CAC looks like when a sales hire closes the deal. If that number does not produce a payback period under 18 months, equity raising conversations need to wait.

Build a bottoms-up revenue model showing how the $10M ARR target gets reached:

Number of reps, quota, ramp time, and channel mix.

That model does more work in an IC meeting than any pitch deck slide.

The GTM audit that unlocked the round:

One founder I worked with came to us with $2.4M ARR and 85% year-on-year growth. At first, I saw the clean pitch, clear product, three Series A conversations but all those conversations were passed. That was a red signal for me.

When we ran the GTM audit, the problem was immediate. Fourteen of the last twenty customers had come through the founder's personal network. Two came from a paid campaign that had stopped converting. Four came from a partnership channel the company could not control or replicate.

I could clearly see that the investors were not wrong to pass. I could not see any sales motion, and that was the clear signal that founders needed to work on their infrastructure before connecting with investors.

I advised founder to go ahead and spend four months building the ICP documentation, launching a controlled outbound channel, and closing six customers through a dedicated sales hire before restarting outreach. After that, founder came back and we closed round eight months later at a $32M pre-money valuation. The ARR had barely moved, but the metrics and story made the deal clear for investors.

How do Series A requirements differ across sectors in 2026?

Sector matters more at Series A in 2026 than it has at any point since 2015. The investor framework for evaluating an AI company and a climate tech company are structurally different. Pitching the wrong investor type for a given sector produces waste of times lost for the founders.

AI startups

AI Series A pre-money valuations averaged $45.7M in 2025, roughly 40% higher than non-AI peers at the same stage. The premium is real, and that leads to same scrutiny during capital raise.

The primary filter for AI startups is defensibility. Every serious investor I sit across from asks the same question in different ways:

What happens to your product if OpenAI ships a feature that covers your core use case?

If the honest answer is churn, there is no exception to underwrite.

If the answer is proprietary data and workflow integrations that deepen with usage, that's your Series A narrative.

Retention is where the category gets exposed.

Budget-tier AI tools averaged 23% GRR in 2025.

AI-native broadly sits at 40% versus a B2B SaaS median of 82%.

Investors already know this. They're pricing in GPU cost structure and platform dependency risk before you walk in. Gross margin by customer segment needs to be audit-ready before any outreach begins, not after the first data room request lands.

Non-AI SaaS metrics for Series A:

Traditional SaaS multiples have stabilized in the 2.5 to 7x EV/Revenue range. AI SaaS raises at 25 to 30x. That gap is not narrowing, and founders who go into term sheet negotiations with wrong valuation anchors either leave money on the table or kill the deal.

The investor is asking one question internally before anything else: which parts of this product's workflow genuinely cannot be AI-generated?

Here are the metrics that I have seen closing rounds over and over:

NRR above 105%

Burn multiple below 2x

Rule of 40 above 30.

Companies that meet those thresholds and have a defensible sector wedge are still closing strong rounds.

Deep tech and hardware stage metrics for closing rounds at Series A

For deeptech and hardware, revenue is not considered the primary criteria. I have seen investors focusing on technical readiness here. One thing that I have seen quite often is that:

Most deep tech VCs will not seriously evaluate a Series A without TRL (Technology Readiness Level) 6, meaning a fully functional prototype in a relevant operating environment, not a controlled lab (WePitched 2026).

Only 29% of deep tech Series A companies have a repeatable sales motion. 30% of Series B deep tech companies still have no revenue as per First Momentum Ventures 2025.

The specific deep tech deal killer here is arriving at Series A with a capital plan that requires the investor to fund manufacturing.

Founders overestimate venture capital. However, VC is not designed to fund factory buildout. That conversation needs infrastructure capital, not venture capital, and conflating the two signals that the founder does not understand the funding stack.

Metrics for Climate tech capital raise

Global climate tech investment reached $40.5B in 2025, up 8%, but deal count fell 18% to 1,545 transactions, the lowest since 2020 (Sustainability Atlas). Like all other sectors, I observed bigger checks accumulated in climate tech as well.

The IRA rollback is the structural macro event reshaping every climate tech Series A calculation.

Any pitch that models revenue on IRA credits remaining fully intact, without a three-scenario unit economics analysis covering full credits, partial rollback, and full credit removal, will not survive a serious IC process in 2026.

