Table of Content

Summary

Understand the financing landscape in 2026

According to market data, $267B flowed into US startups Q1 2026, but 80% went to AI. Non-AI founders face compressed valuations and higher bars for institutional capital.

[01]

Know why valuation is not the scoreboard

Founders obsess over valuation. Control loss compounds faster: Series A 20%, Series B 15%, Series C 12% each round. By Series C, most own less than 30%.

[02]

Choose equity when you need expertise, not just capital

Equity investors bring networks and guidance. Debt is cheaper ($500K at 10% = $550K cost vs. equity at 16.7% = $333M on $2B exit).

[03]

Model dilution compounding before round one

Conservative seed round (20% dilution) compounds to 50% ownership by Series C. Aggressive round (35%) compounds to 40%. The difference is $250M in a unicorn exit.

[04]

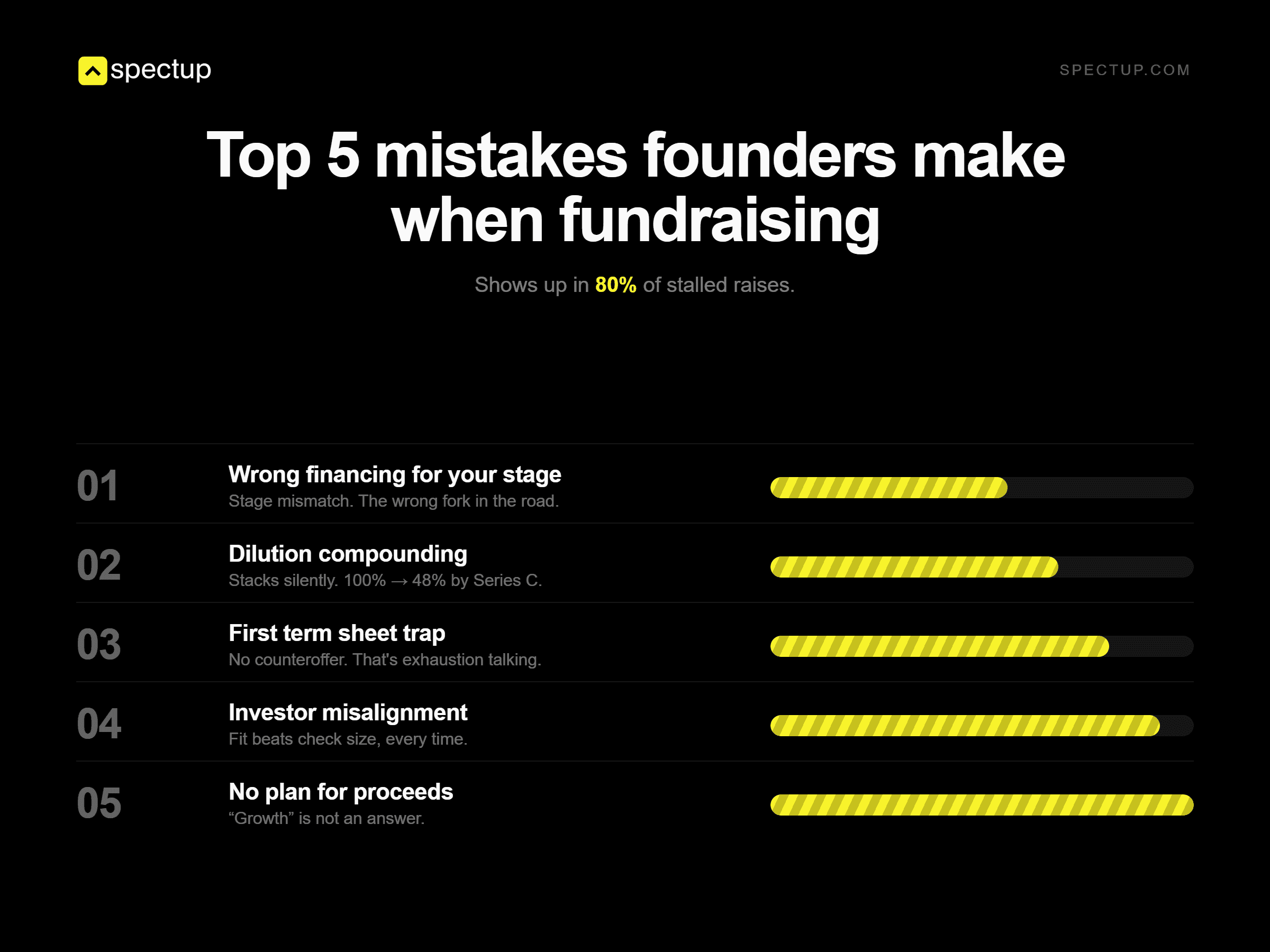

Avoid five critical mistakes most founders make

Chasing wrong financing type for stage, underestimating dilution, saying yes to first offer, ignoring investor alignment, not having a proceeds plan.

[05]

The challenge in tech startup financing is a control problem, not a valuation problem. In 2026, capital is bifurcating: AI mega-rounds are concentrating most institutional capital into AI infrastructure plays, and non-AI founders compete in a compressed market where knowing what type of capital to raise and when determines who stays in control.

Founders who stay ahead understand equity dilution, the debt versus equity trade-off, and how dilution compounds; those who skip this modelling watch their startup funding options narrow with every round they sign.

The short answer is:

Know your dilution trajectory

Model it forward five rounds before you take the first cheque

Most founders don't.

That's the noise. Here's the signal: founders who understand their startup funding options, not just the names of the rounds but the mechanics of control loss, dilution compounding, and when debt actually beats equity, close faster and on better terms.

Most don't. Most chase valuation like it's the scoreboard when it's actually just the price they paid to lose decision-making authority.

With 10 active mandates right now, I see this pattern every week. We work with founders navigating startup funding decisions across venture capital, debt, and hybrid models. The founders who move fastest are the ones who've already modelled their cap table, understood their options, and know exactly which type of capital matches their stage.

Founders spend four months optimising a deck, two months on outreach, and one month in diligence. Then they discover the cap table trajectory they're about to lock in for the next five years.

By then, negotiating power is gone. Working with spectup, we ensure the capital strategy is locked before the process starts.

