Table of Content

Summary

The institutional door narrowed to one

Five firms took 73% of Q1 2026 LP capital. For sub-$100M emerging managers, fund of funds is the last institutional door still writing checks.

[01]

Name the FoFs that actually back Fund I

Cendana, Recast, Screendoor, Sapphire Partners, Top Tier and Al Waha back first-time managers. Most other names enter at Fund II or III.

[02]

FoFs run 8-14 week diligence, not 12 months

FoF diligence is faster than pensions, slower than family offices. Five stages: thesis screen, attribution, references, IC, legal. Plan accordingly.

[03]

Answer the three objections with math

DPI exposure, J-curve depth and fee-on-fee kill more emerging-GP FoF conversations than thesis weakness. Concede the structure, bring the numbers.

[04]

Europe's LP map is being rewritten

EIF ETCI 2 closes summer 2026 with €15B to back ~100 European growth-stage VCs. Per-company ceiling rises from €60M to €200M. Not a Fund I anchor.

[05]

A first-time GP I'll call GP-Alpha-7 sat in a co-working space in Munich last month, staring at a CRM full of dead pension funds. Eighteen months of warm intros, three soft-circled commitments, no closed capital.

Every European pension on the list had paused new VC allocations or "deferred to the next cycle". The endowments he could reach had moved upstream to Fund III managers only. He flipped open a second tab and started building a different list. Fund of funds.

That second list is the one that matters now. 73.1% of all LP capital raised in Q1 2026 went to just five venture firms, with the next ten taking 15.4% and everyone else fighting for the remaining 11.5%.

For sub-$100M Fund I and Fund II vehicles, the direct institutional channel did not narrow. It closed.

This post is the targeting playbook for the LP class that did stay open. I'll name which fund-of-funds venture capital programmes actually back first-time GPs:

What they write

How long their diligence takes

How to answer the three objections that kill most emerging-manager FoF conversations before the IC paper is even written.

The frame is GP-side, written from running ten live placement mandates at spectup right now, not from the LP-allocator perspective most explainers default to.

The fund of funds vocabulary that trips up first-time managers

Fund-of-funds work has its own vocabulary, and it differs from the founder-side fundraising glossary most GPs grew up on. Quick reference before the playbook lands.

Fund of funds (FoF)

A pooled vehicle that takes LP capital and allocates across 20-40 underlying venture funds instead of directly into startups. Two fee layers stack on top of each other.

Anchor LP

The first or largest LP in a fund close. An anchor signals to other LPs that the fund passed institutional diligence; a FoF anchor at 10-20% of fund size opens up the rest of the LP base.

Emerging manager

A GP raising Fund I, II or III. Some FoFs cap their definition at Fund III; others (Cendana) treat Fund I as a separate "nascent manager" sleeve.

DPI, TVPI, IRR

Distributed-to-paid-in (cash returned), total-value-to-paid-in (cash plus marks), internal rate of return. DPI is the test FoFs underwrite hardest in 2026, and TVPI has lost credibility.

J-curve

The first 3-6 years of negative net returns in a venture fund's life before exits start clearing. A FoF that holds 20 funds rides 20 simultaneous J curves.

Fee-on-fee

The structural objection that LPs pay 2/20 to the FoF's underlying GPs and another ~1/10 to the FoF itself.

Capital call lag

The window between LP commitment and actual wire. FoFs typically call capital quarterly; emerging GPs shouldn't plan around immediate liquidity.

Primary vs secondary commitment

Primaries fund new vintages directly; secondaries buy existing LP positions at a discount. Most first-time-friendly FoFs run primary-heavy.

