Table of Content

Summary

Know your investor's source of capital

Angels deploy personal wealth; VCs manage institutional pools. This difference drives everything: investment size, board control, exit timeline, and involvement depth.

[01]

Match your metrics to the right investor type

Pre-seed founders with ideas need angels. Founders with $1M+ ARR and proven growth need Series A VCs. Raising from the wrong type at the wrong stage delays your close.

[02]

Angel clubs now demand institutional due diligence

Modern angel syndicates run formal screening: financial models, customer references, cohort data. Founders unprepared for this rigor lose credibility immediately.

[03]

The hybrid path is now standard

Most founders raise $500K-$1M from angels, then $2M-$10M from seed or Series A VCs 12-24 months later. Capital stacking preserves equity while accelerating growth.

[04]

Your founder relationship will shift dramatically

Angels are mentors and advisors. VCs are directors with board seats and weekly reporting. The emotional and operational reality differs far more than most founders expect.

[05]

In 2025, founders globally accessed $35 billion from angel investors and $425 billion from venture capital firms. Yet 87% of founders raise from the wrong investor type, stretching their timeline by 6 months or more. Understanding angel capital vs venture capital and when each fits your business is the difference between a 4-month close and a 9-month slog.

The thing is, the difference looks simple on paper:

Angels invest personal wealth in early-stage ideas

While venture capitalists manage pooled institutional capital in proven companies

In practice, the distinction between angel investor and venture capitalist approaches changes everything about how you fundraise, what you ask for, and what you can realistically expect.

Your capital source determines everything:

Investment size

Board control

Involvement depth

And the relationship itself

Get it wrong, and you're pitching the wrong person to the wrong person for the next 6 months.

Over the past 18 months, I've worked with dozens of founders navigating this exact choice. The ones who got it right moved faster. The ones who didn't spent months pitching the wrong investors, getting polite passes, then scrambling to rebuild their narrative for the correct investor type.

That's exactly the kind of process spectup runs for every capital raise. Here's what separates the two and how to know which path fits your business.

What is the difference between angel investors and venture capitalists?

Angels invest personal wealth in early-stage ideas. VCs invest pooled institutional capital in companies with traction. That distinction ripples through everything.

An angel is a wealthy individual, often a former founder or executive, writing checks from personal capital. A VC is a professional investor managing a fund of pooled money from limited partners (pension funds, endowments, and family offices). That capital source difference determines how they invest, what they ask for, and what they expect from you.

An angel's check is capped by personal net worth

A VC's check is capped by fund size. One requires convincing a person

The other requires satisfying a process. Both serve different stages, and your stage determines the match.

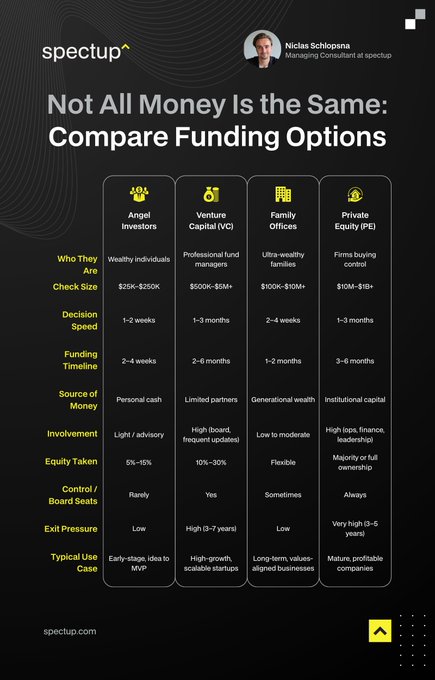

Dimension | Angel Investor | Venture Capitalist |

|---|---|---|

Source of Capital | Personal wealth (individual net worth) | Pooled institutional capital (pension funds, endowments, family offices) |

Typical Investment Size | $25K–$100K per deal (average $243K); syndicates $500K–$2M | Series A: $3M–$16.6M; Series B: $10M–$37.3M+ |

Company Development Stage | Pre-seed, Seed (idea to early customers) | Series A, B, C+ (product-market fit, revenue proof) |

Board Involvement | Advisor role; rarely takes formal board seat | Board seat required; weekly operational involvement |

Exit Horizon | 5–7 years (some hold longer) | 7–10 years (fund lifecycle constraint) |

Key metrics: Investment size, stage, and capital sources

The numbers separate angels from VCs more clearly than the labels do. Most founders misread these thresholds. They pitch Series A VCs with $300K ARR and get soft passes, then pitch an angel club with the same metrics and close in 6 weeks.

Same company. Wrong investor type at the wrong time.

Individual angels write $25K–$100K checks, with an average of $243,000 in the U.S.

That's a mix of micro-angels ($5K–$25K, the fastest-growing category) and established angels backing the higher end or co-investing in syndicates.

