Table of Content

Summary

LPs only really negotiate 7-8 clauses

Everything else in the limited partner agreement is settled paper. Walking in with a pre-decided list compresses negotiation from a year to months.

[01]

The real LPA increasingly lives in side letters

Post-Fifth-Circuit, institutional LPs rebuild SEC-rule protections contractually. A triage framework cuts a side-letter round from four weeks to two.

[02]

MFN propagation is the binding constraint

A $187,500 anchor concession became $4.5M of lost fees over a 10-year fund life when six of eleven LPs elected MFN on a hypothetical $300M fund.

[03]

ILPA Template 2.0 re-opens 2026 LPAs

The new template expands fee disclosure from 9 to 22 categories. LPs are pulling closed funds back to the table on chargebacks and subscription interest.

[04]

Three-phase advisory beats clause-by-clause defense

Pre-LPA term sheet alignment, side-letter triage during the roadshow, and post-close MFN management prevent Year 3 propagation surprises.

[05]

A first-time fund manager in Munich, "GP-Alpha-7", opened the email at 11pm on a Wednesday. The anchor LP's lawyers had returned the draft limited partner agreement after eighteen days of silence. The cover note was four lines.

The redline was forty-seven pages. He called me on Thursday morning, and the first thing he said was, "I don't know what the line is and what the negotiation is."

That's the situation every emerging-manager GP walks into the first time they raise institutional capital.

Fund counsel is paid to keep the document opaque. Institutional LPs are paid to extract every concession a slow-moving GP will leave on the table.

The advantage tips the GP who walks into the negotiation knowing exactly which seven or eight clauses are actually in play and where the market midpoint sits on each one.

Most first-time fund managers assume the whole document is up for grabs and they have to defend forty pages. In reality, LP counsel only fights for seven or eight clauses. Defending the rest just signals you don't know which fights matter.

I run capital advisory at spectup, and a meaningful slice of our work is on the GP side of fund formation. The pattern is consistent across debut funds and Fund II step-ups: LPs only really negotiate a known core. Everything else in the LPA is settled on paper.

This post is the negotiation map for the modern limited partner agreement in 2026, with the 1Q-2026 ILPA Reporting Template 2.0 inflection and the post-Fifth-Circuit side-letter regime baked in.

The LPA vocabulary, in plain words

LPA negotiation comes with its own vocabulary. After roughly 15 fund-formation calls across the last 18 months, here are the 14 terms I see emerging managers stumble on most often. If you've never sat through a fund-formation call before, the next sections move faster if these are in your head first.

LPA: Limited partnership agreement.

The contract that defines the partnership: the limited partner side commits capital, and the general partner side runs the fund. Some counsel call it the "limited partner" agreement and others the "limited partnership" agreement, and the SERP treats both wordings interchangeably.

The partnership limited partner structure has been the institutional fund vehicle since Delaware modernised the form in 1988.

GP: General partner, or we can say it's the fund manager.

Runs the fund, makes investment decisions, carries unlimited liability and earns the carry.

LP: Limited partner.

The capital provider, typically a pension, endowment, family office, or fund-of-funds writing 5-150M tickets. Liability is capped at committed capital so long as the LP stays passive on investment decisions.

LPAC: Limited partner advisory committee.

A small group of LPs (usually 3-7) that the GP consults on conflicts, valuations, and key-person events.

Side letter:

A bilateral contract between the fund and a single LP that grants bespoke rights (fee discounts, enhanced reporting, regulatory carve-outs, co-invest priority).

MFN: Most-favoured-nations clause

The mechanism that lets one LP elect into rights granted to other LPs via side letter is usually within a 30-60 day election window after each closing.

Key person:

Named individuals whose departure or reduced commitment triggers an automatic suspension of the fund's investment period.

GP commit: The GP's own dollars committed to the fund

In our experience across recent debut-fund mandates, 1-2% of fund size is the market for first-time managers, often higher for established GPs.

Carried interest: The GP's share of fund profits above a hurdle

The market sits at 20% for venture and 20-25% for established PE, consistent with the Hamilton Lane PE fee primer linked below.

Hurdle / preferred return

The minimum annualised return LPs must receive before the GP takes carry. 8% compounding remains the institutional default in PE.