The vocabulary that defines your raise

You can't negotiate a cap table if you don't know the terminology. These terms will appear throughout the rest of this post, and getting them right prevents disasters later. A founder who doesn't know the difference between pre-money and post-money will get crushed in a valuation conversation; one who doesn't track dilution across rounds discovers ownership surprises years later.

Term | Definition | Why It Matters |

|---|---|---|

Valuation | The total dollar value of your company.

Example: $5M pre-money + $2M raise = $7M post-money. | Post-money matters for ownership math. If you raise $2M at $7M post-money, the investor owns 28.6%. You own 71.4% remaining. |

Dilution | The percentage of ownership you lose in each funding round. |

Each successive round is smaller by percentage but compounds. |

Burn Rate | Monthly spending. If you raise $2M and burn $100K/month, you have 20 months of runway. | The runway determines when you raise next.

|

Cap Table | A spreadsheet showing who owns what percentage of your company and at what price. | This document locks you in. Convertible notes and option pool expansion change it retroactively. Track obsessively from day one. |

Control and Board Seats | Equity investors often demand board representation. Series A typically gets one seat. Series B might get two. | Control loss happens before you realise. By Series C, you're outvoted on the board by investors. |

The cap table is where founders lose races they didn't know they were running. Most founders ignore it until Series A, by which time SAFEs (Simple Agreements for Future Equity) and expanded option pools have diluted their stake without them noticing.

A founder who raised $500K on a SAFE with a $4M cap, then raised a $1M seed at $8M post-money, discovers the SAFE converts at a lower price than the seed investors paid.

The dilution is invisible until the conversion happens. Understanding the mechanics of SAFEs, option pools, and how future dilution compounds is your defence against ownership surprises.

Founders who track cap tables obsessively from day one catch dilution surprises before they're locked in. Make this your most important financial document from day one.

The short answer is model your cap table forward from day one. Every check that comes in, even the $25K friends round, reshapes your ownership path.

Most founders ignore the cap table until Series A. By then, it's too late to change course.

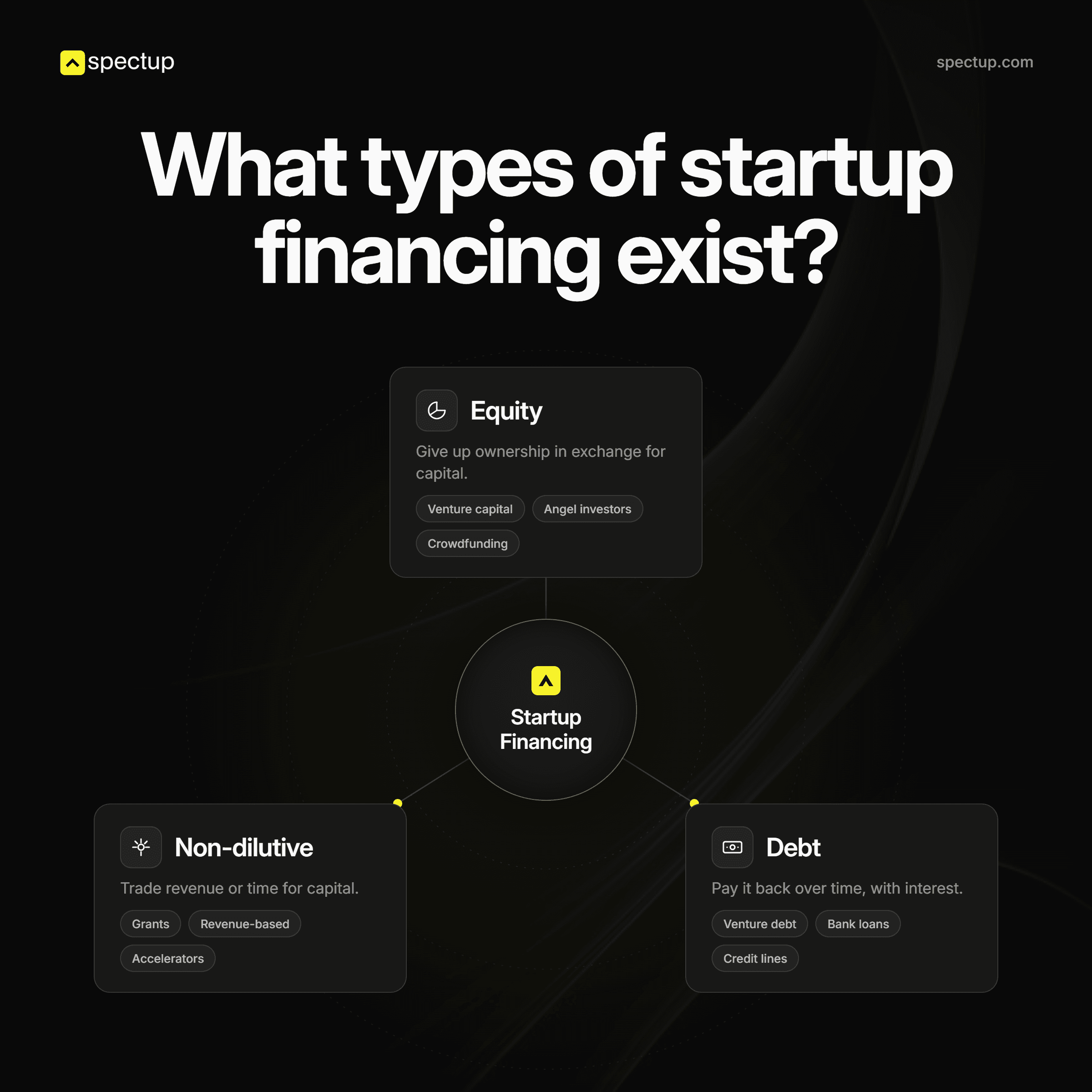

What types of startup financing exist?

Tech startup financing splits into three buckets:

Equity (give up ownership)

Debt (pay it back with interest)

Non-dilutive funding (trade revenue or time for capital)

Most founders pick whichever is easiest, not strategic.

That's the mistake. The choice you make here determines how much of your company you own in five years.