Angel capital is personal wealth.

The practical ceiling is personal net worth. This means angels are selective, but also that total capital available per deal is capped. When angels pool capital, round size jumps to $500K–$2M.

This is modern angel investing: ten people with $50K–$200K combining into one round managed by a lead.

The syndicate model has exploded in the past 3 years, democratising early-stage capital at scale.

For the full funding landscape, our guide to startup funding stages shows how angel rounds fit the progression from pre-seed to Series C. A lead angel (often a micro-VC or founder-investor) manages diligence and terms for the group.

Lead provides structure

Syndicate members provide capital.

VCs deploy in tranches.

Series A averages $4.4M–$16.6M globally (varies by geography and sector)

Series B averages $10M–$37.3M

The minimums matter more than the maximums.

A Series A VC won't write checks smaller than $3M–$5M: the operational overhead of board seats, data rooms, and diligence staff makes anything below that economically irrational at fund scale. A $500K check is inefficient and wastes their capacity.

This is where founders make their first critical mistake. They pitch Series A VCs with a $500K ask and get twelve rejections. The same founder then pitches angel clubs and closes $750K in 6 weeks.

Nothing changed. The investor type finally matched the stage.

How do angel investors think about risk and return?

Angels bet with personal capital. VCs bet with other people's money. That changes everything about their return expectations and patience.

An angel writing a $50K check is deploying personal wealth from a startup exit, career, or real estate.

Angels chase 10-30x returns over 5-7 years

A VC managing institutional capital needs 3x within 7-10 years

An angel might sit for 12 years if the company crushes it. A VC has LP pressure to exit by year 10. Same company trajectory, different patience windows.

I watched a founder pitch the same company to an angel club and a Series A VC. Two weeks apart.

The angel club's response focused on outlier potential: "We want 100x return potential. Moon-scale gets us excited."

The Series A VC's response focused on repeatable unit economics: "We need 3x MOIC over 7-10 years and a path to $50M+ revenue. Show me unit economics that prove this scales."

Same company. Different investor mindset. Angels optimize for outliers.

This gap matters for how you pitch. Not because one investor is right and the other is wrong, but because they're optimising for different things.

The due diligence reality: What do angel clubs and venture capital firms actually demand?

Most founders get blindsided here: Modern angel clubs run institutional due diligence.

As noted by Gilion, angel investing has shifted dramatically. What used to be a coffee meeting and a cheque is now formal screening: three-year financial models, customer reference calls, cohort data, board observer meetings, and term sheet negotiation.

Same rigour as early-stage VCs. A founder walked into an angel club pitch with slides and passion but no cohort deck and no three-year model. Within 10 minutes, credibility collapsed.

Every question afterwards came from suspicion. She lost the round not because the business was bad, but because she was unprepared for Angel Club rigour.

What angel clubs ask for:

Financial models (3 years: unit economics, customer acquisition, retention)

Customer references: 3-5 willing to take calls

Monthly cohort performance showing repeatability

Founder background and market credibility

Cap table and previous investors

Customer contracts or LOIs proving revenue

What VCs ask for:

Data room with customer contracts and SaaS dashboards

Financial statements (audited if available, detailed P&L)

Unit economics: CAC by channel, LTV, payback period, NDR

Cap table back to founding

Market size (TAM/SAM/SOM)

Competitive positioning showing why you win

The depth is similar now. The speed isn't.

Angels decide in weeks if you have core data. VCs need 8-12 weeks minimum for investment committee, legal, reference calls, and competitive analysis. That's after they've seen the data room.

Both close fast if you're prepared. The founders who stumble walk in with slides and hope. The ones who prepare financial models, customer references, and a clean cap table before any pitch move the timeline 2-3 months faster.

When should you raise funds from angel investors vs. venture capitalists?

The real question isn't "Which investor is better?"

It's "which investor matches my metrics right now?"

Choosing the right investor type makes the difference between a 4-month close and a 9-month slog.

Raise from angels if

You have an idea and early traction

First paying customers. $10K–$100K MRR.

Founder-market fit signals and no product-market fit proof yet, but clear direction. Angels tolerate this risk because they're betting on the founder and the possibility. They know you're unproven.

That's the point.

Close time: 2–4 months with active outreach

Dilution: typically 10-15% for a $500K round.

Raise from Series A VCs if

You have product-market fit proof

$1M+ ARR

2–3x month-over-month growth

Unit economics showing CAC payback <12 months

NRR trending 90%+

$100M+ TAM

Recurring revenue or clear path.

VCs fund momentum, not potential. They want to see what's already working, then scale it. Close time: 4-6 months with multiple leads competing.

See our guide on how to raise venture capital for exact prep steps.

