Table of Content

Summary

Capital without giving up equity

Non-dilutive funding provides growth capital while preserving your ownership stake. You keep control of the company and avoid diluting founders and early investors.

[01]

Multiple paths beyond venture capital

Venture debt, revenue-based financing, grants, and loans offer alternatives to VC. Each has different costs, terms, and eligibility criteria that match different company stages.

[02]

Cost is explicit and manageable

RBF charges 2-10% of monthly revenue with a 1.5-2.0x repayment cap. Venture debt carries interest rates of 10-15%. You know the cost upfront, unlike equity dilution.

[03]

Eligibility is built on traction, not potential

Lenders want revenue history, consistent customer base, and clear unit economics. You need to prove the business works, not convince investors it will.

[04]

Most founders combine sources strategically

Smart founders stack multiple non-dilutive sources: a venture debt facility, RBF line, plus grants. This compounds runway without multiplying dilution.

[05]

Every founder I talk to treats equity like it's the only currency in fundraising. It's not.

What is non-dilutive funding?

A founder raises a venture capital round, and the investor takes 25% equity. That's dilutive. The founder loses a quarter of the company.

Another founder takes venture debt or revenue-based financing instead. The loan gets repaid, the lender exits, and the founder owns 100% of the business. That's non-dilutive.

The difference is structural. Equity is permanent.

It dilutes every future round

Debt expires

The borrowed capital is repaid, and the relationship ends.

Your cap table doesn't change.

If you're unfamiliar with how dilution works, our guide on cap table management shows the math.

Why does non-dilutive funding matter in 2026?

Three forces converged in 2025 that made this category essential.

First: The venture debt market hit $27.8 billion in 2025 and is growing 6-7% annually. The capacity exists.

Second: European funding rounds grew 32% in median size between 2024 and 2025, with the EU Commission allocating €1.1 billion for France and €400 million for Greece in cleantech startup funding. The money is flowing to founders who can move fast without waiting for a traditional Series A.

Third: Founder expectations shifted. Higher equity valuations mean higher dilution. A Series A in 2026 costs you more equity than it would have in 2021. Founders are opting out.

Revenue-based financing is growing at 62%+ annually and reached $9.77 billion in market volume in 2025. The SBIR/STTR program, which distributes $4+ billion annually in non-dilutive grants, was just reauthorized through 2031 with new $30 million strategic breakthrough awards. Venture debt is recovering: deal volume in 2025 finished 11% higher than 2024.

This isn't fringe anymore. It's mainstream capital. At spectup, we're seeing more founders ask about non-dilutive options before they even start a pitch deck.

Key terms you should know

Venture debt:

Debt financing from specialised lenders targeting venture-backed startups. Typically comes with warrants that give the lender the option (not the obligation) to buy equity at a set price. Repaid on a fixed schedule, usually over 3-4 years.

Revenue-based financing (RBF):

Lender receives a fixed percentage of monthly revenue (typically 5-10%) until they've recouped the loan amount plus a multiple (the repayment cap, usually 1.5x-2.0x). No fixed payment date, no dilution, no personal guarantee required.

Factor rate:

In RBF, the total amount you repay relative to capital borrowed. A 1.5x factor rate means you repay 1.5 times the original advance. A 2.0x cap means you owe no more than twice the loan, even if revenue grows dramatically.

SBIR/STTR:

Small Business Innovation Research and Small Business Technology Transfer programmes. Federal grants distributing $4+ billion annually to small companies developing novel technology. No repayment required, no dilution.

Dilutive vs non-dilutive funding at a glance:

Dimension | Dilutive (Equity) | Non-Dilutive (Debt/Grants) |

|---|---|---|

Ownership Impact | You lose X% of the company permanently | Your ownership stays unchanged |

Cost | 20-30% per series; compounds across rounds | Explicit: 10-15% interest (debt) or 5-10% monthly revenue share (RBF) |

