Table of Content

Summary

2026 changed the fundraising clock

Median VC fund close stretched to 15 months and the top 10 funds captured 42.9% of capital, squeezing first-time GPs on terms.

[01]

GP commit is signal, not amount

Median commit sits at 1.7%, but how you fund it (cash, fee waiver, deferred) tells LPs more than the percentage itself.

[02]

Recycling is the hidden 25% lever

A $50M fund recycling 100% of fees plus 20% of commitments effectively adds five-plus more shots on goal across the life.

[03]

Side letters now do LPA work

Around 70% of institutional side letters in 2026 modify fees, with MFN tiering, ESG, and ILPA reporting as the new standard riders.

[04]

ILPA 2026 ended the netting era

The updated Reporting Template forces itemized fee, expense, and carry disclosure, redrawing which terms are negotiable versus visible.

[05]

$80 billion flowed into US venture capital and private equity in Q1 2026, the largest fundraising quarter since 2021 according to The VC Corner's fund-activity tracker.

And the top 10 funds captured 42.9% of all capital committed through Q3 2025, a record concentration logged in the latest PitchBook-NVCA Venture Monitor.

Median VC fund close stretched to 15 months, the longest in a decade.

That's the world emerging managers walk into. More capital, but concentrated. Longer timelines, but tighter diligence.

That's the backdrop behind every LPA conversation right now.

And in the middle of it, most first-time GPs we advise at spectup still sign the vanilla 2/20 LPA their lawyer hands them, then wonder why institutional LPs ask the same five questions about the same five hidden levers. The LPA reads fine on paper. It loses money in the actual mechanics.

This piece walks the 2026 reality of venture capital fund structure design:

The four-entity baseline

GP commit funding mechanics

Management fee step-downs

American versus European carry-waterfalls

Recycling provisions

Side-letter inflation

How the updated ILPA Reporting Template (effective January 1, 2026) changed what's negotiable versus what's now simply visible.

It's written for fund managers raising Fund I or Fund II, not founders. We pull from spectup's private placement agent advisory work and from the public 2026 data so the benchmarks are concrete, not legal boilerplate.

What are venture capital fund structures?

Before the LPA mechanics, the simpler question: what is venture capital fund design actually built on? Four entities, one LPA, and a stack of economic terms that decide who gets paid when.

A venture capital fund structure, sometimes called a capital venture fund setup or a venture fund capital stack, is the four-entity legal arrangement that sits behind every institutional VC fund.

The Fund itself is a limited partnership

A general partner entity controls investment decisions and signs documents.

A management company employs the team and runs operations. And the limited partners are the outside investors who actually supply the capital.