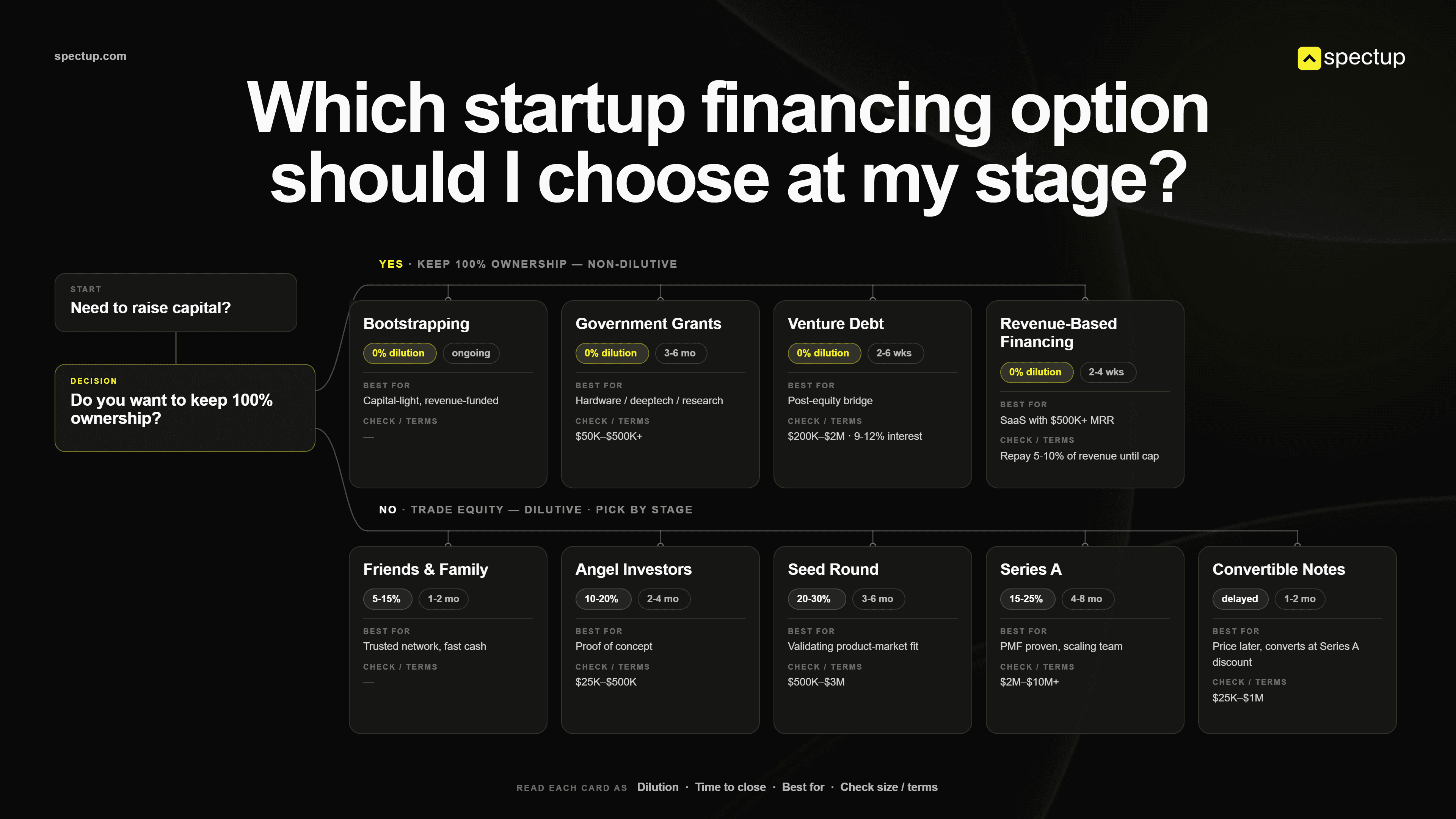

Financing Type | Dilution | Timeline | Best For | Cost/Terms |

|---|---|---|---|---|

Bootstrapping | None | Ongoing | Capital-light businesses; founders unwilling to dilute | 100% dependent on revenue |

Friends & Family | 5-15% | 1-2 months | Founders needing quick capital from trusted network | Often at below-market valuation; high emotional risk |

Angel Investors | 10-20% | 2-4 months | Seed-stage; proof of concept needed | $25K-$500K checks; high variance in terms |

Seed Round | 20-30% | 3-6 months | Early-stage; validating product-market fit idea | $500K-$3M typical; 6-12 month runway post-raise |

Series A | 15-25% | 4-8 months | Product-market fit proven; scaling team | $2M-$10M+ typical; 18-24 month runway expected |

Venture Debt | None (non-dilutive) | 2-6 weeks | Post-equity round; bridge to next milestone | $200K-$2M; 9-12% interest; 3-4 year repayment |

Revenue-Based Financing | None | 2-4 weeks | SaaS/subscription with $500K+ MRR | $100K-$1M+; repay 5-10% of monthly revenue until cap |

Government Grants | None | 3-6 months | Hardware, deeptech, research; regional programs | $50K-$500K+ depending on program; highly competitive |

Convertible Notes | Yes, but delayed | 1-2 months | Early rounds; pricing deferred to later equity round | $25K-$1M+; interest accrues; converts at Series A discount |

This table is not exhaustive. Hybrid models exist: some founders raise 60% equity financing and 40% debt in the same round, combining equity with non-dilutive capital to balance ownership and growth runway. Others combine government grants with venture debt.

Smart founders view tech startup financing not as a linear path (seed to Series A to Series B) but as a menu of options to assemble strategically.

The point is that your financing mix is a choice, not a default. Each choice trades something for capital: ownership, interest expense, reporting requirements, or time.

Equity: Give up ownership now, share future upside with investors, no repayment obligation if the business fails

Debt: Retain full ownership; repay capital with interest regardless of outcomes; faster to close than equity

Non-dilutive: Trade revenue, time, or reported impact for capital; preserve ownership but require operational constraints

How does equity financing work?

Equity financing means you trade ownership for capital. The investor's stake lasts forever: IPO, acquisition, bankruptcy – it doesn't matter. They own their slice.

If you go public, they own their slice

If you're acquired, same

If you go bankrupt, they get nothing

Here's what founders consistently miss: the valuation is almost irrelevant compared to the control loss. Real cap table data from post-exit companies shows the same pattern repeatedly. A 20% seed dilution becomes 45% ownership loss by Series B when you factor in subsequent rounds and option pools.