Comparison of different sectors at Series A stage:

Sector | Primary Filter | ARR Required | Biggest Deal Killer |

AI | Defensibility and moat | $2M+ with NRR 100%+ | Wrapper positioning |

Non-AI SaaS | AI disruption resilience | $2M-$3M with NRR 105%+ | Horizontal moat-free positioning |

Deep Tech | Technical readiness TRL 6 | Pilots preferred over revenue | Under-TRL prototype |

Climate Tech | Policy resilience | Signed offtake contracts | IRA dependency without scenario analysis |

What do investors actually check during due diligence that founders never see?

Out of 200 companies a typical VC firm considers annually, 25 reach management review, 8 reach a partner meeting, 4 enter due diligence, and 1.7 investments close as per areport by Excedr. The pitch meeting is an elimination filter. The actual investment decision happens in an IC room the founder never enters.

The lead partner is building an internal memo that has to survive a room of skeptics.

IC members challenge assumptions, pressure-test the financial model, and probe customer concentration, margins, GTM repeatability, and founder succession planning.

If the IC tears apart a financial model, the champion loses credibility inside the firm. The deal dies quietly and the founder receives a vague decline.

The five things investors systematically check during Series A

Revenue quality by cohort

The MRR schedule gets sliced into GRR, NRR, and logo retention by cohort.

Aggregate ARR is a starting point. A company with $2.5M ARR where 60% lives in two customers is not a Series A company. It is a customer concentration risk.

Unit economics by channel

Founder-led CAC is treated as a temporary condition. Investors normalize to what CAC looks like when a sales hire closes. If the payback period doubles after normalization, the conversation changes.

Cap table cleanliness

An ex-co-founder holding 15 to 30% equity with no remaining vesting cliff and no active role is a deal-stopper. Investors will not fund a table with dead weight equity. Every share needs a signed agreement.

Verbal equity promises are red flags that surface immediately (Spengler and Agans investor readiness guide 2026).

IP assignment.

Every employee, contractor, and intern who touched the product needs a signed IP assignment to the company. Missing assignments derail deals at legal sign-off stage, typically at the point when both parties believe they are three weeks from close.

Data room consistency.

In my experience, when numbers contradict across documents, investors interpret it as either carelessness or deception. Most founders I've worked with who reconcile numbers early close deals on better terms.

The data room is an X-ray of how you run the company at Series A stage:

I've watched rounds collapse because of inconsistent ones numbers.

The pitch deck says $2.3M ARR. The P&L shows $2.1M.

The cap table references a convertible note implying $1.8M at issuance.

Many founders trip here, as they submit three documents, three implied realities, and this signals investors that either the founder didn't check financial model clearly before investor outreach or the numbers are hiding some systematic issues.

This causes the deals to over before even beginning.

Number inconsistencies raise red flags. In my experience, founders who catch these during their own data room review and proactively correct them haven't lost deals over it.

Founders who get caught by investors and scramble to explain usually do lose momentum. The difference is control of the narrative

Start building the data room three to four months before your first investor conversation.

Have an advisor review it as the investor would.

Run a full reconciliation across your deck metrics, financial model, and accounting records.

They need to match to the dollar.

The 2026-specific investor due diligence signal most founders miss

VC firms now use tools like Perplexity, ChatGPT, and proprietary AI scanners to aggregate market presence, competitive landscape, and sentiment data before the first meeting (PitchWorx Jan 2026). If a brand is absent from AI-generated answers about its sector, the company effectively does not exist in the modern due diligence process. This is a preparation variable.

What do European founders need to know about preparing for Series A when raising from US Investors?

The US dominated 60% of total global VC deal value and 80% of high-value rounds in 2025. European founders rely on US investors for 35% of their growth funding pool (Atomico State of European Tech 2024). By Series A, US capital is not just an option for most high-growth European companies. It is a structural necessity and I advise many startup founders to consider this for expansion.

Only 0.1% of European pension fund allocation flows to VC, compared to 10.4% of US public pension fund allocation as per Fortune Nov 2025 report. The capital a European company needs to accelerate frequently does not exist locally at growth stage. Therefore, founders must understand the shift needed to approach US investors.