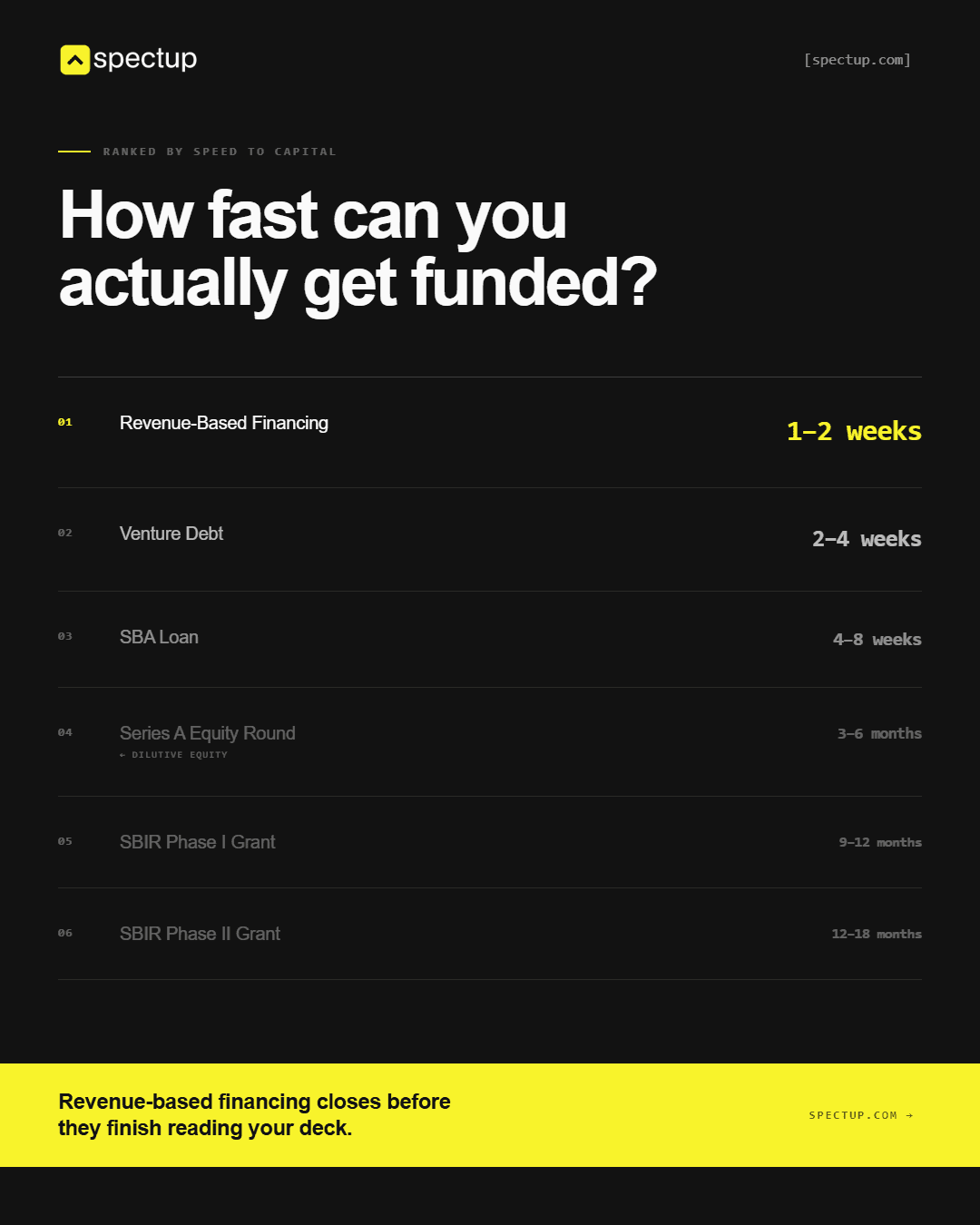

Timeline | 3-6 months; investor due diligence heavy | 2-4 weeks for venture debt; 1-2 weeks for RBF |

Control | Investor often takes board seat or governance rights | Lender has no control; purely financial relationship |

Repayment | Never. Capital is permanent. | Yes. Relationship ends when loan is repaid. |

Best for | Pre-revenue, unproven business models, longer runways needed | Revenue-generating, predictable cash flows, near-term growth acceleration |