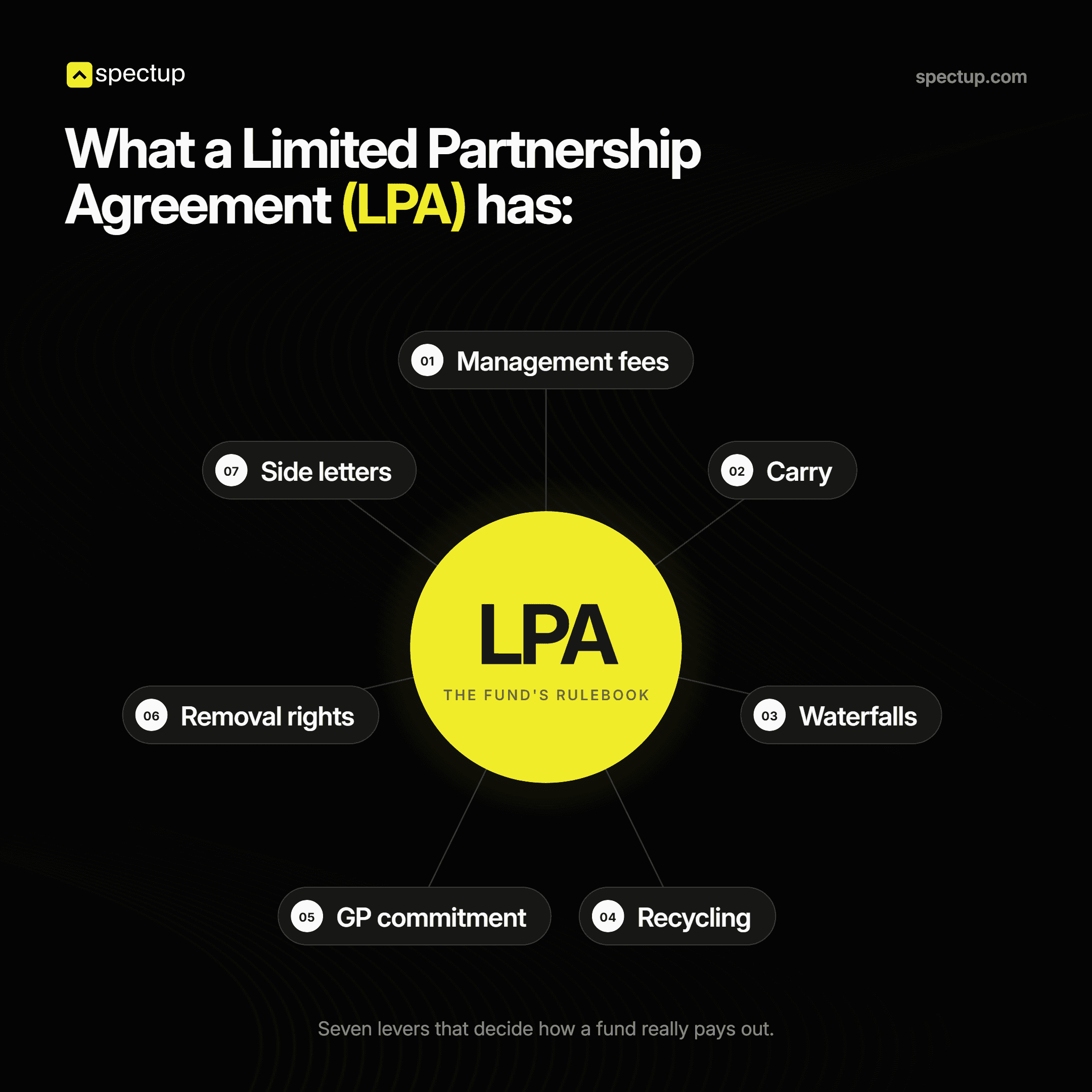

The Institutional Limited Partners Association and primers from operators like Sydecar describe the same baseline. The Limited Partnership Agreement (LPA) is the document that ties the four entities together and governs every economic term that matters:

Management fees, carry, waterfalls, recycling, GP commitment, removal rights, side letters.

The four entities sitting inside a modern venture capital investment fund, in the order LPs care about them, are

The Fund (Fund LP). The pooled investment vehicle holding the assets. LPs subscribe here.

General partner entity (GP LLC). Manages the fund, takes carry, signs investments, and bears fiduciary duty to the LPs.

Management company (ManCo). Employs the partners and the team. Receives the management fee. Pays salaries, rent, software, and travel.

Limited partners (LPs). Endowments, foundations, pension funds, family offices, fund-of-funds, and accredited individuals. They commit capital, the GP calls it, the fund deploys it.

The short answer is venture capital fund structures exist so the LPs get bankruptcy-remote ownership of the fund's assets, the GP gets liability protection at the entity level, and the management company can be paid a fee that's taxed as ordinary income while the GP's carry is taxed as long-term capital gains under Section 1061's three-year holding rule.

None of that's negotiable in the broad sense. What's negotiable lives inside the LPA, which is where the rest of this guide goes.

Why is 2026 a different fundraising environment for first-time gps?

Short answer: three numbers run the room when a first-time venture capital fund manager meets an institutional LP in 2026.

PitchBook tracked the median fund close at 15 months, the longest in a decade.

Second, the 42.9% concentration of capital in the top 10 funds through Q3 2025.

Third, the emerging-manager vehicle count at a decade low of 177 vehicles last year per the same PitchBook-NVCA series.

Capital is up. Access to it is harder.

What that does to fund-structure conversations is simple. LPs have more time to ask questions. They have less appetite for vehicles that look like a 2021 vintage.

And they're reading every term sheet against a much sharper set of benchmarks because their own allocation committees are reading against the same benchmarks. The result is that every venture capital fund manager bringing a Fund I to market in 2026 gets the LPA parsed line by line, not skimmed.

"The 2021 cohort got terms by showing up. The 2026 cohort gets terms by being the one fund in the diligence stack that already speaks the language of the LP's risk committee."

One recent example from our advisory desk. A first-time GP came in mid-raise on a $25M Fund I. The lawyer had given them a clean LPA.

Eight institutional LPs had passed. Not on a track record. On structure.

The recycling cap was the lawyer-default 110% of committed capital with no time window; the management fee basis stayed on committed capital for the full ten years, and the side-letter inventory was empty. We didn't change the strategy. We rewrote the LPA.

Six weeks later, they had two anchor commitments. The structure was the deal.

The macro frame matters because it sets the diligence standard for the LPA itself. A vanilla 2/20 LPA was once a baseline. In 2026 it reads as inattention.

Institutional LPs assume an emerging manager negotiates the same five terms an established firm negotiates and treats the absence of those negotiations as a signal about how the fund will be operated.

GP commitment: how much should you commit, and how do you fund it?

What's a GP commitment? It's the dollar amount the general partner personally commits to the fund alongside the LPs, intended as skin in the game. Per the Carta Fund Economics Report 2025, the median VC GP commit is 1.7% of fund size.

Sub-$10M funds run closer to 2%

Funds in the $25M-$100M band sit nearer 1.5%

Above $100M, commitments drop further as absolute dollars compound.

The number itself matters less than how you fund it. That's the part the competitor articles skip. Across the venture capital fund managers we audit, there are three live paths emerging GPs use, and the LP-signalling math on each is different.