. Waterfall: The order in which fund cash flows back to LPs and GP

"Whole-of-fund" (European) returns capital plus hurdle before any carry; "deal-by-deal" (American) takes carry on each profitable deal with a clawback at the end.

Clawback

The GP's contractual obligation to return excess carry if final fund returns fall short. Standard market is full clawback plus interest.

Recycling:

The GP's right to redeploy distributed capital. The cap sits at 120-125% of commitments in most institutional LPAs before the investment period ends.

Management fee offset:

The percentage of transaction, monitoring, or director fees that reduce the management fee LPs pay. The market has moved from 50% to 100% over the last decade.

ILPA model LPA:

The Institutional Limited Partners Association's published template (whole-of-fund and deal-by-deal), originally released in October 2019 and revised in July 2020. The closest thing the asset class has to a neutral starting point.

What is a limited partner agreement?

The short answer is a limited partner agreement is the constitution of a private fund. It is the contract between the general partner that runs the fund and the limited partners who commit the capital, governing economics, governance, and what happens when things go wrong.

Most LPAs run 50 to 150 pages and govern a fund life of 10 to 12 years, and the limited partner form is the legal vehicle every institutional LP underwrites against.

The naming is confusing on purpose. The "limited partner" form and the "limited partnership" form of the name refer to the same document. Google hasn't resolved the wording overlap; Carta, ILPA, and the law firms treat them as interchangeable.

Use whichever your counsel uses. The document doesn't change.