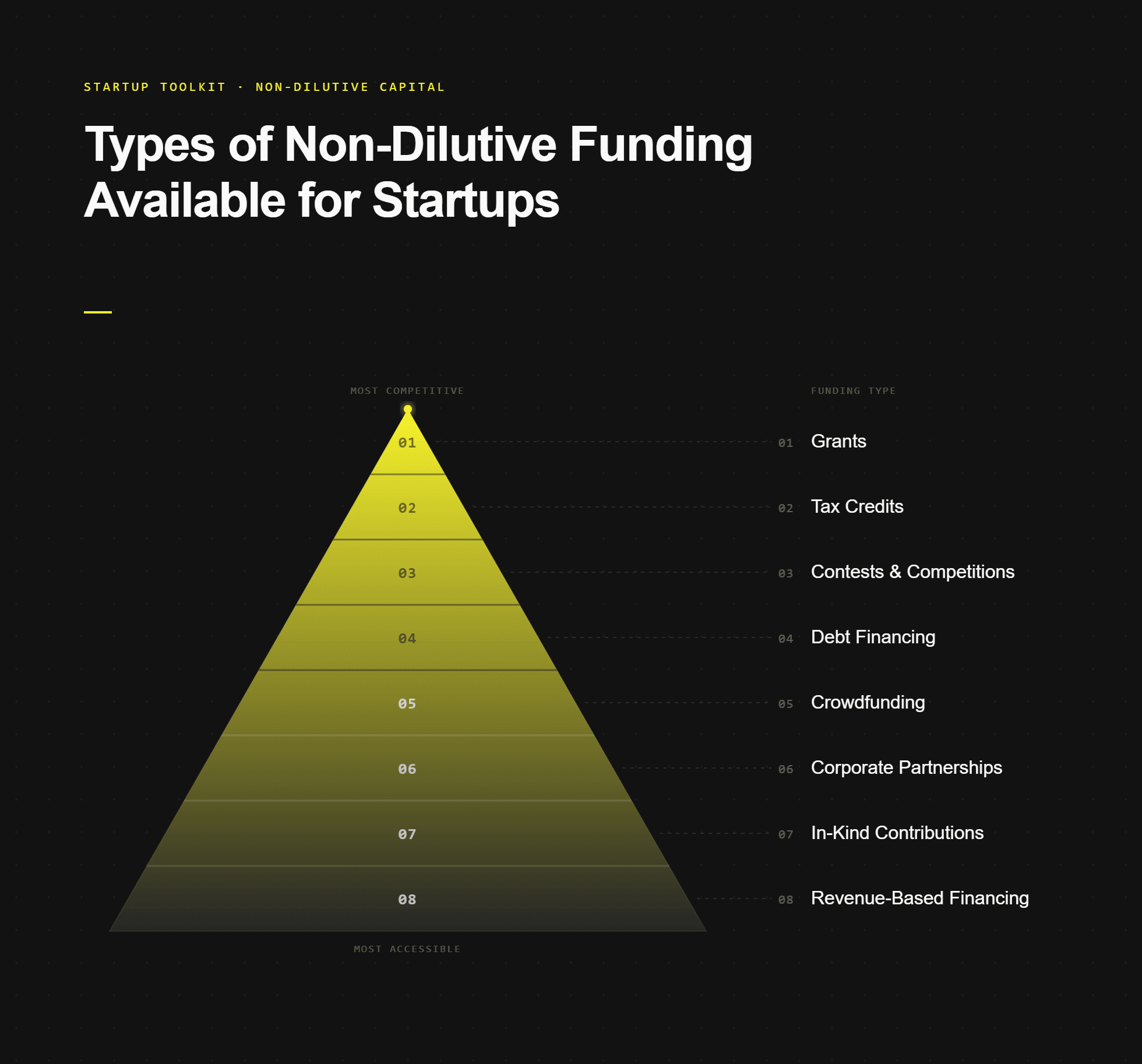

Types of non-dilutive funding

Non-dilutive capital isn't one category. It's a toolkit. Every company qualifies for different pieces depending on revenue, industry, and geography.

Venture debt

Specialised lenders (Clearco, Brex Capital, and others) lend to venture-backed startups. If you're unfamiliar with how this fits into the broader picture, our guide on venture debt financing covers the mechanics in detail. The bet is simple: the company will raise a future equity round and repay the debt first.