Funding path | Mechanic | LP signal | Tax treatment | Common range |

|---|---|---|---|---|

Personal cash | GP wires cash to the Fund LP on each capital call alongside LPs | Strongest signal. Personal capital at risk on the same waterfall as LPs. | No special treatment. Standard capital contribution. | 1.5%-3% of fund size |

Management-fee waiver | GP waives a portion of future management fees and credits the waived amount as the GP commit | Acceptable if disclosed and modelled. Reads as cash-poor but committed. | Historically structured around fee-waiver-to-profits-interest mechanics, post-Section 1061 and IRS guidance, treatment is scrutinised. Fund counsel must opine. | 0.5%-2% of fund size, capped at the present value of fees waived |

Deferred / anchor-LP backed | An anchor LP advances the GP its commit on a side-letter loan or deferred payment basis, repaid from carry | Weakest signal alone, but defensible with anchor-LP cosign and disclosure | Loan treatment if structured as bona fide debt; otherwise contribution | 1%-2% of fund size |

One of our recent venture capital fund managers ran the second path. The founding GP had spent eight years at a tier-one growth firm and had earned strong carry, then took two years off to launch their own vehicle. By the time the LPA was drafted, the personal cash was low.

The institutional anchor LP signed off on a structure where the GP waived roughly 70% of management fees across the first three years and credited that against a 2% commit. The math worked. The LP saw alignment.

Diligence closed.

For a first-time venture capital fund manager, a low commit funded by waiver is a credible signal as long as it's explained, modelled, and acknowledged on the first LP call. A low commit that nobody addresses kills diligence faster than any other LPA detail. LPs aren't measuring how rich the GP is.

They're measuring whether the GP treats their own capital the way they will treat the LP's capital.

Silence on the GP commit reads as carelessness

Carelessness compounds across a 10-year horizon

First-time GPs assume the commit percentage is what gets diligenced. In reality, the funding mechanic is what gets diligenced.

A 2% commit funded with a clean fee-waiver disclosure beats a 3% commit nobody can model.

Management fees and the step-down that determines your team's runway

Management fees pay for the people, and across modern venture capital fund designs, they set the operating runway for the team. The standard is 2% of committed capital during the investment period, which usually runs three to five years. Then the fee steps down.

Two mechanics drive that step-down, and most emerging managers undernegotiate the second one.

According to Carta's management fees primer and the Cooley fund-formation primer describe the two paths.

The first is a rate step-down: the percentage drops, usually by 25 basis points per year, until it lands at 1.0-1.5%.

The second is a basis change: the fee stops applying to committed capital and starts applying to invested capital, or to the remaining cost basis after writedowns.

Institutional LPs win millions over fund life by negotiating the basis change. Emerging GPs almost never raise it.

Here's the maths on a $50M Fund I with a 10-year life, a 3-year investment period, and a market-standard step-down.

Years | Rate | Basis | Annual fee |

|---|---|---|---|

1-3 (investment period) | 2.00% | Committed capital ($50M) | $1.00M |

4 | 1.75% | Committed capital ($50M) | $0.88M |

5 | 1.50% | Invested capital (~$42M deployed) | $0.63M |

6 | 1.25% | Invested capital ($42M) | $0.53M |

7-10 | 1.00% | Remaining cost basis ($30-35M) | $0.30-0.35M |

Total fees across that life land near $6.5M-$7M, roughly 13-14% of the fund. Run the same model without the basis change, and the same fund pays closer to $8.5M-$9M. That's two analyst salaries every year for the back half of the fund, paid out of the LPs' upside.

This is exactly the kind of work a serious financial modeling consultant sets up before the LPA hits the lawyer.

Where most first-time GPs lose the negotiation: They negotiate the rate step-down (visible) and never raise the basis change (hidden). In the LPAs we audit, the basis-change clause is missing more often than it's present. That's negotiating room left unused.

A first-time GP can't win every fee fight, but the basis change is the one to push because the dollar value compounds across years six through ten.

The related term to watch inside any venture capital investment fund: fee offsets.

Portfolio company fees (board fees, monitoring, and transaction) flowing to the GP should offset management fees at 100%

The 80% offset is no longer marketed in 2026.

The new ILPA template makes this visible anyway, so the only question is whether you negotiate the rate or get caught by the audit.

Carry waterfalls: american vs european, and why most vcs choose neither in pure form

The short answer is, across modern venture capital fund structures,

American waterfalls pay carry deals by deal

European waterfalls pay carry whole-fund

Most US VC funds run a hybrid that looks American but acts European through clawback escrow.

The pure forms exist in textbooks. The market runs in between, which is why most US VC vehicles land somewhere in the hybrid middle.

The deeper comparison. American waterfall (also called 'deal-by-deal') lets the GP earn carry on each profitable exit once that investment has returned its cost basis plus the hurdle rate. The European waterfall (whole-fund) holds back all carry until LPs receive 100% of committed capital and the preferred return across the full fund.

The distribution-sequence walkthrough from The Fund CFO shows the cash-flow shape clearly: a $100M fund returning $250M in proceeds yields roughly a $30M carry pool under either structure, but the timing of when the GP touches that $30M is wildly different.

Dimension | American (deal-by-deal) | European (whole-fund) |

|---|---|---|

When GP earns carry | On each profitable exit, after that deal's cost basis + hurdle returned | Only after LPs receive 100% of committed capital plus the preferred return across entire fund |

GP cash timing | Years 4-7 typical first carry receipt | Years 7-10 typical first carry receipt |

Clawback risk | High. A GP may owe carryback if later writedowns drop the fund below the benchmark. | Low. Carry only paid after the benchmark is cleared on the full fund. |

Common LP type | US family offices, smaller endowments, accredited individuals | Pension funds, large endowments, European institutional LPs, fund-of-funds |

Complexity | Higher (per-deal accounting, ongoing clawback test) | Lower (single end-of-fund test) |

Typical 2026 US VC adoption | ~60% in modified American form (deal-by-deal with full-fund clawback) | ~30-35% pure; ~70% in Europe |

The "modified American" structure that dominates US VC in 2026 has three features. Deal-by-deal carry. A full-fund clawback that snaps back if writedowns later drag the fund below the hurdle.