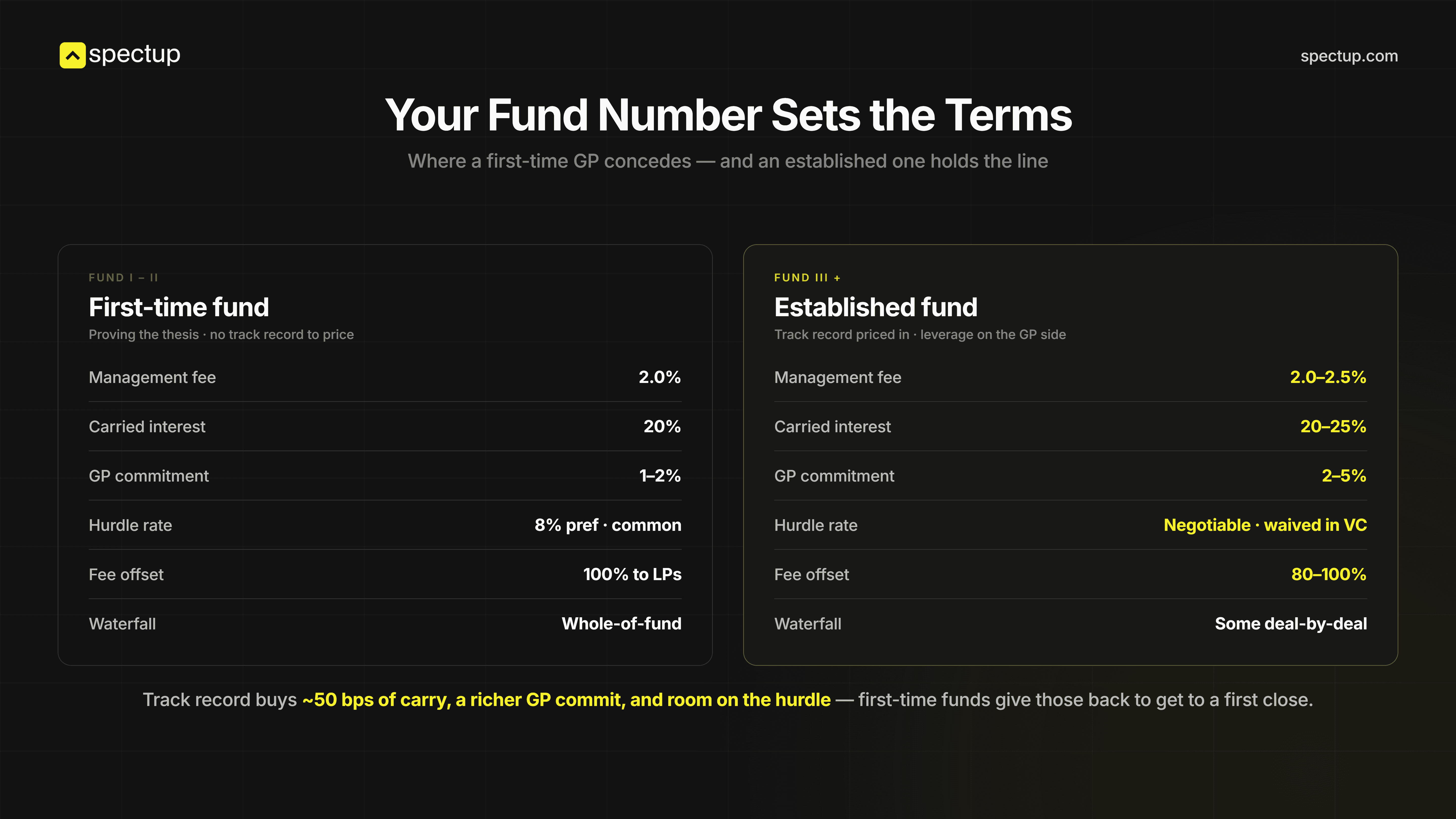

GP commit

The GP's own check into the fund. FoFs expect 1-5% of fund size as GP commitment, more for first-time managers signalling skin in the game.

What is a fund of funds in venture capital?

The short answer: a fund of funds vehicle in the venture capital market is a pooled fund that takes capital from limited partners and allocates it across 20-40 underlying VC funds, rather than investing directly into startups.

The LP pays the FoF's fees (typically 0.5-1% management plus 5-10% carry) on top of the underlying funds' standard 2/20. In return the LP gets manager diversification, access to closed funds, and emerging-manager exposure they couldn't source alone.

Mechanically a FoF runs three commitment types, each with its own diligence rhythm that emerging managers should understand alongside related fundraising mechanics, like how to raise venture capital:

Primary commitments fund new vintages directly. This is the bulk of most FoF books and the channel emerging managers care about.

Secondary commitments buy existing LP positions from other allocators looking to exit early, usually at a 10-30% discount to NAV.

Co-investment sleeves let the FoF write direct startup checks alongside its underlying GPs, capturing direct-deal economics without management fees.

The first two sentences of an FoF's marketing deck are about manager selection. The deeper read is more interesting.

A FoF is functionally a wholesale buyer of GP track records. They run the manager-selection process that a small endowment or single-family office can't staff for themselves. Carta's primer on the structure captures the LP-side trade clearly: you pay the second fee layer to outsource the work of finding, diligencing and monitoring 20+ GPs.

For an emerging GP raising into FoFs, this reframe matters. You aren't pitching a strategic financial partner; you're selling a track record to a buyer whose entire business model is buying track records well.

The pitch is structural, not aspirational.

Why did anchor limited partners go quiet in 2026?

The macro context is sharper than most GPs want to admit. Q1 2026 PitchBook-NVCA Venture Monitor data shows the LP base inverted.

Five firms (a16z, Sequoia, Lightspeed, Accel and one peer) took 73.1% of all LP capital raised in the quarter.

The next ten took 15.4%. Every other US venture firm, with hundreds of vehicles in the market, split 11.5%.

The downstream effect on emerging managers is brutal. Pension funds, once the workhorse for $50-100M Fund II commitments, pulled back across the board. State pensions cited illiquidity exposure.

Corporate pensions cited rate-environment rebalancing. Several went passive on alts entirely.

Endowments did the opposite of what the Yale Model predicted: they consolidated into the same five top-quartile names rather than backstopping the long tail. Sovereign wealth pivoted toward direct co-invest, not blind-pool commits.

The one institutional class that did not retreat from emerging managers is fund-of-funds venture capital programmes. The fund-of-funds venture capital base treats Fund I and Fund II as a mandate, not a favour.

Emerging-manager exposure is part of the explicit mandate of most VC FoFs. Cendana, Recast, Sapphire Partners, and Top Tier – these vehicles raise from LPs who specifically want the emerging-manager bucket they can't source themselves. Pulling back from Fund I would break the FoF's own fundraising thesis.

That's the structural reason a FoF still takes the first meeting when a pension fund doesn't return the email.

It's also why a sub-$100M emerging manager today should treat FoFs as the lead institutional channel, not the backup. The pension-fund-first sequence inherited from 2019 playbooks is over.

LPs: stop letting GPs raise on TVPI, underwrite on cash returned. Half the managers in Europe wouldn't raise Fund IV under that rule. The flip side for emerging GPs is that the FoF base actually applies that test, which is exactly why the FoF base is the right room for a clean first-fund pitch.

Which fund of funds actually backs first-time vc managers?

This is the FoF directory table competitors don't have. The directories you'll find on most explainer pages either list mega-allocators that mostly won't back Fund I (HarbourVest, Pantheon, and Pathway) or stop at three or four names.