Typical terms for venture debt:

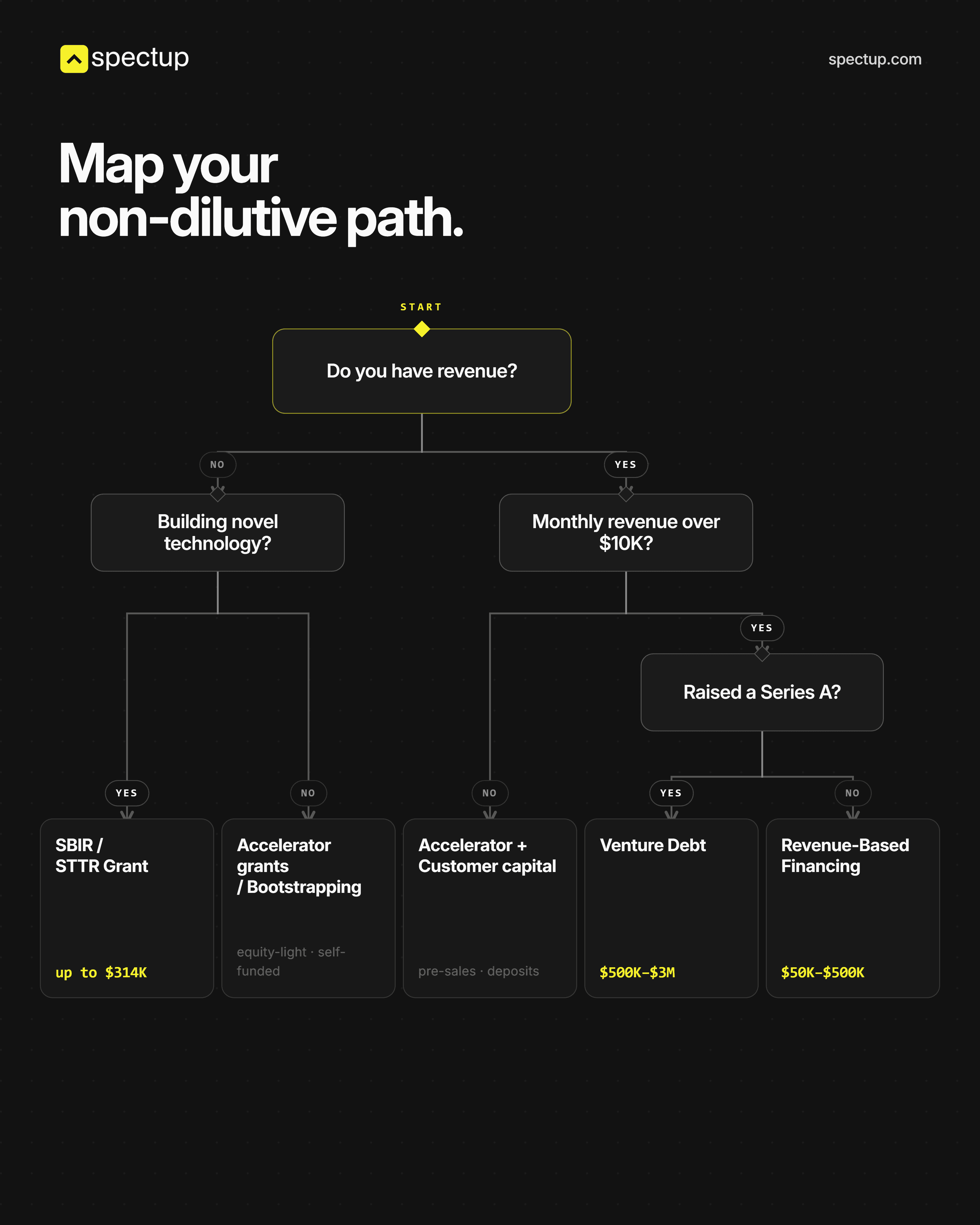

$500K-$3M

3-4 year repayment at 10-15% interest

Plus warrants giving the lender the right to buy equity at a discount.

Warrants are cheap insurance for the lender. For you, they're a tiny amount of future dilution.

Venture debt works best if you've raised a Series A or B already. Lenders want to see that professional investors believe in your company. If you haven't raised institutional capital yet, venture debt is harder to access.

Revenue-based financing

RBF is the fastest-growing non-dilutive category. Lender sends capital upfront. You repay a percentage of monthly revenue until you've paid back the advance plus the cap (typically 1.5-2.0x).