And a carry escrow is holding back roughly 20-30% of GP distributions until the end-of-fund test confirms the GP earned what it received. The vglawfirm.com piece on LP economics in 2026 argues this escrow level is now baseline for institutional LPs and should be assumed in any first-time LPA.

The 8% preferred return plus 100% catch-up remains the market default for both waterfall types. The catch-up gives the GP carry-on prior LP returns once the hurdle is cleared, so over the life of a successful fund, the GP still receives 20% of total profits.

The catch-up rate (the speed at which the GP catches up, 100% or 50%) is sometimes negotiated, particularly by larger institutional LPs, and it interacts with each investment in venture capital the GP makes during the investment period.

Tiger Global's 500-plus-investment 2020-2021 cohort is a useful reference for why structure matters at scale. A capital-deployment pace that aggressively interacts with American waterfall carry differently than it does with European, because deal-by-deal carry creates pressure to mark winners early and ignore the long tail. Most of those funds are now working through clawback math.

SoftBank's Vision Fund, at $100B, is the same lesson in extreme: at that scale, the choice of waterfall doesn't just shift GP cash timing, it shifts the entire risk distribution between LPs and the GP, and the 2023 writedowns illustrated how violently a misaligned waterfall can reset expectations.

My direct view: emerging managers should default to European waterfall on Fund I and Fund II. The reasoning isn't ideological. It's that LP diligence is faster, clawback risk is lower, and the modest cash-timing penalty is more than offset by the credibility a clean European structure buys with institutional LPs.

'Modified American' only makes sense when the LP base actively prefers it, which is rare on a Fund I.

First-time GPs assume American welfare pays carry sooner and is therefore better. In reality, the clawback math on year-seven write-downs frequently makes Europe the higher-net structure for the GP. Speed of payout matters less than the probability of returning it.

Recycling provisions: the LPA term that decides whether your fund has 25 shots on goal

Recycling is the LPA provision that lets a GP redeploy realised capital instead of distributing it. On Fund I, it's the most consequential lever most first-time GPs ignore.

The math is direct. A $50M fund spending roughly 15% of capital on fees over its life has approximately $42.5M to actually invest.

Add a recycling provision allowing 20% of commitments plus 100% of management fees to be recycled

And you restore roughly $10M of deployable capital across the fund's life, about 25% more shots on goal.

This is one of the most under-negotiated levers across the LPAs we audit.

According to Carta's capital-recycling primer documents, the standard caps are 20-25% of committed capital, or 100-120% of management fees, with a 12-24 month window after distribution for redeployment.

The decision a GP has to make at LPA drafting is which cap to use and how to phrase the time window. Each variant has a different feel for LPs, and across the LPAs we audit, the cap-plus-window combination drives most of the back-and-forth.

Cap type | Typical range | LP-friendly version | GP-friendly version | spectup recommendation |

|---|---|---|---|---|

% of committed capital | 20-25% | 20% cap with 12-month window | 30% cap with 36-month window | Fight for 25% with 24-month window on Fund I; concede the window for the cap |

% of management fees | 100-120% | No fee recycling, or 50% cap | 120% with no time window | 100% of fees minimum. This is the term that earns the fees back. |

Uncapped | ~37% of funds historically | Rarely accepted by institutional LPs in 2026 | Strongly preferred by GPs | Do not push for uncapped on Fund I. Take the capped version and earn the trust. |

The case from our practice. Earlier this year, a first-time GP on a $25M Fund I came to us with a lawyer-default LPA that included no recycling provision at all. We added 100% of management fees plus 20% of commitments, with a 24-month redeployment window.

On a fund that size, that change adds roughly $5M of additional deployable capital across the life, close to one extra Series A cheque, or two seed cheques at full conviction. Same fund, same team, same strategy. Different LPA.

The institutional anchor LP read the recycling structure as "this GP thinks like an operator, not just a salesperson."

"Recycling is the only LPA term that meaningfully changes how many shots the fund actually gets. The carry math is downstream of how many bets you can place. If you don't fight for recycling, you're optimizing the wrong end of the equation."

What works against the GP: pushing for uncapped recycling on a first fund. Institutional LPs read that as an attempt to expand the fund without permission. The right play is to take the 20-25% cap, demonstrate disciplined recycling decisions, and renegotiate from a position of track record on Fund II.