Below is the working venture capital fund of funds list I keep updated for spectup placement mandates, with the first-time fund posture made explicit.

FoF | HQ / Geography | Typical commit (emerging) | First-time-fund posture | Example-backed managers |

|---|---|---|---|---|

Cendana Capital | San Francisco / global seed | $10-20M Core; $1M "nascent" bets | Yes, Fund I is friendly. | IA Ventures, Forerunner, K9, Susa |

Recast Capital | New York / emerging-manager focused | $3-10M | Yes, Fund I and II | Diverse-led seed funds; Lerner-network |

Screendoor | New York / under-represented GPs | 10% minimum of fund size | Yes, Fund I only | ~25 first-time GPs since 2020 |

Sapphire Partners | Menlo Park / global early-stage | $15-25M into $40-100M+ funds | Selective, typically Fund II+ | Data Collective, Felicis, Defy |

Top Tier Capital Partners | San Francisco / multi-vintage | $5-20M | Selective, emerging + established | Multi-strategy venture book |

Foundry Group Pathfinder | Boulder / network-driven | $3-10M | Yes, first-time friendly | Foundry-adjacent seed managers |

Industry Ventures | San Francisco / secondaries-heavy | $5-15M primary; larger secondary | Selective, prior-fund track-record bias | Mixed primary/secondary book |

StepStone (formerly Greenspring) | La Jolla / institutional scale | $10-25M+ | Fund II+ only | Established managers; rare Fund I |

HarbourVest Partners | Boston / global mega-allocator | $10-25M typical, larger on flagship | Fund II+ only | Established managers, primary + secondary |

Isomer Capital | London / European venture | €3-8M | Selective, European Fund I and II | European seed and Series A managers |

Molten Ventures (FoF programme) | London / European growth | €5-15M | Selective, Fund II+ bias | European growth-stage VCs |

EIF ETCI 2 | Luxembourg / pan-European venture capital fund-of-funds | €30-200M per fund (growth-stage) | Growth-stage only, not Fund I seed | ~100 European growth VCs (target) |

Al Waha Fund of Funds | Bahrain / MENA | $5-15M | Yes, MENA-focused Fund I is friendly. | BECO Capital, MEVP, 500 MENA, Shorooq |

Mubadala Capital (FoF sleeve) | Abu Dhabi / sovereign-linked | $15-50M+ | Fund II+; selective on Fund I | Global tech VC managers |

How to read this table?

"Yes" in the first-time-fund column means the FoF has a documented Fund I programme and writes Fund I anchors as part of its normal book.

"Selective" means Fund I is possible but uncommon and usually requires a strong reference from a backed GP.

"Fund II+ only" means don't waste the meeting if you're pre-Fund II.

The check sizes are working ranges from the last 18 months of placement work and from public sources where available: Cendana's stated approach, Emerging Manager Monthly's profile of Screendoor's 10% anchor framework for first-time managers, Sapphire Partners' published thesis and MENAbytes' reporting on Al Waha's MENA fund of funds programme.

The named-protagonist scene worth carrying forward: when Cendana closed $470M in 2023 specifically to back seed-stage GPs, the founder team led by Michael Kim explicitly carved out a "nascent manager" sleeve for $1M-scale bets into pre-Fund I GPs with no institutional anchor yet.

That sleeve still runs. Most managers assume Cendana only writes the $10-20M Core cheque; in reality, the nascent sleeve is the right opener for a pre-Fund I GP with no institutional anchor.

The fund of funds diligence process venture capital really runs

Most GPs walk in expecting either a fast family-office yes or a slow pension drag.