Here's the mechanic:

You raise $250K on a 2.0x cap

You owe a maximum of $500K.

If you repay 6% of monthly revenue and revenue is $50K/month, you pay $3K monthly.

When you've paid $500K total, you're done.

If revenue drops to $10K, you pay $600 that month.

The payment scales with your business.

The market is growing 60%+ annually. Clear skies capital, lighter capital, pipe, and others have built this market.

Typical range for revenue-based financing:

2-10% of revenue

1.2x-3.0x cap, depending on your risk profile.

Approval takes 1-2 weeks if you have 6+ months of revenue history.

Grants and competitions

SBIR and STTR grants distribute $4+ billion annually.

Phase I grants go up to $314K as of October 2024.

Phase II costs $600K-$2.8M over two years.

Phase III (new in 2026): up to $30M over four years for strategic breakthrough projects.

Eligibility criteria for SBIR and STTR grants:

Your company must be:

A small business (under 500 employees)

US-based

Developing novel technology.

The application is heavy. You're writing a technical proposal. Treating it like sending a pitch deck is big mistake.

Approval rate is 15-20%. But if you get it, the capital is non-dilutive and non-repayable.

A founder I worked with stacked cloud credits from AWS, a $50K accelerator grant, a $200K SBIR, and a $300K RBF line. Together: $550K non-dilutive. Zero equity given up.

What are the options beyond SBIR?

Accelerators (Y Combinator, Plug and Play, others) hand out $20K-$150K as equity-free grants.

Industry-specific competitions (AWS Startup Grants, Google for Startups, etc.) award credits and cash.

I sat with a founder from Greece who had successfully navigated the European Innovation Council (EIC) Fund grant process. The EIC covered half of their Series A round through a blended finance model, essentially a non-dilutive grant layered with an equity investment. The remaining 50% came from Greek VCs.

Bank loans and SBA loans

Traditional bank loans require collateral and personal guarantees. Hard to access without revenue history. But SBA loans (7a programme and Microloan programme) are backed by government guarantees, making banks more willing to lend to startups.

SBA 7a loans go up to $5M at rates around 8-10%.

Typical terms for bank loans and SBA loans are:

10 years for equipment

7 years for working capital

The SBA guarantees 75% of the loan, so the bank takes less risk. Approval takes 4-8 weeks and requires business financial statements.

Bootstrapping and customer capital

The most underrated non-dilutive strategy: don't borrow. Generate revenue and reinvest. We've written about bootstrapping strategies in depth. A founder with $100K in monthly revenue can self-fund a team, product iteration, and growth without raising a dime.

Customer capital is related: take pre-payments for future services. Contracts for consulting or custom development work. Annual subscriptions paid upfront. You're using your customers as informal lenders.

Bootstrapping means slower growth. But it means full ownership and no founder fatigue from fundraising. Some of the most capital-efficient companies I've worked with were bootstrapped until $5M+ revenue, then took a single strategic round.

Crowdfunding and equity alternatives

Rewards-based crowdfunding (Kickstarter, Indiegogo) isn't equity. You take pre-orders. The capital comes from future customers, not investors. It validates demand before manufacturing.

Community notes and community shares (Republic, Wefunder) let you raise from non-accredited investors without full dilution. Different structure, but less demanding than VC.

What does non-dilutive funding actually cost?

Every founder asks this question backward. They think: "Equity is expensive because I'm losing upside." Actually, equity is cheap upfront (no cash outlay) but expensive long-term. Non-dilutive looks expensive because you pay cash, but it's often cheaper when you model it out.

Venture debt costs

Interest rate: 10-15% annually

Warrant coverage: 10-25% (the lender gets the option to buy equity at a discount). This is small, but it's dilution.

Origination fee: 2-4% of the loan amount, charged upfront

Example: $1M venture debt at 12% interest, 15% warrant coverage, 3% origination fee. You pay $30K upfront (origination), then $120K annually ($10K/month) for repayment. Over 3 years, you've paid $390K total and given up warrant coverage on ~15% of your cap table.

Compare it to a $5M Series B at 20% dilution: you lose 20% equity, and $1M in valuation goes to the new investor. If your company sells for $50M, you've lost $10M in founder proceeds from that dilution alone.