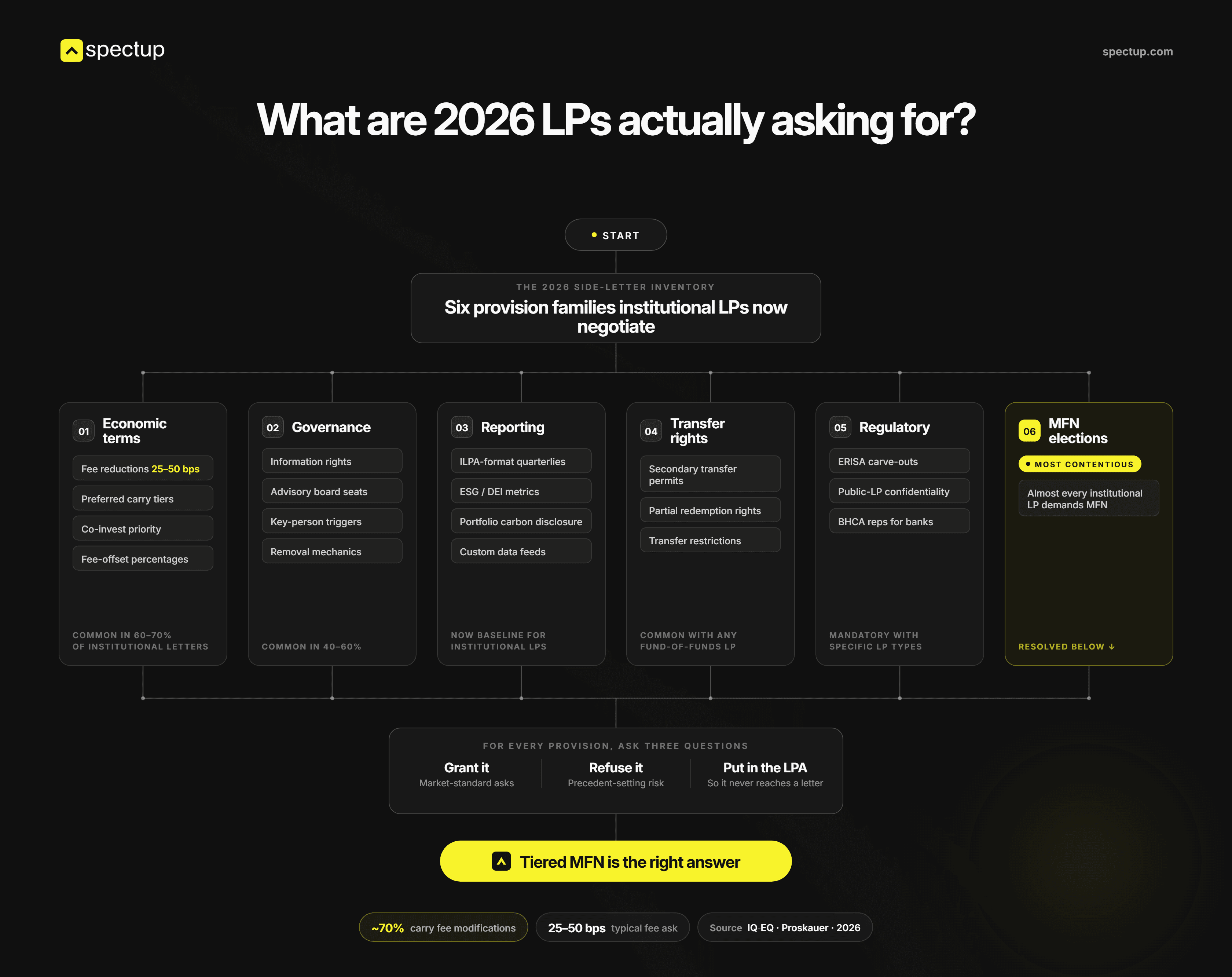

Side letter inflation: What are 2026 LPs actually asking for?

Short answer: side letters used to be light-touch riders bolted onto the LPA. Mostly MFN (most-favoured-nation) clauses and an occasional ESG carve-out. In 2026 they do as much economic work as the LPA itself.

The IQ-EQ January 2026 side letters guide and the Proskauer 2026 side-letter publication document the shift: roughly 70% of institutional side letters now contain fee modifications; a typical request is a 25-50 bps reduction on management fees; and the new common provisions extend well beyond economics.

The 2026 side-letter inventory is now riding on top of institutional venture capital fund structures.

What you should expect to grant?

What you should refuse?

What should be in the LPA so it never reaches a side letter?

Economic terms

Fee reductions (25-50 bps)

Preferred carry tiers

Co-invest priority

Fee-offset percentages

Common in 60-70% of institutional side letters

Governance

Information rights

Advisory board seats

Key-person triggers

Removal mechanics

Common in 40-60%.

Reporting

ILPA-format quarterly reports

ESG/DEI metrics

Portfolio-company carbon disclosure

Custom data feeds

Now baseline for institutional LPs.

Transfer rights

Secondary transfer permissions

Partial redemption rights

Transfer restrictions

Common with any fund of venture capital funds as the LP.

Regulatory

ERISA carve-outs

Public-LP confidentiality

BHCA representations for banks

Mandatory with specific LP types.

MFN elections

The most contentious. Almost every institutional LP demands MFN

Tiered MFN is the right answer.

The MFN problem deserves a separate beat. A naive MFN clause lets every LP elect any term granted to any other LP. A $250K LP getting access to the terms granted to a $25M anchor LP is the failure mode.

The 2026 market answer is tiered MFN:

Rights are linked to commitment size

Vintage tier

Closing date

A small LP can't elect large-LP terms. The Proskauer publication walks through the tiering math, and the vglawfirm 2026 piece shows how MFN tiering interacts with the broader alignment design.