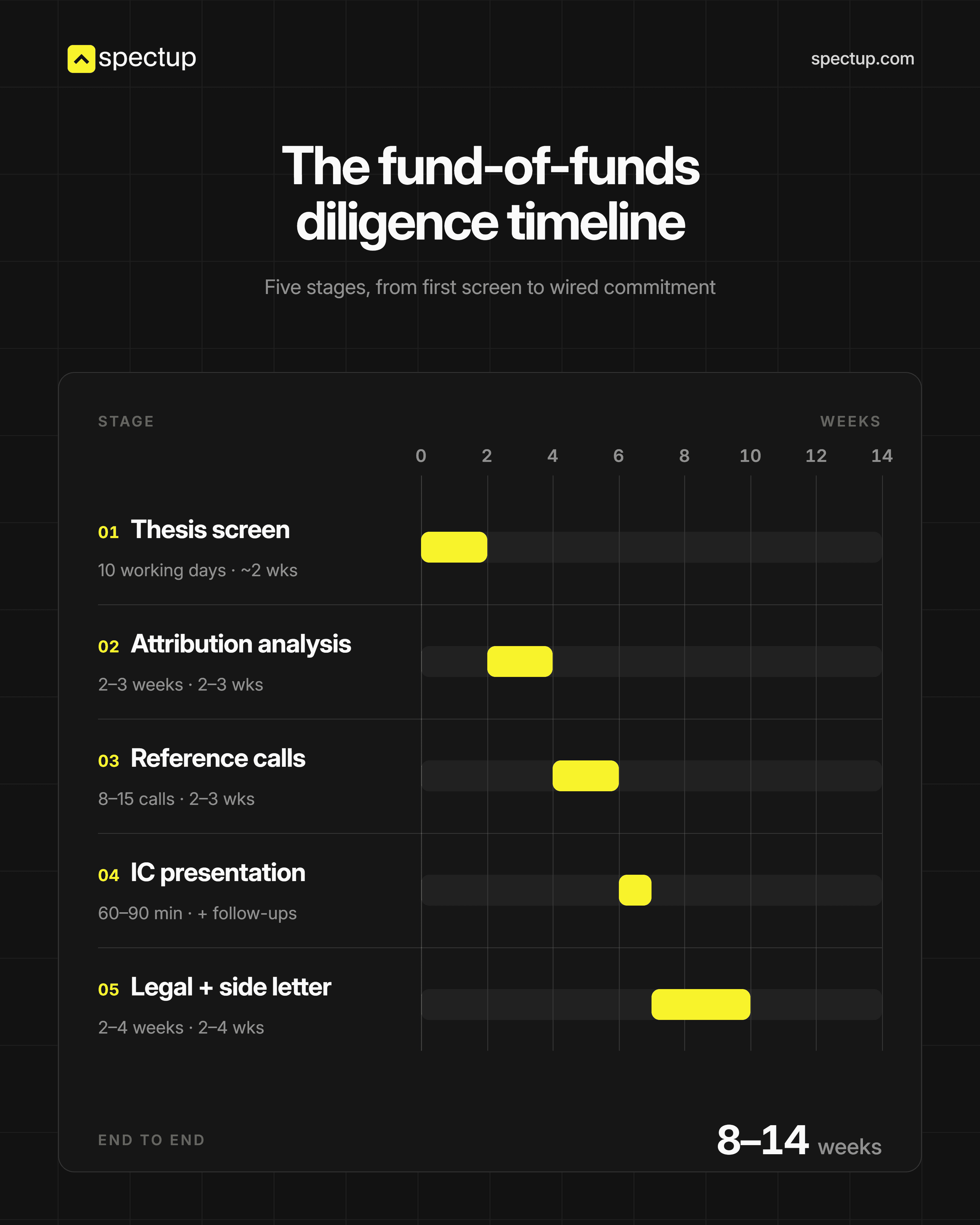

The fund of funds diligence process venture capital programmes actually run sits in between 8 and 14 weeks from first meeting to IC decision.

Compare against the alternatives below.

LP class | First meeting to IC | Diligence depth | Reference calls expected |

|---|---|---|---|

Family office (single) | 4-8 weeks | Thesis + GP fit | 2-4 references |

Fund of funds | 8-14 weeks | Full attribution + reference battery | 8-15 references |

Endowment (small) | 3-6 months | Full attribution + market sizing + ops DD | 10-20 references |

Corporate pension | 6-12 months | Full DD + investment consultant + board cycle | 15+ references |

HNW / accredited individual | 2-6 weeks | Light, narrative-driven | 0-2 references |

The FoF cycle moves through five distinct stages, each with its own kill point.

Thesis screen

The FoF reviews a 2-page teaser plus prior-fund track record packet. Most rejections happen here, usually within 10 working days. The kill point is the "wrong stage" or "no differentiated thesis".

Attribution analysis

The FoF rebuilds your prior deals from scratch:

Were you actually the lead voice on the wins or a co-investor along for the ride?

This stage takes 2-3 weeks and is the silent killer for spinout GPs from larger funds.

GP reference calls

8-15 calls with founders, co-investors, prior LPs.

The FoF is listening for one thing: do other people in the market actually want to work with you again?

IC presentation

A 60-90 minute IC paper plus a live presentation.

Two or three rounds of follow-up questions, then the vote.

Legal + side letter

2-4 weeks of LPA review, MFN negotiation, and side letter drafting.

Most first-time managers underestimate the side letter back-and-forth, which can stretch the timeline.