Why does a 20% seed dilution end up costing founders 40% or more by Series B? Because it compounds with every subsequent round and option pool expansion. A founder we worked with took a $5M seed round at $17M pre-money (28.6% dilution), and the investor took a board seat.

Eighteen months later, the founder wanted to pivot product direction based on customer discovery. The board investor's response: four months of debate while product development froze.

By the time the pivot happened, two competitors had captured the market the founder had discovered first. Customer churn had accelerated in the gap.

The company was acquired four years later at a lower exit multiple than it would have achieved with product-market fit intact. The founder's $1.5M stake (on a $35M acquisition) felt hollow given what could have been.

The founder was so focused on the $17M valuation that he didn't model what happens when you can't make strategic decisions alone anymore. The control he lost was worth more than the valuation he gained.

This is why understanding your venture capital terms and equity impact upfront is non-negotiable. Working with a fundraising consultant to model board dynamics and decision authority upfront prevents this common scenario.

Equity rounds have a rhythm: angels first (high conviction), seed investors next (betting on founder quality), institutional VCs later (metrics-driven). Understanding this progression is core to your tech startup financing strategy. At each stage, you're trading more decision-making authority.

Angel checks are checks: $25K-$500K, few strings attached. Seed rounds add governance: information rights, maybe an observer seat at the table.

Series A includes board representation (one investor seat), information rights (monthly financials, board materials), and veto provisions (major decisions require investor sign-off). Series B adds another board investor, and veto provisions expand.

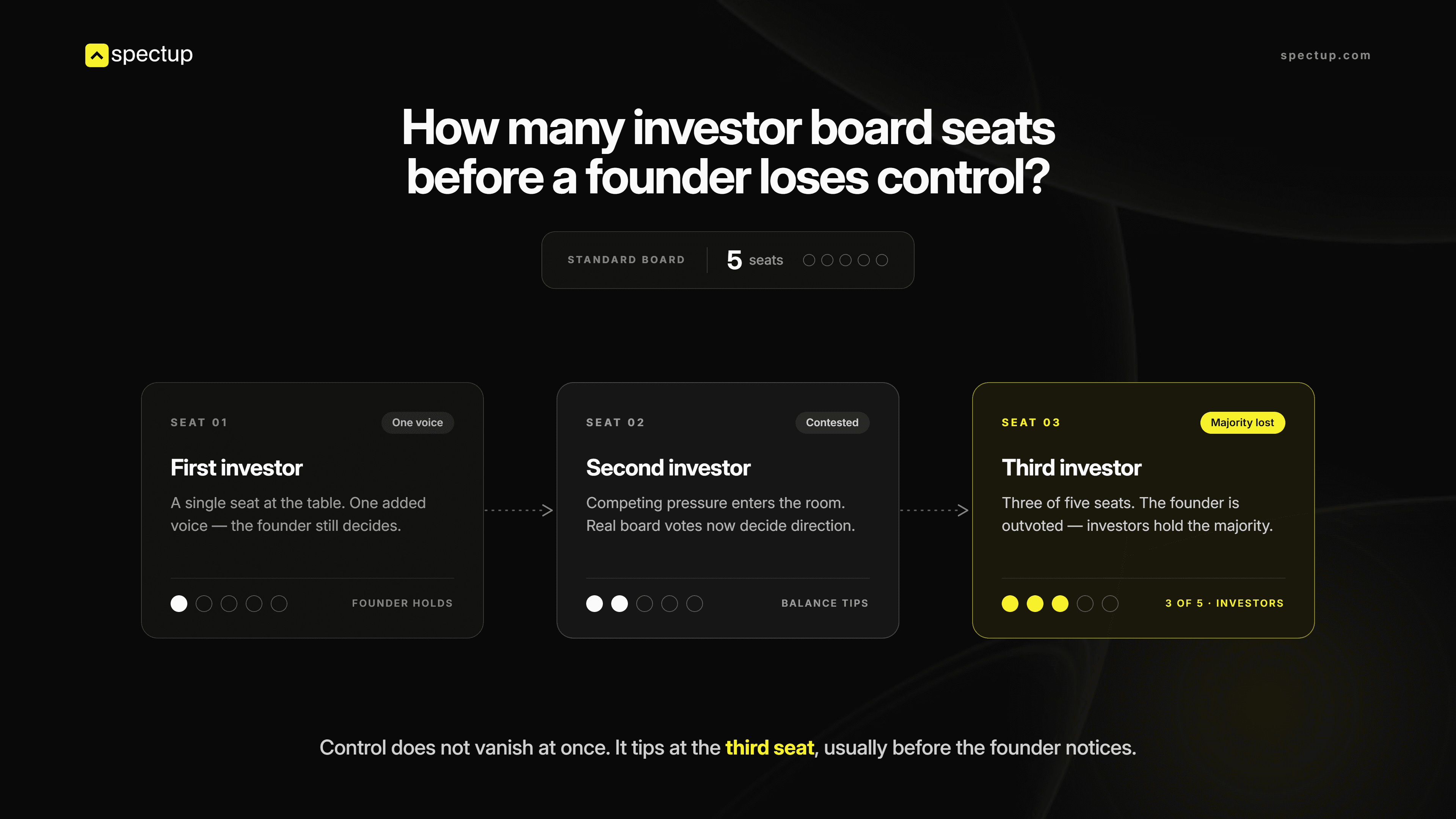

Control shifts with every board seat.

First investor is one voice

Second adds competing pressure and board votes

By the third, you're outvoted on a standard 5-person board structure

Most founders don't notice until they try to make a decision and can't.

Extending runway gets overruled, pivoting gets blocked, and that 4x acquisition gets outvoted because the fund needs 10x. The founder title is yours. The decision authority isn't.

The hidden cost of equity rounds is option pools. Series A investors usually demand 10-20% carved out for future hiring. This dilutes everyone, including you and the seed investors.

So a 20% Series A dilution actually costs 25-30% when you factor in the pool. Real cap tables show founders think they're accepting 20%; they're really accepting 28% when the pool is carved out. This shows up in the term sheet, and most founders don't model it until it's locked in.

Debt vs equity: the decision framework

Here's the tech startup financing framework that almost no founder uses but should:

Debt if you have revenue

Equity if you're pre-revenue and need expertise and capital simultaneously.

Debt is cheaper. A venture debt firm lends $500K at 10% interest over 3 years: Total cash outlay: $550K. Equity is expensive: that same $500K at a $3M post-money valuation costs you 16.7% of your company forever.