Inside a fund of venture capital funds, side letters operate at two levels: between the fund-of-funds and its LPs, and between the fund-of-funds and the underlying VC funds it allocates to. Both stacks need MFN tiering. A fund-of-funds with sloppy side-letter discipline at one level usually has sloppy discipline at both.

First-time GPs need a side-letter MATRIX from the first close, not from the fifth one. The cousin to this is the placement agent conversation: when LPs route through agents, the side-letter inventory inherits the agent's standard riders, which is fine if you know it and disastrous if you don't.

A spreadsheet listing every grant, every LP, every commitment tier, with cross-references to the LPA section that pre-empts the rider. Without the matrix, side letters accumulate as administrative debt, and by Fund II the GP can't answer the question "what did you grant LP X" without a 90-minute legal call. That's a structural failure, not a paperwork failure.

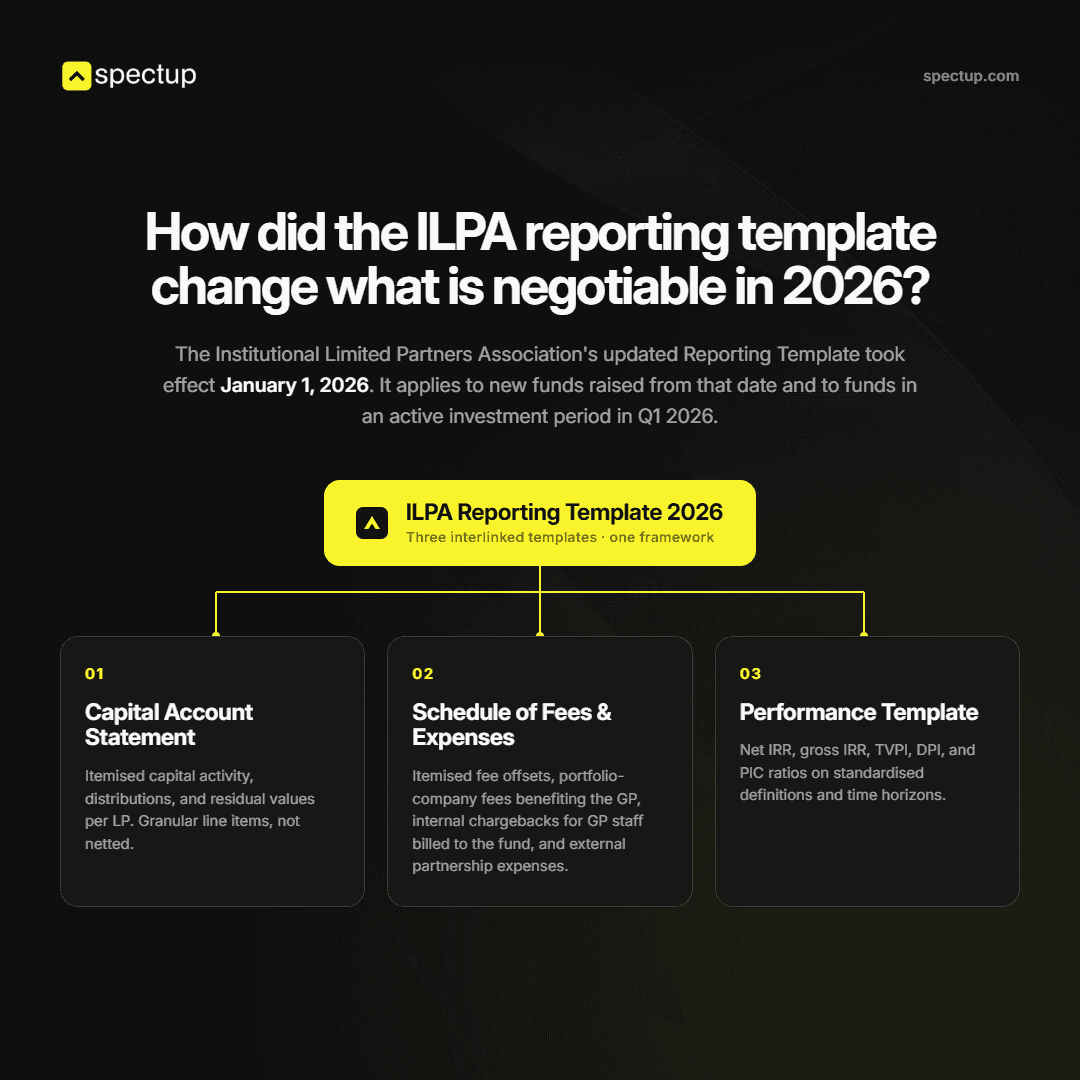

How did the ILPA reporting template change what is negotiable in 2026?

The Institutional Limited Partners Association's updated Reporting Template took effect January 1, 2026. It applies to new funds raised from that date and to funds in an active investment period in Q1 2026. The KPMG guide on ILPA 2026 documents the structural change: three interlinked templates now sit at the centre of LP-GP reporting.

The three templates now sitting under every institutional venture capital investment fund:

Capital Account Statement. Itemised capital activity, distributions, and residual values per LP. Granular line items, not netted.

Schedule of Fees and Expenses. Itemised fee offsets, portfolio-company fees benefiting the GP, internal chargebacks for work done by GP staff billed to the fund, and external partnership expenses.