Revenue-based financing costs

Monthly revenue share: 3-10% depending on risk

Repayment cap: 1.5x-2.0x (you never pay more than that multiple)

Origination fee: 1-3%

Example: $300K RBF at 6% monthly revenue share, 1.8x cap. Origination fee: $6K (2%). You pay 6% of monthly revenue until you've paid $540K ($300K × 1.8x). If revenue is $100K/month, you pay $6K/month and are done in 90 months (7.5 years). If revenue grows to $200K/month, you pay $12K and are done in 45 months.

The cap is critical. It's your insurance against slow growth. You can't be forced to pay more than 1.8x what you borrowed.

SBIR/STTR grants

Cost: Zero. No repayment, no dilution.

But: The application process is heavy. Budget 40-60 hours of technical writing. Phase I success rate is 15-20%. And you'll give the government a non-exclusive license to use your patents (standard requirement).

If you're deep tech (biotech, hard materials, semiconductors), SBIR is the obvious first call. If you're a SaaS company, it's harder to qualify.

Who qualifies for non-dilutive funding?

Eligibility varies by source. But there's a pattern.

Venture debt requirements

Raised Series A or later (or have a clear path to one)

Minimum $1M ARR (ideally $2M+)

Growth rate: 3x+ YoY common, 2x minimum acceptable

Existing investor relationships (even angels, as long as they're institutional)

Clear unit economics and customer concentration below 20% (no single customer over 20% of revenue)

Revenue-based financing requirements

Minimum $10K-$20K monthly revenue (varies by lender)

6+ months of consistent revenue history (some lenders take 3 months)

Predictable revenue model (SaaS preferred; custom services harder to model)

Monthly revenue growth rate: 5%+ preferred (20%+ is strong)

No personal guarantees needed if business credit is solid

SBIR/STTR grants

US-based company (some international exceptions)

Fewer than 500 employees

Novel technology (R&D component required)

Can be pre-revenue or early revenue

SBA loans

Operating for 2+ years (some exceptions)

Credit score 680+ (lower scores possible with compensating factors)

Personal guarantee typically required

Some revenue history required, but not Series A-level metrics

The pattern: All non-dilutive sources want proof. Proof of revenue, proof of traction, proof the business model works. Equity investors bet on potential. Lenders bet on evidence.

What founders get wrong about non-dilutive funding?

Founders assume non-dilutive funding is free capital

It isn't. You're paying in cash, not equity. That sounds cheaper until the monthly payment hits your bank account and runway shrinks.

In reality, non-dilutive funding has an explicit cost. You see it. Every month. A $100K RBF line at 6% monthly revenue share means you're writing a check for $6K every month your revenue is $100K. That cash leaves your business. You need to model whether you can afford it.

I worked with an AI company targeting logistics and manufacturing that had previously raised $8.7M, split 60% equity and 40% debt. The debt portion looked smart on paper because it preserved ownership. But the repayment schedule assumed enterprise contracts would close on time. They didn't. The founder spent two months renegotiating terms with the lender instead of closing customers. The lesson: non-dilutive only works if your cash flow supports the repayment timeline.

Founders assume they need Series A to use debt

The myth is venture debt requires institutional investors on your cap table.

Wrong. You need revenue.

In reality, revenue-based financing works for pre-seed companies with paying customers. A founder with $15K monthly recurring revenue can get a $200K RBF line without ever raising institutional capital.

Venture debt is harder pre-Series A, but it exists. Some specialist lenders (Lighter Capital, Heaton VC, others) will underwrite Series Seed companies if the unit economics are clean.

A DTC subscription founder I worked with had $100K in first-year sales, built entirely through organic social media. No institutional capital on the cap table. He was exploring a small RBF line to scale paid acquisition before pursuing a larger equity round.

The point: you don't need a Series A to access non-dilutive capital. You need revenue.

Founders assume non-dilutive funding delays equity rounds

The logic seems right: if you have debt, won't investors penalise you in Series A valuation? Sometimes. But usually not.

In reality, smart debt actually improves Series A valuations. Why? Because you extended the runway without diluting. You hit higher revenue numbers before raising.

Higher revenue = higher valuation. The debt is paid back from Series A proceeds anyway, so investors don't care. Clean your cap table at close, and you're fine.