If you go public at a $2B valuation, that 16.7% stake is worth $333M. The $500K loan cost you $333M on an exit. This math is why venture debt exists: it lets founders avoid dilution.

So why does anyone raise equity? Two reasons.

Equity investors don't require you to repay anything if the business fails.

If your company burns cash for 18-24 months and misses product-market fit, the investor lost their check. You owe nothing else; that's zero liability on a failed experiment.

Debt requires monthly payments whether you're growing or collapsing. If you're pre-revenue and uncertain, debt payments become an additional burn.

Equity investors bring expertise and networks you actually need. $500K from an investor includes introductions to customers, guidance on product direction, and credibility with future investors.

A $500K loan from a debt firm includes a term sheet and a lender relationship. Different products.

Pre-revenue founders need equity because they need runway (capital with no repayment requirement) and expertise (investor guidance on founder mistakes). A venture debt firm won't lend to someone with zero revenue. Debt underwriting is revenue-based.

An equity investor will fund pre-revenue teams because their game is pattern recognition on founding teams and market timing. They're betting on founder execution, not current revenue. But this expertise comes at a cost: equity dilution and board oversight.

The short answer is yes, venture capital structured as debt is dramatically cheaper than equity.

A $500K loan at 10% interest costs $550K total; the same capital at 20% dilution is worth $500M+ on a successful exit. This is why understanding the full menu of tech startup financing options matters before you sign anything.

According to SVB and other venture debt firms offer non-dilutive loans that post-revenue founders should seriously consider before raising equity. We've seen $5M ARR SaaS founders raise $2M equity rounds when venture debt would have been cheaper and faster.

A $2M equity round takes 4-6 months of process, board diligence, legal work, and ongoing governance (monthly board meetings, quarterly financials, and information rights). A $2M venture debt round takes 2-3 weeks: application, underwriting, term sheet, close.

The $2M equity round costs you 15-20% dilution.

The $2M debt round costs you 10% of annual revenue (roughly $50K/month on $5M ARR, payable over 3-4 years = $600K total interest). The debt is cheaper.

But equity gives you negotiating power for higher valuations in Series A. A founder who raises equity at $15M post-money signals market confidence.

A founder who raises only debt might signal they couldn't raise equity. The signal matters to future investors.

The growth paradox: debt is cheaper, equity is faster and brings expertise.

When you're pre-product-market fit, speed and expertise matter more than cost

When you're past PMF with clear growth metrics, cost matters more than speed.

A $10M ARR founder with 50% YoY growth and positive unit economics should never raise equity, they should raise venture debt and preserve ownership. A $500K ARR founder who pivoted three times should raise equity; they need an expert partner and room to pivot again without payment pressure.

The difference: a revenue-backed founder can access investor outreach services to negotiate from strength, whereas a pre-revenue founder needs an investor's expertise and conviction.

Non-dilutive funding: the overlooked path

Can you raise capital without giving up equity in your tech startup financing strategy? Yes: grants, revenue-based financing, customer deposits, and strategic partnerships all preserve 100% ownership. Yet most founders skip them entirely.

The reasoning is fair: non-dilutive funding takes longer (grants 6 months, partnerships 3-6 months).

Equity funding takes 3-4 months in the best case. When you're burning cash, longer timelines feel dangerous. But they often aren't.

A SaaS founder we advised was at $250K ARR with 12 months of runway. They had two options: raise a $1M seed round at $4M post-money (25% dilution) or pursue revenue-based financing for $500K at 8% of monthly revenue.

The non-dilutive funding approach was cheaper in cash cost (they'd repay $50K/month = $600K total cost) and faster in execution (closing vs. full diligence). They chose equity because it was familiar.

Non-dilutive funding shines for hardware companies and deep tech.

Government grants (SBIR/STTR in the US) fund hardware R&D at $150K-$500k

EU Horizon programmes go to €3M

These aren't consolation prizes; they're capital from sources that don't own equity and don't attend board meetings.

Revenue-based financing is non-dilutive lending: you repay a percentage of monthly revenue until you've paid principal plus interest. A $500K RBF deal at 8% of revenue, with a $600K total cap, takes 12 months at $50K/month revenue or 6 months at $100K/month.

The faster you grow, the faster you're done paying. At $500K ARR and above, RBF often beats equity for founders who are profitable or nearly so. The risk is asymmetric: if you grow 3x, you're done in 6 months and still own 100% of the company.

If you grow slowly, you're making small payments but still own the company. You never lose control.