Performance Template. Net IRR, gross IRR, TVPI, DPI, and PIC ratios on standardised definitions and time horizons.

What ILPA 2026 makes visible that was historically hidden in netting or aggregated reporting:

Monitoring fees, transaction fees, and consulting fees paid by portfolio companies to the GP or its affiliates

Internal chargebacks (GP staff time billed back to the fund as expenses)

Placement-agent fees and how they offset (or don't offset) management fees

Partnership expenses that previously aggregated into "other" are now itemized into legal, compliance, IT, audit, deal-related, dead-deal, travel

Capital-call and distribution timing with cash-on-cash precision rather than period-average smoothing

What this changes for fund-structure negotiation: the question is no longer "should we disclose this fee?" The question is "should we charge it at all?" Anything that goes into the new template will be read by every LP's allocation committee and every fund-of-funds analyst. Terms that survived for years inside netting calculations now sit on a single line item. Some of them survive scrutiny.

Some don't.

This is the biggest structural shift in venture capital fund structures since the 2/20 formula became the default. Funds raising after January 2026 without ILPA-compliant reporting are getting screened out at the gatekeeper level. Allocation analysts now run automated diligence checks against the template, and a fund that can't deliver clean ILPA reporting on day one fails the first filter regardless of strategy.

The practical implication for first-time GPs is that you draft the LPA and the side-letter inventory backward from the template. What needs to appear on the Schedule of Fees on day one? Make sure the LPA permits exactly that and no more.

What needs to appear on the Performance Template? Make sure the LPA's distribution mechanics produce numbers the template can render. Funds that draft the LPA forward (a lawyer hands you a template, you sign it, then you discover the reporting doesn't match) spend year one cleaning up.

First-time GPs assume the ILPA template is a reporting chore. In reality, the template is a structural filter the LPA has to satisfy before the first capital call. Reverse the drafting order and the rest of the LPA gets easier to defend.

Carry vesting, clawback, and the personal-liability conversation no one wants to have

Carry vests. That's the part most emerging GPs understand. What most don't understand until they're 80% into LPA negotiations is the interaction between vesting, clawback, and personal liability of individual GP partners.

The Archstone carried-interest guide documents the market-standard vesting:

Four to five years

A one-year cliff

Then monthly or quarterly thereafter

Forfeiture on bad-leaver termination

Partial or full acceleration on a good lever.

Clawback is the LP protection that requires the GP to return previously distributed carry if later writedowns drag the fund below the hurdle. Two mechanics. End-of-fund clawback tests once at fund wind-down.

Interim clawback tests periodically through fund life. Almost every institutional LPA in 2026 includes some form of clawback, and the vglawfirm LP economics piece notes that 20-30% carry escrow is now a baseline LP expectation as the mechanism for actually enforcing it.

Here's the conversation no one wants to have. The clawback obligation sits at the GP entity. Sometimes LPs require personal guarantees from individual partners so that if the GP entity can't fund the clawback, the LPs reach through to the partners themselves.

Solo GPs and small partnerships routinely sign these guarantees without modelling worst-case exposure. That's the single most common LPA mistake in our emerging-manager mandates.

Worked clawback example. $100M fund, $30M total carry earned, and $8M of that distributed across years four and five during a hot tape. Years six and seven bring two large writedowns.

The end-of-fund test runs in year ten and shows the GP overdrew its share by $5M. Who actually pays the clawback when the GP entity can't cover it?

If clawback sits at GP entity only, the GP entity owes $5M. If it has been wound down or has no assets, the LPs may have no practical recovery.

If clawback is backed by 25% escrow: roughly $2M of the $8M was held back, so $2M satisfies the clawback first and the GP entity owes the remaining $3M.

If clawback is backed by personal guarantees on the four partners, each partner is jointly and severally liable for the full $5M (less anything recovered from the GP entity or escrow). One partner can be pursued for the full amount.

One of our solo-GP advisory cases ran straight into this. The LPA draft included a full personal guarantee on clawback, with no cap and no carve-out for distributions previously paid as tax. The GP hadn't modelled the exposure.

We ran the math against three return scenarios and showed the worst-case personal liability sitting near $4-5M against a personal net worth a fraction of that. We renegotiated to GP-entity-only liability backed by 25% escrow across distributions. The anchor LP accepted because the escrow gave them recovery, and the GP no longer had a structural risk that could bankrupt them on a bad vintage.

The rule of thumb here. Carry is upside. Clawback is a downside.

Personal guarantees turn a downside into existential exposure. The right structure for an emerging manager is escrow first; GP-entity liability second; and personal guarantees only as a last-resort concession to a specific institutional LP who insists and never without a cap. Even partner-track contracts at established firms carry some clawback exposure in their carry compensation, but those firms have decades of distributions to reach back through.

A first-time GP doesn't.

My direct read after 18 months of advising emerging managers

Across the emerging-manager mandates we've run over the last 18 months on venture capital fund structures, watching first-time GPs sit across from institutional LPs and negotiate venture fund capital line by line, the same pattern repeats. The strategy is usually fine. The team is usually credible.

The differentiating filter is the LPA, and most first-time GPs lose that filter because they accept the lawyer-default 2/20 vehicle and think the negotiation is on the management fee rate and carry percentage. It isn't. The negotiation is on the five hidden levers.