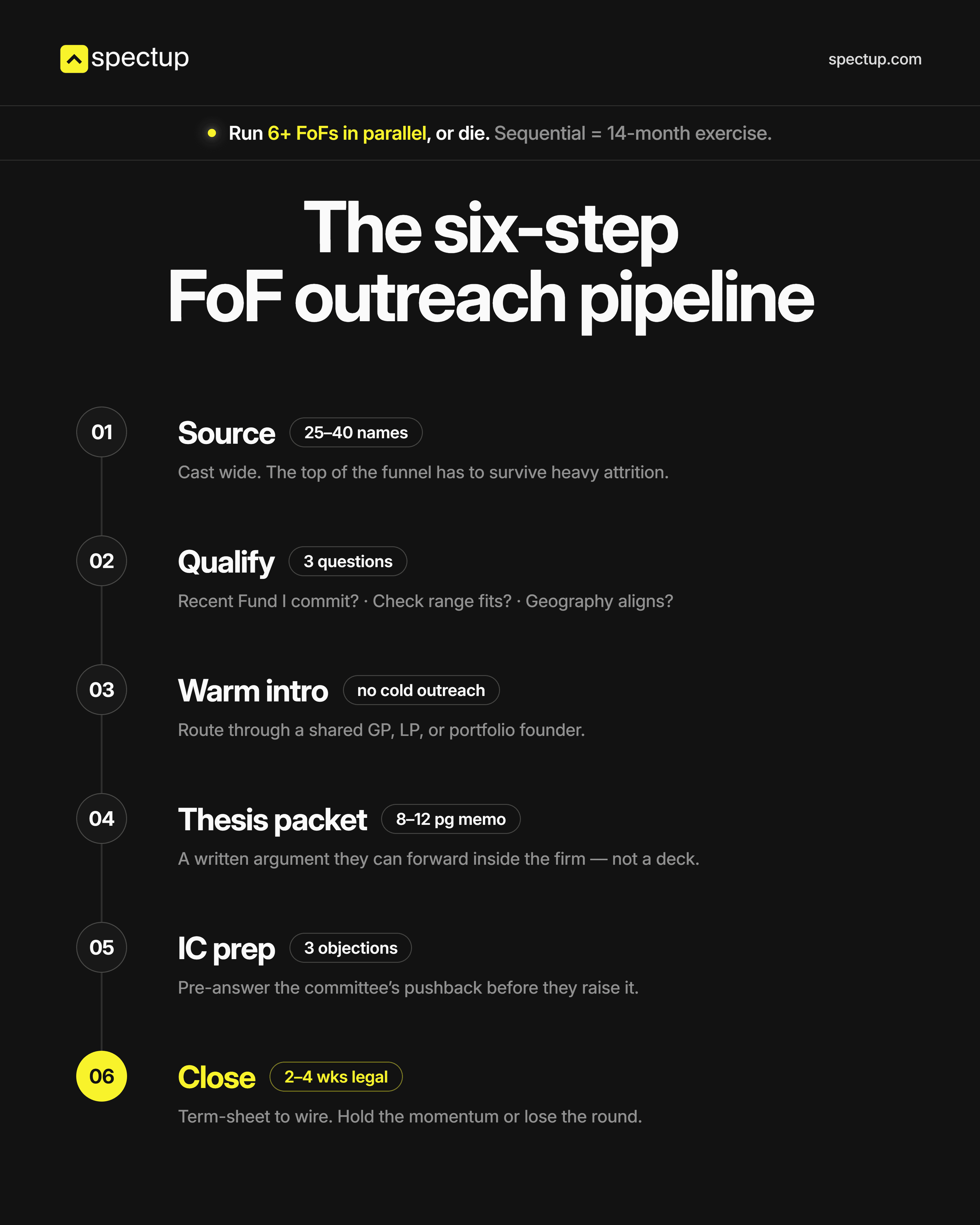

The implication for pipeline construction is simple: budget 12 weeks per fund of funds venture capital target as a baseline. A six-FoF pipeline run sequentially is a 14-month exercise. Run them in parallel or die.

Sapphire Partners' OpenLP commentary on emerging manager diligence backs this up: they say explicitly that GPs who run FoFs sequentially "lose the LP attention war". The Screendoor underwriting framework Lisa Cawley described on the Swimming with Allocators podcast is even more direct: their reference-heavy process compresses to 10 weeks for warm-intro GPs and stretches past 16 for cold inbound.

On spectup mandates, the pattern is consistent. Warm-intro first meetings convert to advanced diligence at roughly 4-5x the rate of cold inbound.

The same FoF runs the same 14-week cycle either way. The cold case just adds a 6-week "who are you really?" pre-screen that the warm case skips entirely. The placement work itself is largely about engineering the warm path.

The three objections every fund of funds venture capital partner will raise

Thesis weakness rarely kills FoF conversations on its own. Three structural objections do.

Most emerging GPs fumble all three because the rebuttals are tribal knowledge rather than published advice. Below is the working playbook.

Objection | What the FoF actually means | GP-side response (with math) |

|---|---|---|

DPI exposure | Your prior funds haven't returned cash; the marks are paper. We can't underwrite a track record we haven't seen liquidate. |