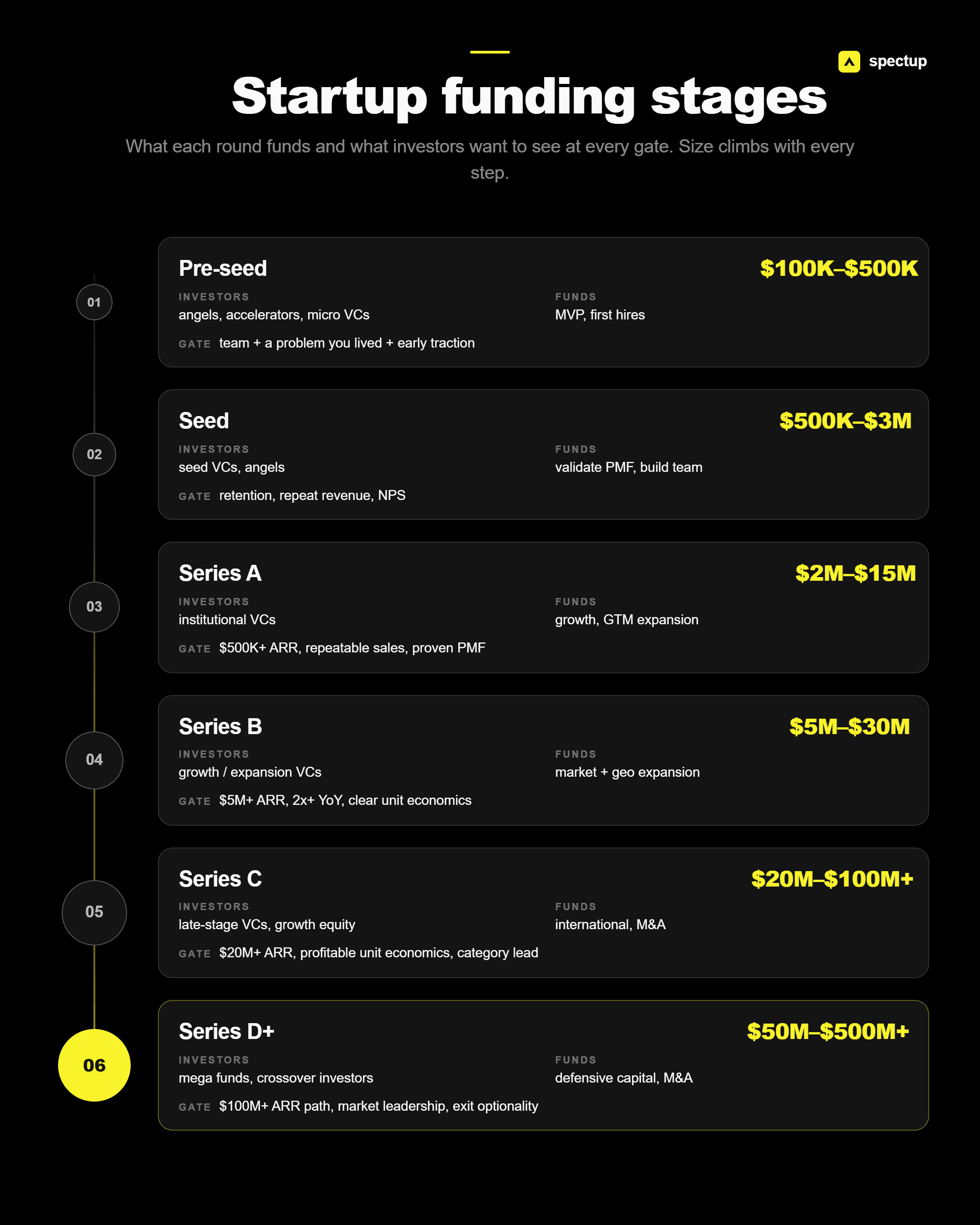

The funding stages: from pre-seed to late-stage rounds

Funding rounds have distinct sizes, investor types, and expectations at each stage, and your tech startup financing strategy must align with these. NVCA Venture Monitor benchmarks show the current funding ranges and investor patterns.

The mistake founders make is raising at the wrong stage for their metrics. Pitch Series A with $100K ARR and you'll get passed in three weeks. Pitch it with $1M ARR and the conversation changes entirely.

Stage | Typical Size | Investor Type | What It Funds | What Investors Want to See |

|---|---|---|---|---|

Pre-Seed | $100K-$500K | Angels, accelerators, micro VCs | MVP, first hires, proof of concept | Founding team + problem they experienced + quick initial traction |

Seed | $500K-$3M | Seed-focused VCs, angels | Product-market fit validation, team building | Product-market fit signals (retention, repeat revenue, NPS) |

Series A | $2M-$15M | Institutional VCs | Growth acceleration, GTM expansion | Proven product-market fit, repeatable sales, $500K+ ARR |

Series B | $5M-$30M | Growth equity, expansion VCs | Market expansion, geographic expansion | $5M+ ARR, 2x+ YoY growth, unit economics clarity |

Series C | $20M-$100M+ | Late-stage VCs, growth equity | International expansion, acquisitions | $20M+ ARR, profitable unit economics, category leadership |

Series D+ | $50M-$500M+ | Mega funds, crossover investors | Defensive capital, strategic acquisitions | $100M+ ARR path, market leadership, exit optionality |

The 2026 market has collapsed timelines. A founder with 3x YoY growth, 130%+ NRR, and CAC payback under 12 months can jump seed to Series B in 18 months. A founder pivoting slowly can take 3-4 years to Series A.

There's no fixed schedule. What matters is matching your ask to your actual progress, not to calendar rounds.

Early-stage investors (angels and seed funds) fund the founder + idea. They know the company will pivot; they're betting on pattern recognition: founder quality, problem insight, and willingness to iterate.

A pre-seed funding stage pitch with traction (10+ paying customers, $5K MRR) is stronger than a seed pitch with zero revenue.

Series A investors fund product-market fit proof.

They want to see retention (customers stay), expansion (customers grow), and repeatability (you can acquire more like them). This is where having a repeatable sales process matters – not a one-off land deal, but evidence you can rinse and repeat customer acquisition, and preparing a strong pitch deck becomes essential to close the round.

Series B investors fund growth at scale

They're not debating whether your product is good; they're asking:

Can you grow 3x while maintaining unit economics?

How much will you burn to achieve that growth?

What's the payback period?

Series B is where founder control visibly contracts because the question has moved from "is this real?" to "can you professionally scale it?"

5 critical mistakes founders make when capital raising

Most fundraising failures aren't product failures; they're timing and mindset failures. In my experience across 10 active mandates, these five mistakes show up in 80% of stalled tech startup financing processes. Our pitch deck team sees them weekly.

Mistake 1: Chasing the wrong type of financing for your stage.

Pre-revenue founders raising venture debt (lenders won't touch them); revenue-producing founders raising seed capital at inflated valuations when seed investors want validation risk, not optimisation.

Bootstrapped founders at $500K ARR pursuing Series A when venture debt or revenue-based financing would close in weeks, this mismatch kills processes before they start.

The startup funding path isn't a highway; it's a branching tree based on your stage and metrics. You choose which fork by understanding where you are and where you're going. A founder at $100K MRR should not be pursuing seed rounds.

They should be pursuing venture debt (2-3 weeks to close, $200K-$1M at 10% interest) or angel rounds. Seed investors want to fund product-market fit validation, not growth optimization. Mismatched stage + financing type = months of process with zero traction.

Get the stage right, and the startup funding process accelerates.

Signs you're raising too early:

You have zero customers or paying traction but are pursuing Series A rounds

You have revenue but no path to profitability, yet you're avoiding venture debt

You haven't shipped a product yet and are already in investor meetings

You're burning $50K monthly on team before product validation

Mistake 2: Underestimating dilution compounding.

The dilution in equity rounds compounds relentlessly:

Seed at 25%, Series A at 15%, Series B at 12%, Series C at 10%. Each round feels small individually.