Those five levers shape the LPA from Fund I onwards. GP commit funding (cash versus waiver versus deferred). Management fee step-down basis (committed versus invested capital).

Waterfall type (European default, modified American only when the LP base demands it). Recycling cap (100% of fees plus 20% of commitments minimum). And the side-letter matrix from day one.

None of them are visible on the LPA cover page. All of them decide whether the fund attracts institutional capital or stays with friends and family.

"Most first-time GPs negotiate their LPA the way founders negotiate term sheets, they fight for the headline number and concede everything that matters in the fine print. The institutional LP base in 2026 reads the fine print first."

The controversial position. Most emerging managers should reject the modified American waterfall on Fund I. The dominant US convention is doing first-time GPs a disservice.

Pure European waterfall is faster to diligence, lower in clawback risk, and signals discipline that wins the second close. I haven't seen a first-time GP suffer from the cash-timing penalty of Europe in any of the funds we've helped close. I've seen plenty suffer from modified American clawback nightmares in year seven.

The other position that will draw disagreement. ILPA 2026 will compress GP economics across every capital venture fund raised over the next three years. Not by changing rates, but by forcing the disclosure of fee streams that quietly subsidised the standard 2/20 model.

Portfolio-company monitoring fees, transaction fees, and internal chargebacks – these were the silent yield supplements. They're now itemised. GP take-home will trend down across the industry by a measurable amount as the new template gets parsed by LP allocation committees.

The funds that come out ahead are the ones that price this in from Fund I and structure clean.

How spectup advises emerging managers on venture capital fund structures

Our work with emerging venture capital fund managers on these structures typically starts six months before first close, and that lead time is where the room to move on the LPA lives. By then the strategy and the team are usually settled. The real lever is the LPA.

We run what we call The Five-Lever Audit, a structured review of the GP commit funding mechanic, the fee step-down basis, the waterfall type, the recycling cap, and the side letter matrix design. The audit produces a marked-up LPA, a side-letter template ready for institutional LPs, and a reporting architecture aligned to the ILPA 2026 Template before the first capital call.

Across the mandates that have closed in the last 18 months, the common pattern is that the structural rewrite gets the fund into institutional diligence stacks it couldn't reach with a default LPA. That has been true on $20M Fund I vehicles and on $80M Fund II raises. The structure decides whether the fund qualifies as institutional or stays in the friends-and-family pool.

We work most often with first-time and second-time managers raising $10M to $100M, the range where the LPA negotiating room on a capital venture fund is widest and the cost of a structural mistake compounds over the full fund life.

If you're six months from first close and your lawyer just handed you a vanilla 2/20 LPA, that's the moment to audit the structure before the first LP sees it. spectup runs that audit alongside the legal team and the institutional LP outreach so the LPA, side-letter inventory, and reporting architecture land in front of LPs as one coherent package. Book a call before the term-sheet cycle starts moving on you; every week of the mid-raise structure rewrites costs you negotiating room with the anchor LPs you haven't closed yet.

Where I'd actually focus right now if I were raising fund I

If I were closing a Fund in the current market and putting venture fund capital in front of institutional LPs, my pre-LPA prep list would be three items long, and they wouldn't be the items most lawyers prioritise.

First, I'd model the GP commit funding across all three paths before I touched the LPA template, because the LP signal on the commit decides whether the rest of the LPA gets a full read or a polite pass.

Second, I'd draft the side-letter MFN tiering before the first close, not the second, because the cost of fixing MFN at the second close is roughly five times higher than getting it right the first time.

Third, I'd benchmark the entire reporting architecture against the ILPA 2026 template before the LPA was signed.

The market is going to reward the GPs who get the LPA right early. The 15-month median close window isn't a temporary blip; it's the new baseline diligence cadence. LP allocation committees have caught up to the 2021-cohort sloppiness, and they have the time and the data tools to read every LPA against benchmarks they didn't have access to five years ago.

The funds that close fast in 2026 are the ones that show up with venture capital fund structures already correct, not the ones that promise to fix them before the second close.

And the last call I'd make. Stop letting the lawyer drive the LPA. The lawyer's job is to produce a defensible document.

Your job is to produce a fund. Those aren't the same task. The structure decides whether the fund attracts institutional capital or whether it raises from the same friends-and-family base everyone else is fishing in.

If you have a $25M target and you're six months out, that audit happens now, not after the first close.

Concise Recap: Key Insights

Five hidden levers decide your LPA

GP commit funding, fee step-down basis, waterfall type, recycling cap, and side-letter matrix design, none on the cover page, all decide institutional fit.

Recycling adds 25% more shots

A $50M fund with 100% of fees plus 20% of commitments recyclable restores roughly $10M of deployable capital across life, the single biggest hidden lever.

ILPA 2026 ended the netting era

The updated Reporting Template forces itemized fee, expense, and carry disclosure on day one, draft the LPA backward from the template, not forward.

Frequently Asked Questions

What is a venture capital fund?

A venture capital fund is a pooled investment vehicle, usually structured as a limited partnership, that invests committed capital from LPs into private startups in exchange for equity. The fund has a 7-10 year life, a general partner that runs investments, and a management company that employs the team.