|

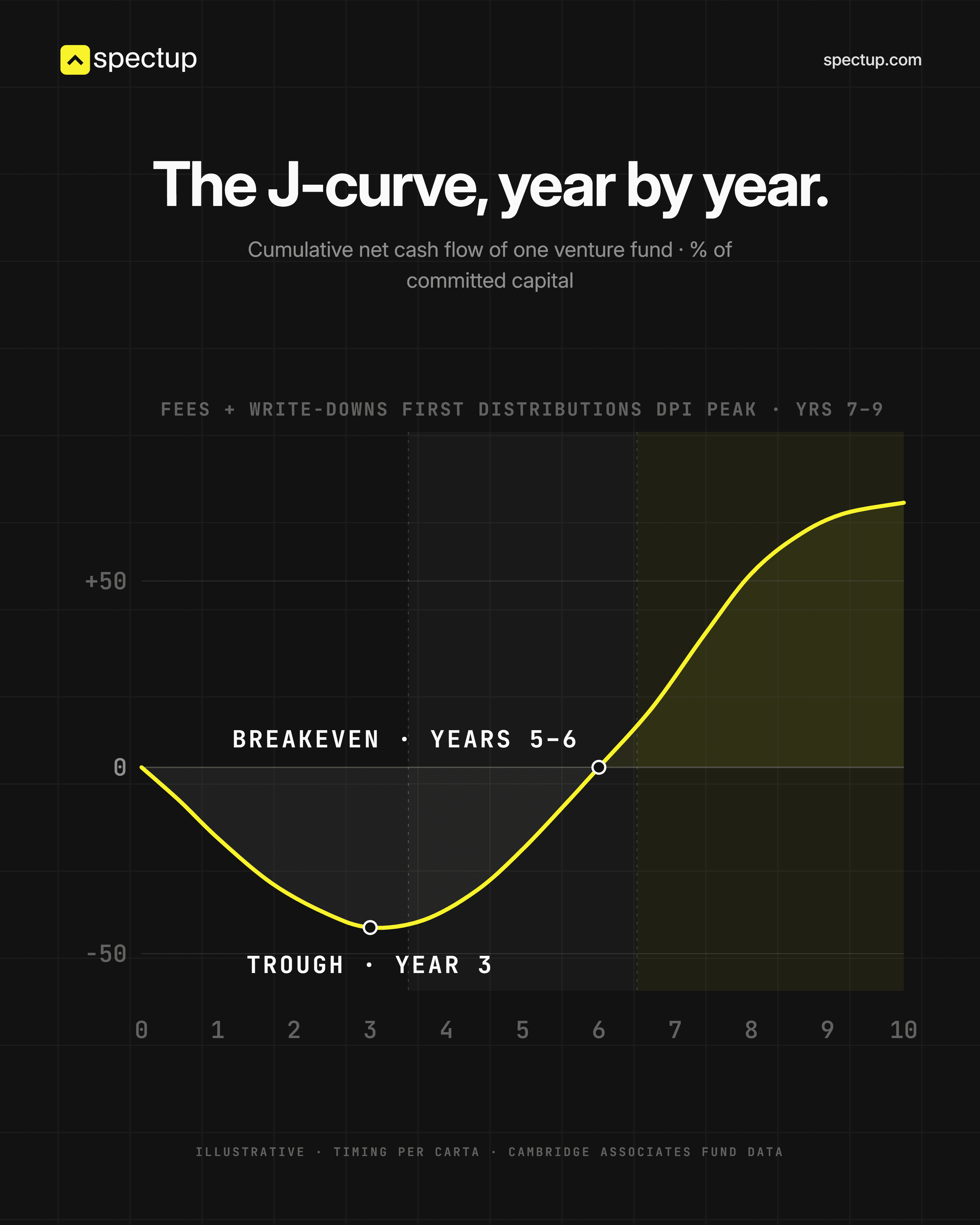

J-curve depth (j curve venture capital fund of funds) | We will be underwater for 5-6 years before any distribution. Our LPs see the mark, not the IRR forecast. |

Typical seed funds hit the J-curve trough at year 3, recover at years 5-6, and peak at DPI years 7-9. Quantify the trough depth in basis points of fund size, not in narrative. |

Fee-on-fee (fund of funds fee on fee venture capital) | Our LPs pay us 1/10, plus your 2/20. That is 3/30 effective. Defend the second fee layer. | The reframe: the FoF's fee buys 20+ manager selections their LPs can't make themselves. The right comparison isn't "your 2/20 + our 1/10 = 3/30". It's "our LPs paying 3/30 net for a 2.5x return vs paying 0/0 for self-allocation at 1.4x".

|

The meta-point on all three:

FoF partners have heard every GP rebut DPI poorly.

The bad rebuttals all sound the same. "TVPI tells a different story," "the exits are coming in 2027," our model says.

The good rebuttals concede the structural concern first and then bring numbers the FoF can't dispute.

A FoF that hears "I know DPI is the right test, here's the cohort math against the median" will sit forward in the chair. A FoF that hears "DPI doesn't really capture the value creation" will tune out.

One pattern from a recent placement mandate: a Fund II GP rehearsed the fee-on-fee rebuttal with us before an IC presentation. We ran the math against the FoF's own published net-return distribution.

The GP went into the IC with a 90-second answer ready instead of the usual 4-minute defensive monologue. The FoF voted yes that week. The cap commitment was $8M.

GPs raise Fund III on paper markups from Fund I. TVPI feeds the next fundraise, DPI tells you whether the model works. The two have decoupled, and almost no one is calling it; for a FoF underwriting your Fund II, the only safe assumption is that the test will be cash returned, not paper.

How much will a fund of funds actually write into your fund?

Check sizes across the FoF base vary more than most directories suggest. The full range I see across active FoFs: $1M nascent-manager bets to $25M anchor positions in established Fund III vehicles. Any working venture capital fund-of-funds list has to track these ranges per name, not in aggregate.

Anchor norm for Fund I from a first-time-friendly FoF is:

$5-15M

Often capped at 10-20% of total fund size

Cendana's published Core position is $10-20M.

Screendoor's stated anchor minimum is 10% of fund size

The cheque-size question is also where the venture capital fund of funds vs direct investing comparison gets concrete: a FoF anchor of $5-15M into your Fund I is capital you'd never raise as 30 separate direct-startup tickets from the same allocator.

FoF | Typical commitment into Fund I | Typical commitment into Fund II+ | Cap as % of total fund |

|---|---|---|---|

Cendana Capital | $1-5M nascent / $10-20M Core | $10-20M | 10-20% |

Screendoor | 10% minimum (often $3-5M) | n/a (Fund I only) | 10% minimum |

Recast Capital | $3-10M | $5-15M | ~10% |

Sapphire Partners | Selective only, typically $10M+ | $15-25M | 10-15% |

Top Tier Capital Partners | $5-15M (selective) | $10-25M | 10-15% |

HarbourVest / StepStone | Rare | $15-25M+ | 5-10% |

Isomer Capital | €3-8M | €5-12M | 10-15% |

EIF ETCI 2 | n/a (growth-stage only) | €30-200M | Up to 25% |

Al Waha (al waha venture capital fund of funds) | $5-15M | $10-20M | ~15% |

The EU exception is worth calling out in any FoF sizing analysis. EIF ETCI 2 will write into larger growth-stage funds (€300M-€1B+), not Fund I seed vehicles.

According to Sifted's coverage of the launch confirms the per-company check ceiling rises from €60M (ETCI 1) to €200M (ETCI 2). Emerging managers shouldn't pitch ETCI 2 expecting a Fund I anchor. Pitch Isomer or Molten instead, or pitch ETCI 2 when you reach the growth stage.

Closing math worth doing aloud. A $30M Fund That I win a single $5M FoF anchor is one-sixth of the way to close before any HNW or family-office work.

A $40M Fund I that win two FoF anchors at $5M each is at $10M / 25%, typically enough to trigger the first close and open up the rest of the LP base. The pull-through effect is real. One named FoF anchor changes the conversation with every subsequent LP you talk to.