A premium e-bike company I worked with took $2M in venture debt to fund inventory. By the time they raised Series A, they'd hit $18M revenue instead of $10M revenue. The debt got repaid at close. The Series A valuation was 2x higher than if they'd diluted themselves with Series A capital earlier.

Founders assume all non-dilutive sources are equally accessible

They're not. SBIR is incredible if you're deep tech and spend 60 hours on a grant application. Impossible if you're a B2B SaaS company. Venture debt requires Series A already closed. RBF requires 6+ months of revenue.

In reality, you have to match your company's stage to the funding sources that actually serve that stage. Understanding where you sit in the startup funding stages is the first step.

A pre-revenue startup has basically one play: grants, accelerators, and bootstrapping.

A $1M ARR SaaS company has venture debt and RBF as real options. A $5M ARR company has all of them.

I see founders chase SBIR when they should be chasing RBF, or vice versa. The timeline alone kills them. SBIR takes 9-12 months. You need capital in 60 days. RBF in 2 weeks is the answer.

Stop treating non-dilutive funding as a fallback. It's a first move. The founders who get this right don't raise equity because they have to. They raise it because the numbers say it's the right time

My direct assessment

Non-dilutive funding is underrated because it's boring. Equity rounds get press. A $30M Series B gets written up. A $500K RBF line doesn't. But from a founder's perspective, a $500K non-dilutive line that costs you 6% of revenue and requires no board seat is objectively better than a $500K from an investor who takes 5-10% equity and a seat.

The best capital is capital that doesn't exist. The second-best capital is capital that doesn't dilute. Founders who skip non-dilutive options purely because it's not "venture-scale" are leaving money on the table and accepting dilution they don't need to accept.

The smart move is to combine sources. Take a $200K SBIR if you qualify. Stack a $300K RBF line for working capital. Build to $2M ARR. Then raise Series A from a position of strength, having extended runway without selling equity you didn't need to sell.

The only time I'd push a founder toward equity first is pre-revenue. If you're still proving the model, debt doesn't make sense. But the moment you have revenue and a path to growth, you have options. Use them.

European founders especially have missed a structural advantage. The EU Commission just allocated €1.1B in government support. Access to European VC is strong. Access to government grants is even stronger. The playbook is:

European grant first

Then growth debt

Then US Series A.

Not: US Series A immediately. That costs you way more equity.

How spectup helps?

Non-dilutive capital is one piece of a larger capital strategy. Some companies should stack multiple sources. Some should do equity rounds. The question isn't 'non-dilutive or equity?'It's about what sequence of capital preserves the most equity while hitting our growth targets?'

A fundraising consultant working through this calculus with you does three things:

Maps your options (grants, debt, equity)

Models the dilution impact of each scenario

Structures the process so you aren't doing it 60 days before you run out of money

That's the difference between a clean capital raise and a desperate one.

If you're 6-12 months from a Series A and want to extend runway without dilution, or you're trying to figure out whether financial modeling consultant support for venture debt makes sense for your ARR level, that's the conversation we run. If you need help deciding between a SBIR grant, RBF line, or a small Series Seed round, we model all three.

If you're raising now and want to understand your non-dilutive options before you pitch to VCs, book a call with me. We'll map the capital sources that actually fit your company.

Concise Recap: Key Insights

Non-dilutive funding is capital without ownership loss

Venture debt, revenue-based financing, and grants preserve your equity. Debt gets repaid and the lender exits. Your cap table stays intact. The cost is explicit and upfront, not compounded across future rounds.

Matching funding sources to your stage matters more than chasing size

Pre-revenue founders: grants and bootstrapping. Early revenue: RBF. Series A already closed: venture debt. Each source has specific eligibility criteria. Chasing the wrong source wastes weeks and burns goodwill with lenders.

The best strategy stacks multiple sources strategically

SBIR grant + RBF line + venture debt can combine to $500K-$1M+ with total dilution close to zero. Founders who treat these as either/or instead of both/and leave capital on the table and accept unnecessary dilution.

Frequently Asked Questions

Can you use venture debt and equity in the same round?

Yes. In fact, it's common. A company raises Series A equity from one investor and venture debt from a debt specialist fund in the same quarter. The debt has a shorter term (3-4 years) and the equity is permanent. Investors expect you to be smart about capital structure. The debt gets repaid first and doesn't affect Series A valuation math.