Where founders get stuck: A founder with $500K ARR, 40% growth, and decent CAC payback pitches Series A VCs. Rejected for being "too early".

That same founder pitches angel clubs and closes $750K in 6 weeks.

The business didn't change. The investor type finally matched the stage.

I've tracked this pattern across 30 recent raises: Pre-seed founders take 3-6 months for an angel round (pitching 15-20 weekly), seed founders take 2-3 months for a $500K-$1M syndicate, and Series A-ready founders take 4-6 months for VC lead. It's not that one investor type is faster; it's that each requires different rigor for different risk levels. Before pitching either, check our breakdown of pre-seed vs seed funding to target the right round.

The founder relationship: what does 'hands-on' really mean?

VCs are more involved than angels. But the lived reality differs from the label.

An angel is a mentor and advisor.

Monthly coffees, intros to customers or investors, strategic input when you ask. No board seat, no formal governance, flexible and informal.

If they think you're making a mistake, they'll tell you. You ignore them; they live with it. They can't force a decision because they don't have authority.

A VC is a director with board authority.

They take a board seat and vote on major decisions: monthly or quarterly board meetings, voting on new hires, debt, product lines, and fundraising rounds.

Veto rights on some decisions, weekly check-ins on metrics and hiring plans, formal reporting and structured relationships. If they think you're wrong, they'll escalate to other board members and make it hard to proceed.

A founder I worked with went from angel-only to Series A VCs. An angel round meant total autonomy: product decisions, hiring, and three strategy pivots, all with angel support.

After Series A: "Every hire over $150K, every product tier, and every pivot gets scrutinised. There's always a board question. It slows us down."

That's not bad governance. That's the cost of accessing institutional capital.

Both relationships can be healthy. They're just different. Know the difference before you commit.

Emerging trends: angel syndicates, micro-angels, and geographic shifts

The angel-VC landscape is changing faster than most founders track. The solo angel writing $100K checks is outdated. Here's what's happening in 2024-2025:

Angel syndicates are replacing solo angels.

Pooled capital with a lead investor coordinating due diligence and terms. This scales angel capital without creating mega-firms.

The lead angel provides expertise

The syndicate provides capital

What I'm seeing with the founders I work with: syndicates now dominate pre-seed and seed rounds in major hubs.

Micro-angels are growing fastest.

Checks of $5K–$25K from emerging investors

These are people in their late 30s and 40s who had one successful exit and now back early-stage companies part-time

The micro-angel base is democratising early-stage capital.

Geography is shifting dramatically.

Per Angel Capital Association data, Asia-Pacific angel investment is growing 25%+ annually. North America remains the largest absolute market, but its relative share is declining. Founders outside the U.S. now access more angel capital than they did 3 years ago.

Sector concentration in angel deals:

According to recent market data, tech accounts for 40% of angel deals in 2025. AI and deeptech are becoming specialist sub-categories with their own lead angels and syndicates. If your company is outside these buckets, you'll find fewer angels but more specialized ones who understand your sector deeply.

The VC market consolidates differently. 8% of deals (117 mega-rounds) captured 75% of all VC capital in 2024, according to Statista VC investment data. Institutional capital concentrates around proven mega-scale teams.

Angels and syndicates spread capital more widely.

What I'm tracking in the current market:

Seed VCs are increasingly focused on AI companies

Early-stage VC funds are consolidating or closing

Mega-firms (those managing $5B+ in assets) are winning the institutional capital war.

For founders, this creates opportunity. Angels now have more capital than 3 years ago, and they're more organised. VCs concentrate firepower on mega-deals and AI, meaning mid-market founders face less competition if they're not chasing unicorn growth.

How to pitch differently: the story vs. data angle?

The split between angel capital vs venture capital shows most clearly in the pitch. Your core material is the same, but emphasis shifts. Pitch deck design gets this distinction right by tailoring narrative to investor type.

An angel pitch emphasises story and founder relationship. Open with: Why did you start this? What did you see that needed fixing?

Angels back founders first, companies second.

They want conviction, persistence through setbacks, and the sense that you've lived the problem.

They evaluate founder-problem fit.

Angel opener: "I spent five years in [industry]. Saw founders struggling with [problem]. No one built [solution], so I did.

We've got 30 paying customers and we're validating this problem is real."

A VC pitch emphasises metrics and market.

Open with the three questions VCs always ask:

How big is the market?

What's your competitive advantage?

What traction proves it works?

Paul Graham's essay on fundraising captures this dynamic well: VCs are pattern-matching against the handful of deals they've seen succeed at scale.

VCs back businesses and scalability, evaluating the pattern, proof, and path to scale.

Angels look for founder conviction; VCs look for repeatable unit economics.

VC opener: "We're building the standard for [category] in a $10B market growing 40% annually. Customers spend $200K/year on manual processes we automate. CAC payback: 6 months.