Each round feels small individually, but compounded, founder ownership drops from 100% to 48% by Series C. This is why tech startup financing strategy demands forward modelling with someone who understands the impact; cap tables from real Series C founders show this exact pattern consistently. Working with a fundraising consultant to model dilution across five rounds prevents the surprise of discovering 40% ownership loss.

One founder we worked with took a 22% seed dilution and thought it was conservative. By Series C, he owned 31% of a company generating $40M ARR. The 31% was worth $120M in the eventual exit, so he can't complain.

But had he negotiated seed rounds more aggressively, he'd own 45% and be worth $180M. The difference is $60M. By the time you realise the compounding effect, your negotiating power in Series C is gone.

Model your cap table forward five rounds before you take the first check.

Mistake 3: Saying yes to the first offer.

The first term sheet feels like validation; it's actually just one person's view of your company. The cost of turning it down is 3-4 months; the cost of accepting bad terms compounds for the life of the company.

Aggressive anti-dilution provisions, follow-on expectations, and restrictive board seats compound for the life of the company. A bad Series A term sheet becomes the template for Series B and C.

Founders accept the first term sheet because they're exhausted from fundraising.

If an investor says no to a counteroffer on terms, they weren't confident in your upside anyway.

Confident investors fight for the companies they believe in.

Mistake 4: Ignoring investor alignment.

Capital from misaligned investors is often worse than no capital. A $5M check from a 50-company spray-and-pray fund treats your company differently than one from a focused 15-company portfolio where industry expertise and geographic focus both match.

A Southeast Asia-focused VC expecting 5x on a regional play wants you to stay regional and exit profitably; a global fund expecting 10x+ wants US expansion and an eventual IPO. Neither is wrong. Misalignment is wrong.

A founder we advised took $2M from a European fund expecting an 8-year hold period and a debt/equity exit. Two years later, a US acquirer showed interest in a 4-year hold. The European fund blocked the sale because it didn't match their LPs' expectations.

The founder couldn't exit. Talk about exit expectations explicitly before you take the check. Get it in writing.

Mistake 5: Not having a plan for proceeds. Investors want to know:

What does this capital do for you, not "growth" or "scaling" but specifically and operationally at each function? Founders who can't answer this in 60 seconds haven't done the work.

Avoiding this fundraising mistake means forcing yourself into specificity before the investor meeting. An investor asking, "What will you do with this capital?" and hearing a vague answer will lose confidence immediately.

The right answer: "$1.2M for team hiring (VP Sales, three SDRs, one CS manager); $1M for paid customer acquisition (LinkedIn ads, sponsorships, events); $500K for product development (three engineers for Series B feature set); $300K for operations (finance hire, legal retainer); $300K operating buffer."

This is concrete and believable; it shows you've thought through the fundraising round in parallel with operational needs. Vague founders get vague interest. Specific founders get committed investors.

What to expect in 2026: market trends and founder timing?

Q1 2026: $297B flowed globally in venture capital, though the US portion reached $267B, but the headline hides a bifurcation that changes everything for non-AI founders. AI captured 80% of global capital ($242B of $297B). OpenAI's $122B and Anthropic's $30B alone exceed combined Series A and Series B deployments for traditional startup funding.

For non-AI founders, the market feels abundant. It isn't; it's concentrated. The capital available to you depends entirely on whether you're building AI infrastructure or solving problems for humans.

What's changed: timelines compressed. In 2026, a weak Series A pitch gets passed in week 3 (down from 4 months of meetings and slow fades in 2024) – one investor meeting and done. That efficiency works in your favour: you know fast whether an investor is serious.

Geographic advantage is gone. A Munich founder with $2M ARR and 100% NRR can now raise funds from US VCs without moving, but they compete against Austin, SF, and Berlin founders for the same pool. What matters: warm intros from portfolio companies and a verifiable track record.

Institutional capital is consolidating. LPs are backing established managers with proven exits (worst year for first-time funds since 2008), and fewer micro VCs are spinning out. The money flows to managers who've already returned capital.

For founders, this means warm intros from existing portfolio companies matter exponentially more than they did in 2021. Cold outreach gets passed. A founder with a Sequoia portfolio intro gets a meeting in a week.

For non-AI startups navigating tech startup financing, raising is harder, but the investors who write checks are the ones who actually want you. Spray-and-pray angels, micro-VCs clicking 'yes' to every pitch, and accelerators funding 100-company cohorts are all gone. This is a feature.

You get partners or passengers. Partners compete for your seat and defend you. Passengers show up when there's bad news.

In 2026, there are fewer passengers. That's good.

My direct assessment

Here's what most people get wrong about tech startup financing: they treat it like something that happens to them instead of something they architect. Every bad financing outcome traces back to earlier decisions made under pressure or bad information. The winners aren't the ones who negotiate hardest in the term sheet; they're the ones who modelled their cap table, understood their alternatives, and moved from reactive to proactive.

A founder with six months of runway and an investor who understands their market is in a stronger position than a founder with eighteen months of runway and a misaligned investor writing a big check. The runway matters less than the fit and the structure.