The Delaware question

Some US VC fund documents prohibit investment outside Delaware entities. It is a legal constraint written into the LP agreement.

At seed stage, roughly 80% of US investors require a Delaware parent.

The requirement drops somewhat at Series A and further at Series B.

Ask each fund directly before engaging legal counsel. When required, the Delaware Flip involves incorporating a Delaware C-Corp and exchanging all existing shares for shares in the Delaware parent. The European operating company becomes a wholly owned subsidiary.

EU-Inc: what it is and what it actually changes

On March 18, 2026, the European Commission formally presented its proposal for EU-Inc, a single optional EU-wide legal entity that founders can incorporate in 48 hours for under EUR 100, with no minimum share capital requirement. It standardizes:

Share structures

ESOP frameworks

Governance across all 27 member states.

EU-Inc (proposed March 2026) would standardize European cap tables. However, as of writing, it's not yet law.

It requires Parliament/Council approval in 2026 and operability in 2027-2028. If you're raising Series A in 2026, don't make cap table decisions based on EU-Inc. It's not available yet. Treat it as nice to have eventually but plan for Delaware if raising from US investors.

What US investors expect differently?

US investors underwrite to a $1B+ exit path. The EU market as the primary TAM cuts the investor's addressable return model by 80%.

Lead with global TAM.

Position the EU as the validated beachhead.

Growth rate expectations are calibrated to US fund return models.

60% year-on-year growth may be excellent European traction. Against a US Series A bar of 3x, it does not position competitively.

US customer validation matters even at small contract values. Even one or two US lighthouse customers materially changes how a US investor reads the pitch.

It signals the product works in the market they understand and can reference-check.

US GAAP is non-negotiable. Financial statements prepared under IFRS or local European standards need to be reconciled before financial diligence can proceed.

This takes time and a specialized accounting firm. It cannot be started after term sheet.

Structural alignment that closed the round

A Berlin-based B2B SaaS company came to us preparing for a US-targeted Series A. EUR 2.1M ARR, strong German-market retention, and a well-built product. They had no US customers, and had a German GmbH structure. Three US funds passed within six weeks, all citing the same internal concern.

We built the 12-month bridge. The company landed two US pilot customers through warm introductions from their existing European investors. The cap table was audited and a Delaware C-Corp was incorporated cleanly. The pitch was rebuilt around global TAM with Europe as the validated beachhead.

The round closed 11 months later with a US-led fund at a $38M pre-money valuation. This is how structural alignment transitions whole capital raise.

The 18-month Series A preparation timeline:

The most critical insight is timing. Based on successful founders I've worked with, here's the typical sequence of 18-month Series A round. Many founders compress this into 10-12 months by starting investor conversations earlier. Others extend it to 24 months while building more traction. It depends on sequence and your startup niche.

Months 0-6: Metrics & financial foundation with GTM planning:

I advise founders to audit your current metrics against Series A benchmarks before starting.

Calculate your actual burn multiple, NRR, CAC payback, and Rule of 40 score.

Identify gaps.

If you are below $2M ARR or your burn multiple is above 2.5x, start here, this is a 3- to 4-month foundation-building phase.

Get your financial statements audit-ready.

Standardize your revenue recognition.

Document your customer cohort behavior.

Run the GTM audit first.

Map your last 20 customers by ICP consistency, channel source, and sales cycle length.

If the pattern is scattered, spend this phase tightening it.

Hire a sales person if you haven't. Model what CAC looks like when a non-founder closes deals.

Document your repeatable motion with real data.

Months 6-12: Investor familiarity & positioning

At month 6-12, you should start reaching out to investors.

Send monthly updates to 20-30 qualified investors.

Share wins, product progress, and key metrics.

Ask for advice on specific problems, not funding. Get warm introductions through your existing investors.

Build your data room.

Have a neutral party (fundraising advisor or peer) pressure-test your financial model and cap table for inconsistencies.

Develop your sector-specific positioning.

Months 12-15: Structural alignment & data room

If you are a European founder raising from US investors, complete your Delaware flip, get HMRC pre-clearance if applicable, and file your 83(b) election.

Finalize your data room with 100% consistency between pitch deck metrics, P&L, cap table, and financial model.