NRR: 120%. ARR: $1.5M in 18 months."

Same company, same founder, different emphasis. One pitch feels relational, the other analytical. Both are true, but the emphasis matters.

Angel investors vs. venture capitalists: pros, cons, and the hybrid path

Strategic choice beats desperation every time.

Angel pros: Speed (weeks, not months)

Flexibility

Lightweight docs

Angel cons: Limited capital (capped by personal wealth).

No operational support at scale

Dependent on single investor who might flake.

VC pros: Large checks.

Professional operational support (recruiting, press, strategy). Institutional credibility.

VC cons: High entry bar (must have product-market fit).

Board involvement (less autonomy)

Pressure for 3x growth annually

The hybrid path follows this: raise $500K–$1M from angels.

Over 12-18 months, hit product-market fit, $800K–$1.2M ARR, 2-3x monthly growth.

Then approach Series A VCs with undeniable traction and close $2M–$5M. Angel capital funded the risky phase; VC capital funds the scaling.

A SaaS founder I worked with raised $600K from an angel syndicate over 9 months. That capital proved go-to-market and landed her first 20 enterprise customers. Twelve months later, she closed a $2.5M seed round in 6 weeks.

The angel syndicate took a bigger equity stake because of early risk; the seed fund took a smaller stake because the risk was lower. The founder owned more equity than if she'd gone institutional-only. That's the hybrid model working.

For deeper data on funding rounds and investor activity, Crunchbase's venture database is the best free resource available for tracking real deal flow by stage and sector.

My direct assessment

The funding choice confusion is almost always a stage mismatch dressed as investor preference. Founders don't fail to raise because they picked the wrong investor. They fail because they pitch Series A VCs at $200K ARR and get soft passes, or they stay with angels too long and miss the window when their growth metrics mattered.

Stop asking which investor is better

Start asking which investor fits your metrics today

Angels and VCs each serve specific stages; your current metrics determine the right fit.

Founders who get this decision right move 40-60% faster through funding cycles. Founders who don't spend 9-12 months pitching the wrong investors, burning goodwill, and watching runway shrink.

One more thing most content won't say: angel syndicates in 2024-2025 run more rigorous diligence than many seed funds did five years ago. Walk in thinking it's casual and you'll get surprised.

Treat every pitch with institutional rigour. The bar's risen. The capital available at that bar is also larger than most founders realise.

How spectup helps

We work with founders at the inflection point between angel and institutional capital. Our fundraising consultant practice builds the strategy, materials, and outreach that matches your stage, not the stage you wish you were at.

We help you assess whether your metrics fit angel rounds, angel syndicates, or Series A; build the financial model and data room angel clubs now demand; and develop pitch narratives that shift from founder story (angel) to traction and market data (VC). We've seen both investor types: Niclas's VC Scout background at Flashpoint gives institutional perspective, and our client work spans pre-revenue startups through Series B-ready companies.

If you're unsure which stage fits your metrics, our investor outreach service through personalized outreach: the right list, the right materials, the right investor type.

The bottom line: choosing your funding path

Angel capital and venture capital aren't competing options. They're sequential stages. Your job: pick the right investor for your current stage and metrics.

An idea and prototype mean angels; $1M ARR and growth mean VCs. Flipping that order is the expensive mistake most founders make.

Angel syndicates and micro-angels mean early-stage capital is more accessible than 5 years ago. VC consolidation around mega-deals means institutional capital is more competitive for the mid-market. But this shift creates opportunity for founders who understand the distinction and time raises correctly.

Get your stage right, and your timeline compresses from 9 months to 4 months. Get it wrong, and you'll spend a year pitching the wrong investors, getting educated rejections, and rebuilding the narrative. The investors aren't the problem; the mismatch is.

Concise Recap: Key Insights

Angel investors are personal, VCs are institutional.

Angels invest their own capital in idea-stage companies; VCs manage pooled funds for Series A+. Different capital sources drive different behaviors: angels accept founder risk, VCs demand operational proof.

Angel clubs demand rigor modern founders miss.

Today's angel syndicates run institutional-grade due diligence, financial models, customer references, cohort data. Founders unprepared for this rigor lose credibility within 10 minutes of the pitch meeting.

Your metrics determine which investor fits.

Pre-seed ideas need angels; $1M+ ARR with 2-3x growth needs Series A VCs. Picking the wrong investor type adds 6+ months to your timeline and costs you equity.

Frequently Asked Questions

What is the main difference between an angel investor and a venture capitalist?

Angels invest personal wealth in early-stage ideas; VCs invest pooled institutional capital in companies with traction. Angels back founders and potential; VCs manage institutional capital and back teams with proven metrics. The key difference: angels bet on the founder and story, VCs bet on the metrics and trajectory.