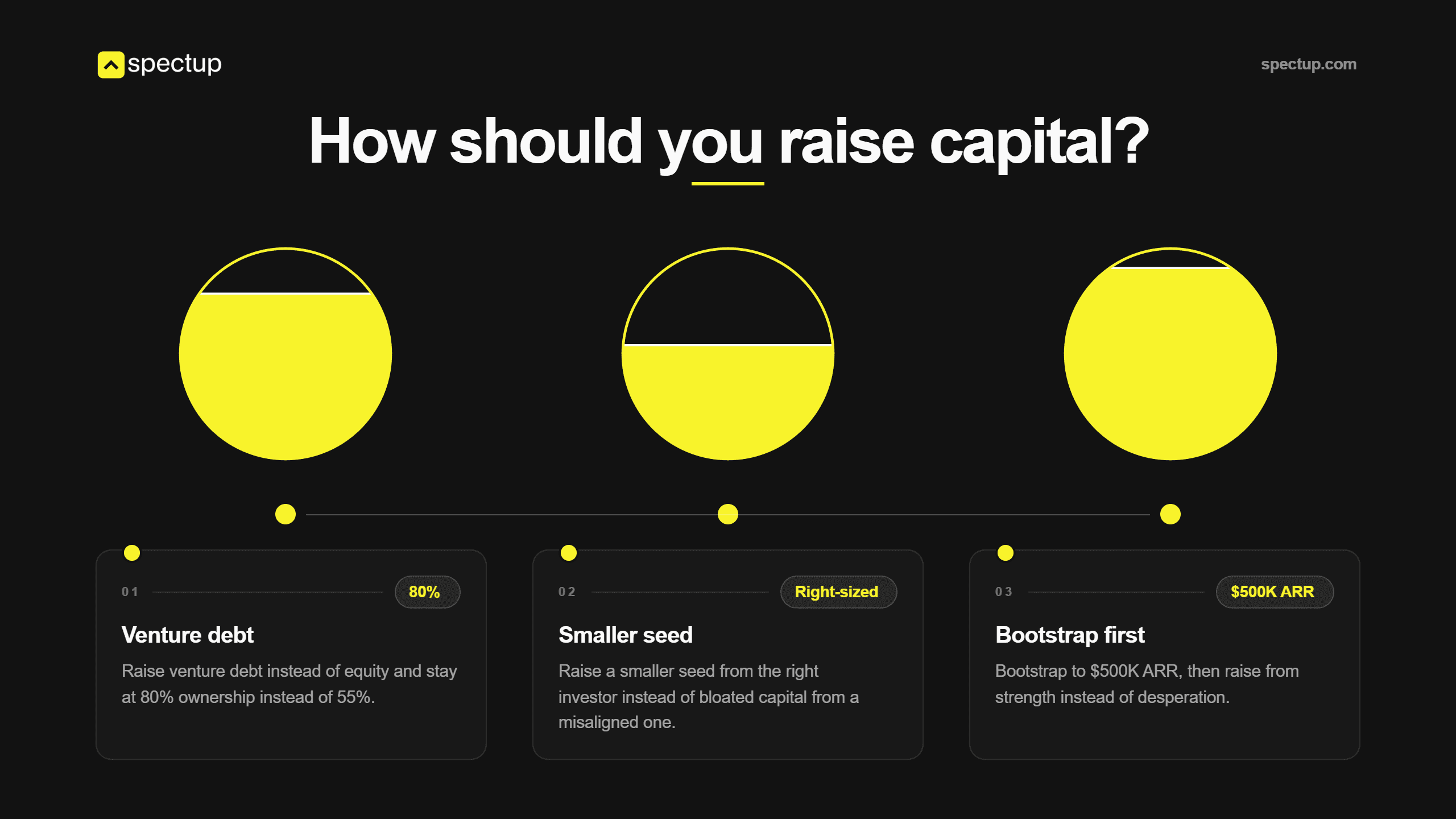

2026: the bifurcated market means non-AI founders navigating tech start-up financing have to think harder. You can't out-raise the mega-funds. You can out-think them.

Raise venture debt instead of equity and stay at 80% ownership instead of 55%

Raise a smaller seed from the right investor instead of bloated capital from a misaligned one.

Bootstrap to $500K ARR, then raise from strength instead of desperation.

These aren't sexy and don't make for good founder war stories. But they preserve control and optionality across five rounds, and the compounding effect is massive.

2026 playbook: get to revenue fast, stay lean, and be selective about who you take capital from. Speed and team quality matter more than capital abundance.

How spectup helps

Most founders treat financing like a crisis: 6 months from depletion, they panic and take the first offer. The Y Combinator seed fundraising guide puts it well: the best fundraising happens before you need it. By the time you need it, your negotiating position is gone.

Real fundraising starts earlier, when you have runway and optionality. Our work focuses on the decisions that come before the process: which capital type, where your cap table lands by Series C, when to say no, and which investors actually align with where you're going.

We've modelled cap tables for founders at every stage and restructured bad Series. A term sheet, introducing them to venture debt when equity would've been a mistake.

What we catch consistently: founders underestimating their dilution trajectory by 10-15 percentage points before signing. They think they're giving up 20% in Series A; the actual path to Series C is 35-40% when option pools and future rounds compound. Founders who model with us before desperation hits close Series A 15% faster and negotiate from a position they actually understand.

If you're mid-raise and squeezed, or you're a year out and want to think through your financing path strategically, that's what a fundraising consultant is for.

Cap table modeling: We map ownership across five rounds so you see where you land at Series C, not where you assume you land

Financing type assessment: Whether equity, venture debt, or non-dilutive fits your stage and metrics, with the math showing why

Term sheet evaluation: We've restructured terms that recovered 8-12% founder ownership founders were about to sign away

Raise preparation: You go into conversations understanding your alternatives, which changes how you negotiate

Personal conclusion

Most founders wait for the right moment to start thinking about tech startup financing. They finish the product, get a few customers, and then start learning about dilution, board seats, and cap table mechanics; by then, the first cheque is already in and the terms are locked.

In my experience across 10 active mandates, the founders who end up with the best outcomes aren't the ones who raised the most; they're the ones who understood the options before they needed them. A founder who models their cap table at 18 months of runway negotiates differently than one who models it with six months left.

Same deal on the table, different negotiating position, different terms, different ownership trajectory for the next decade. The gap between those two founders is preparation, not talent.

The goal isn't to become a financing expert. It's to understand enough to ask the right questions before you sign. That gap is smaller than most founders think, and the return on closing it is measured in percentage points of ownership you actually keep.

Concise Recap: Key Insights

The 2026 market favors founders with revenue

Q1 2026 funding records are concentrated in AI. Non-AI startups face compressed valuations and higher institutional bars. Pre-revenue founders compete harder; revenue founders gain bargaining power.

Equity dilution compounds faster than expected

Seed: 20-30%, Series A: 15-25%, Series B: 12-20%. By Series C, founders often own less than 30%. Model your cap table forward five rounds before taking the first check.

Non-dilutive funding is not a consolation prize

Revenue-based financing, grants, and venture debt are legitimate tools for $500K+ ARR founders. They're often cheaper and faster than equity, yet most founders ignore them.

Frequently Asked Questions

What separates a seed round from a growth-stage raise?

Seed rounds fund product-market fit validation with 6-12 months of runway and $500K-$3M in capital, investors bet on founder quality and early traction signals like retention and repeat revenue. Series A rounds fund growth and scaling with $2M-$15M in capital over 18-24 months of runway. At Series A, investors want proof: $500K+ ARR, repeatable customer acquisition, and strong unit economics.