The european shift: what EIF ETCI 2 means for european fund of funds for emerging vc managers

The single biggest LP-side event of the European cycle is happening in the next twelve weeks. The European Investment Fund's ETCI 2 programme closes its €15B pan european venture capital fund-of-funds in summer 2026, anchored by €1.25B from EIF and EIB directly. It's the single largest pan european venture capital fund-of-funds vehicle in the market and reframes the entire fund-of-funds venture capital map for European GPs.

The mandate is to back roughly 100 European growth-stage VCs and release €80B in scaleup financing across the continent over the next decade.

The structural change matters more than the headline number.

ETCI 1's per-company investment ceiling was capped at €60M, which forced GPs into small-fund discipline but locked European companies out of the growth-stage capital available to US competitors.

ETCI 2 raises that ceiling to €200M per company.

European GPs can finally write €25-50M Series B and C cheques without syndicate-stacking five smaller funds together.

For emerging managers, the read is two-sided. ETCI 2 isn't a Fund I anchor. The fund-size minimums for ETCI 2 commitments will exclude seed-stage Fund I vehicles.

The opportunity is for emerging growth-stage GPs who can credibly raise €300M+ debut funds or for Fund II/III graduates from the seed-stage to growth-stage trajectory. Map yourself accordingly.

European founders also need to read the parallel co-investment trend. Institutional Investor's reporting on the family-office direct-deal pivot reported that 83% of family-office startup deals are now co-investments or club deals, not blind-pool fund commitments.

Family offices that used to anchor small EU funds have pivoted to writing direct checks alongside named GPs. The implication for first-time European GPs: the family-office anchor that backstopped European Fund I rounds in 2018-2022 is structurally weaker now. The replacement is a tiered LP pipeline.

I call this the Tiered LP Pipeline for European emerging managers:

Anchor-stage FoF (Isomer, Molten) for the first 30-40% of fund close

ETCI 2 for any growth-stage step-up vehicle

Family offices for fill-in commitments at 5-15% of fund

Pitch each tier with the structure it wants:

Anchors want institutional-grade attribution

ETCI wants European policy alignment

Family offices want sector affinity

Most founders assume one pitch deck travels across all three LP classes; in practice, the same memo gets rejected by the FoF, ignored by ETCI, and read politely by the family office. One deck for all three is the most common failure mode I see on European mandates.

How to pitch a fund of funds as an emerging manager: the outreach process?

How to pitch a fund of funds as an emerging manager comes down to one rule:

Treat the FoF pipeline like a sales process or you'll lose the LP-attention war by month four

Targeting the top venture capital fund of funds at random doesn't work, because every name on that shortlist has its own thesis, geography and check-size grid you have to qualify against first. The mechanics that work, in order:

Source

Build a long list of 25-40 FoFs from public directories, AltExchange, PipelineRoad, Crunchbase News, and the named directory above.

Filter for check size, geography, stage and first-time-fund posture.

Qualify

For each FoF, ask three questions before any outreach.

Has the FoF closed a Fund I commitment in your stage in the last 18 months?

Does your fund size sit within their stated check range?

Is your geography on their map?

Warm intro

80%+ of FoF first meetings come from a backed GP's introduction.

Spend the first month of fundraising sourcing intros, not pitching.

The Founder Institute LP-matching guide notes that warm intros raise first-meeting conversion rates roughly 4-5x against cold inbound.

Thesis packet

8-12 page memo

Full track-record attribution by deal

Portfolio construction model

GP commit and team detail.

Not a pitch deck. A FoF reads a memo, then asks for the deck if they want the live pitch.

IC prep

Write the IC paper for them

Anticipate the three objections (DPI, J-curve, fee-on-fee) with the math ready

Rehearse the 60-90 minute presentation with a friendly LP before the real one.

Close

Capital call schedule, side letter, MFN negotiation.

Plan 2-4 weeks of legal turnaround

Most first-time managers underestimate the side letter and start drafting the day after the IC vote.

The cadence that ships on the fund of funds venture capital mandates we run: 40+ tracked LP calls per week across the live portfolio, with warm leads worked every 2-3 weeks across a 9-12 month full close.

Pipeline reviews are weekly, not monthly. The placement model that doesn't ship is the one that treats FoF outreach as a series of one-off pitches rather than a managed multi-quarter campaign. A disciplined private placement agent runs this as a process, with the same weekly review rhythm a startup uses for its sales pipeline.

One scene worth carrying. On a recent emerging-manager mandate, a first-time European GP came to us with a target list of 14 FoFs and a "warm intro" path mapped for 11 of them.

We rebuilt the qualification filter, and four of the 14 were structurally wrong (US-only, $50M+ fund minimums, secondaries-only). The path collapsed to seven targets.

We added six replacements from the Al Waha / Isomer side of the map, with the Al Waha venture capital fund of funds as the obvious MENA opener for any GP carrying a regional thesis. The GP closed the FoF anchor in week 19, a $6M check that pulled three family offices in within the next 30 days. The original 14-name list would have run out of time.

The fund size most first-time gps pick is the one that kills the raise

Here's the take I've got the most pushback on this year, and I'll say it anyway. The right Fund I target size in 2026 is $25-40M, not the $75-100M most first-time GPs put on the cover slide.

The industry default is to raise the biggest fund your thesis can defend. I think that's wrong for the 2026 cohort, and the math is what convinces me, not the vibe.

At $30M a single FoF anchor of $5-10M closes the raise to 25-35% before you talk to a single family office. At $90M the same anchor is 6-11% of the fund.