Have everything verified to the dollar.

Get IP assignments signed from every employee and contractor who touched the product.

Months 15-18: Market readiness & process launch

Month 15-18, you shouldbe ready for outreach.

If you have 50+ qualified investors in your pipeline and you have sent them regular updates for 6+ months, getting meetings should be easy. Now, start the formal fundraising process.

What are the five most common mistakes founders make when preparing for Series A?

Founders assume the pitch meeting is where the decision is made

This is an assumption that I have seen a lot. The pitch is an elimination filter. Most decisions happen in IC rooms, but some investors decide before the pitch based on deck alone.

Founders who do not understand this optimize the pitch for emotional resonance and show up to due diligence with a model that cannot withstand pressure. That kills the champion's credibility inside the firm. The deal dies quietly and the decline is vague.

Founders assume revenue growth is the primary signal

I advise founders to understand that revenue growth is the entry requirement. It is not a selection criteria but it heavily impacts your entire round due to your strong metrics. What investors are evaluating is the quality of that growth:

Where it came from, whether it repeats, and what it cost to generate.

But for some emerging fund categories (founder-friendly, revenue-based) explicitly, investors don't care about metrics. A company growing 80% year-on-year with high churn, NRR below 100%, and a burn multiple above 2.5x is not a Series A company in 2026. It is a company that has purchased top-line growth with capital. Investors recognize that pattern in the first cohort table they see.

Founders assume starting outreach means starting to fundraise

By the time the first email is sent, the decision about whether to take the meeting has already been made, based on signals accumulated over months. 78% of VCs in 2025 cited compelling narrative as a top investment factor (Qubit Capital 2025). Startups that closed rounds within 90 days of starting outreach were 2.5x more likely to secure follow-on funding (Crunchbase 2025).

The 12 months before outreach is when the actual fundraise is won or lost. Investor familiarity built through update emails, advice-seeking calls, and public progress signals does more than any first meeting. A minimum investor outreach pipeline of 50 qualified funds is a starting point.

Founders assume strong ARR means they are ready

ARR is a number. What investors need is a financial modeling consultancy grade model explaining how that ARR was built, and a bottoms-up projection showing how the $10M ARR target gets reached: how many reps, what quota, what ramp time, what channel mix.

Founders who present aggregate ARR without the cohort behavior, channel attribution, and forward model underneath it make the revenue number a question. Metrics without a model is one of the most consistent Series A failure patterns across live deal processes.

Founders assume valuation reflects performance

Valuation at Series A is a negotiation output shaped entirely by process dynamics. A founder running a serial process, one investor per week over four months, is signaling to every investor they speak to that no one else is excited. A parallel process with a hard close date creates the only condition under which investors move fast and on founder terms.

The typical pre-money at Series A in 2026 falls between $25M and $50M. Where within that range a company lands depends almost entirely on whether multiple investors are in process simultaneously. Valuation is not discovered. It is constructed through process architecture.

Conclusion:

Preparing for Series A is an 18-month operational discipline. The Series A bar in 2026 is not what it was three years ago. The metrics threshold has moved, the AI premium has changed what comparable means, and investors are running more rigorous process than most founders are prepared for.

I've seen across the deals that the founders who close well aren't necessarily the ones with the strongest numbers. They're the ones who arrived with consistent numbers, a data room that could survive scrutiny, and a process they controlled rather than one that carried them.

Retention, defensibility, capital efficiency, and structural readiness are not investor preferences. They're the entry conditions now. If your raise is 12 months out, the work starts today. If you want personalized guidance, spectup helps with this. If you prefer to DIY, the checklist above is a solid starting point. Either way, the investment in operational rigor before outreach beats scrambling during process.

Frequently Asked Questions

How much ARR do you need to raise Series A in 2026?

Carta Q2 2025 data confirms that $3M ARR is the benchmark investors calibrate around for a competitive Series A. $2M ARR is the practical minimum, not the goal. ARR alone is insufficient: investors require 3x year-on-year growth alongside the revenue number, NRR above 100%, and a burn multiple below 2x. The median time from seed to Series A has stretched to over 24 months, which means preparing for Series A starts at seed deployment, not when the company first feels ready to go to market.