You still need a pension or large endowment ticket to clear the first close at the bigger size, and that LP class isn't writing into Fund I right now. The bigger fund isn't more ambitious. It's structurally unfundable at this vintage.

The vanity of a $90M Fund I cover slide is the cheapest way I've seen first-time GPs burn 18 months of runway. A $30M Fund I that closes in nine months returns more carry to the GP than a $90M Fund I that stalls at $42M and gets pulled.

The scene that made me stop pitching the bigger number

One GP-Sigma we worked with last year came in wanting an $85M Fund I. Ex-operator, two unicorn angels on the prior book, thesis was strong and the deck was clean. The target LP list was 80% pensions and university endowments.

We modelled the close two ways.

At $85M, the math required two pension anchors at $15M each, and the realistic conversion rate on that LP class in 2026 is roughly one in fifteen.

At $35M, the same GP needed one FoF anchor at $7-10M and a family-office stack of 8-12 tickets at $1-3M each.

Same carry economics for the GP at 2/20, same fund management infrastructure, and a wildly different probability of close.

The GP took the smaller number. First close hit at $22M in month seven, anchored by a $6M FoF check. Final close landed at $38M in month thirteen.

The pushback I get from FoF allocators on this is fair. A $30M Fund I makes 18-22 investments at a $1.2-1.5M average, which means the GP either calls follow-on capital from a pro-rata SPV or skips pro-rata entirely. Both compress returns relative to a $90M fund running concentrated bets with reserves.

I hear that. I still think the $30M closes and the $90M doesn't, and a closed fund beats an unclosed one every cycle.

How spectup runs emerging manager fund of funds placement?

Emerging manager fund of funds placement is our core work. Most spectup mandates are first-time GPs targeting the venture capital fund of funds base for an anchor LP commitment, and we're running ten live placement mandates right now with the working ICP crystallised as "growth-stage tech companies and fund GPs raising $2-50M in venture and growth". The emerging manager fund-of-funds book is where most of those mandates close their anchor ticket.

The pattern across the GP mandates is consistent:

Emerging managers come in with a target list dominated by the wrong LP class (pensions, large endowments, and sovereigns that have all paused)

The first 30 days of the engagement are spent rebuilding the list around the top venture capital fund of funds programmes and the wider fund of venture capital funds map that actually writes Fund I cheques.

A well-built fund's shortlist of venture capital funds is the deliverable that resets month two of the raise.

The work itself is two-track.

The pipeline track is sourcing, qualification, warm-intro engineering and weekly tracked outreach.

The materials track is the thesis packet, the cohort cash-flow model, the IC paper template and the three-objection rebuttal scripts. Both tracks ship in parallel from week one.

A fundraising consultant who only ships one of the two tracks (most ship materials; very few ship the pipeline) leaves the GP doing the harder half alone. That's the failure pattern that surfaces in month five.

If you're an emerging manager with a thesis worth backing and a prior track record that holds up to attribution, and you want a tiered LP pipeline that opens with FoF anchors rather than ends with them, book a call with me.

The placement work and structured investor outreach service are full-cycle, not packet-only, and we maintain a working reference on VC fund structures in 2026 and the limited partnership agreement terms LPs negotiate for GPs designing first close mechanics.

Where would I actually focus your fund-of-funds venture capital outreach right now?

The reflex I see most often from first-time GPs is to keep dialling the same pension fund contact list that worked for a friend's Fund I in 2021. That list is dead for 2026 vintages at sub-$100M. The FoF base is the only LP class still writing live anchor checks at this size.

The five firms that took 73.1% of Q1 LP capital aren't coming for your fund either way. The institutional class that did stay open is fund-of-funds venture capital, and the playbook for winning them is closer to a sales process than a relationship game. Three working documents earn their place on your desk week to week:

A current venture capital fund-of-funds list,

A top venture capital fund of funds qualification grid

A fund of venture capital funds mapped by geography

My honest read after working this market: the GPs who close their first close in 2026 are running a tiered LP pipeline with FoFs as the named anchor, not the backup. They run 6-10 FoF conversations in parallel, not in sequence, and they put MENA anchors like Al Waha venture capital fund of funds on the same target sheet as European names like Isomer or Molten.

They walk into IC presentations with the DPI / J-curve / fee-on-fee rebuttals already on the page, not extemporised. They pre-built the warm-intro path for 80%+ of their target list before sending a single cold email.

If you're still designing your fundraise around pension and endowment outreach because that's the LP class you understand best, you're designing for the market that existed three years ago. Rebuild the target list around FoFs first. The numbers will tell you the rest.

Concise Recap: Key Insights

Five firms took 73% of Q1 capital

Direct institutional channel froze for sub-$100M emerging managers. FoFs are the LP class that stayed open and still write Fund I anchors.

FoF diligence runs 12 weeks, not 12 months

Run six FoFs in parallel across a 9-12 month close. Sequential outreach loses the LP attention war by month four.

Answer the three objections with math

DPI, J-curve and fee-on-fee kill more FoF conversations than thesis weakness. Concede each structurally, then bring the cohort numbers and the vintage-by-vintage attribution.

Frequently Asked Questions

What is a fund of funds in venture capital?

A fund of funds in venture capital is a pooled vehicle that takes capital from limited partners, then allocates across 20-40 underlying VC funds rather than investing directly into startups. The LP pays two fee layers: the FoF's 0.5-1% management fee and 5-10% carry, plus the underlying funds' 2/20. In return the LP gets manager diversification and emerging-manager exposure they couldn't source alone.