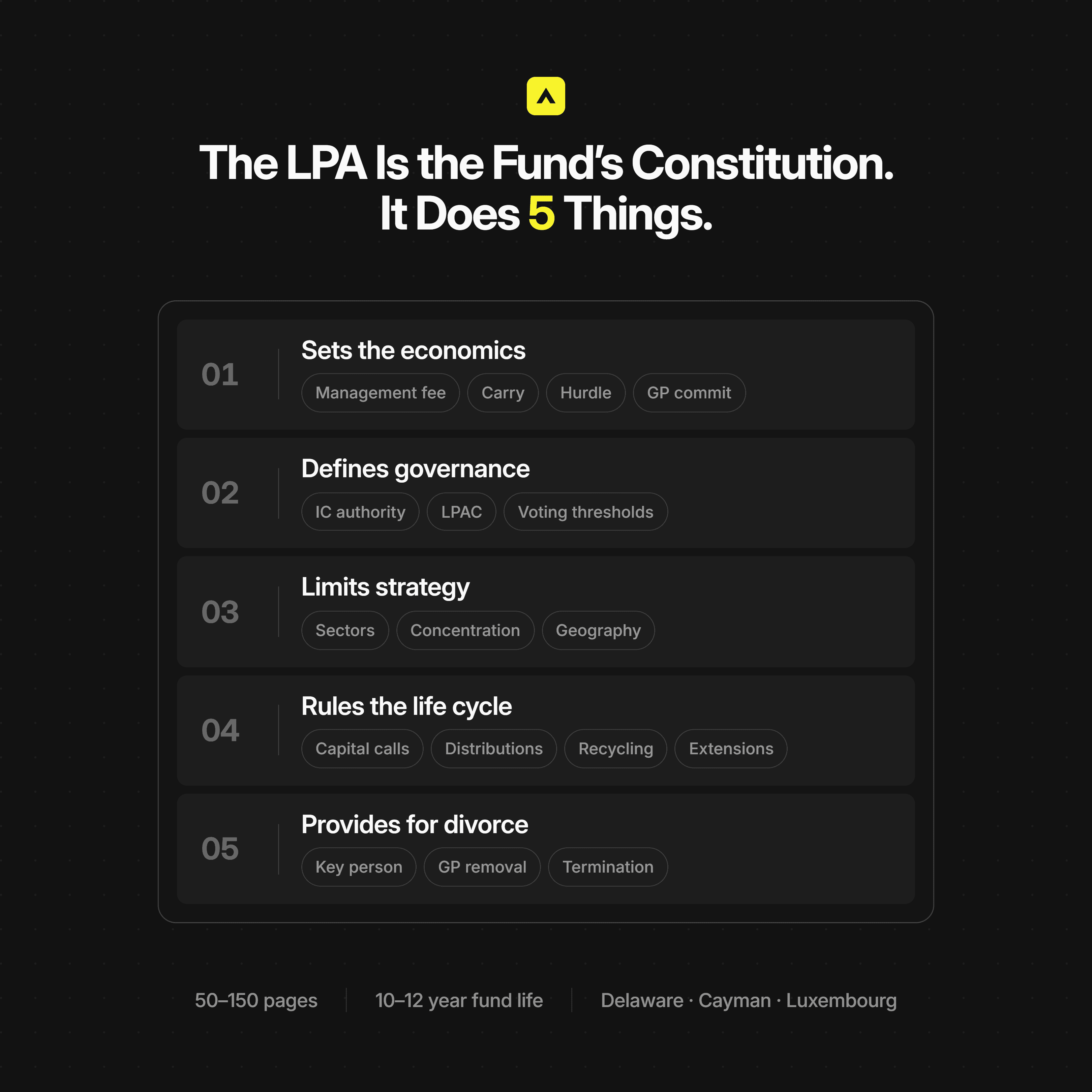

The LPA does five things, and the 2022 ILPA model LPA organises them in roughly this order:

It sets the economics (management fee, carry, hurdle, GP commit).

It defines the governance (investment committee authority, LPAC, voting thresholds).

It limits the strategy (sector restrictions, concentration limits, geographic scope).

It sets the rules for the fund's life cycle (capital calls, distributions, recycling, term extensions).

It provides for divorce (key person triggers, GP removal, fund termination).

LPA dimension | Typical 2026 market |

|---|---|

Document length | 50-150 pages |

Fund life | 10 years + two 1-year GP extensions |

Investment period | 4-5 years |

Governing law | Delaware (US) or Cayman (offshore); Luxembourg (EU) |

Parties | GP entity + LP investors + manager (if separate) |

A useful frame: the on-page LPA is what the regulators and auditors see. The real economics increasingly live in the side letters, sometimes 14 pages of them per anchor LP. We will return to this several times.

Limited partner vs general partner: who is on which side of the LPA?

The asymmetry between the limited partner and the general partner is the structural reason the LPA exists at all. The general partner versus limited partner split runs through every clause:

The GP runs the fund and carries unlimited liability for its decisions

The LP commits capital and carries no liability beyond the commitment, so long as the LP stays passive.

That trade was the original innovation of the limited partnership form when Delaware codified the modern Revised Uniform Limited Partnership Act in 1988, and every clause in the partnership limited partner structure pivots off it.

Founders who only know operating-company equity sometimes ask what is limited partner status really worth. The short answer: liability protection in exchange for total passivity.

For founders who have only ever raised equity into an operating company, the "what's a limited partner in business?" The question lands differently than it does in fund land.

In an operating partnership, an LP is a silent capital provider

In a private fund, an LP is an institutional investor running its own underwriting process on the GP's track record and team

The asymmetry of information in the general vs limited partner setup is the opposite of a startup raise.

Dimension | General partner (GP) | Limited partner (LP) |

|---|---|---|

Liability | Unlimited (entity layer mitigates) | Limited to committed capital |

Control | Day-to-day investment decisions | Passive; LPAC consultation only |

Capital contribution | 1-2% GP commit (typical) | 98-99% of fund size |

Fees received | Management fee + carry | None received; pays the management fee |

Carried interest | 20% standard; 25% for established managers | None; receives 80% of profits above hurdle |

Fiduciary duty | Owes duty to the fund and to LPs | None owed to GP or other LPs |

Removal exposure | For-cause and no-fault removal both possible | Effectively can transfer only with GP consent |

Typical entity | LLC + GP LP layer (Delaware) | Pension, endowment, family office, fund-of-funds |

One detail competitor posts rarely mention: the limited partner versus general partner distinction isn't a status. It's a behaviour test. The general partner versus limited partner trade only holds while the LP stays on the right side of it, and the limited partner versus general partner line gets enforced by passivity, not by paperwork.

If an LP starts to direct investment decisions:

Take a board seat under the GP's authority

Or sign on the fund's behalf; that LP can lose its limited-liability shield.

Hustle Fund's primer calls this the "99 LP problem" because the Section 3(c)(1) cap most US VC funds rely on is set at 99 limited partners.

The cap is structural; the passivity test is behavioural. The limited partner vs general partner line is something an LP can cross by accident, just by acting like a GP, and the general vs limited partner protection collapses with it. The limited partner versus general partner distinction also dictates what counsel can cover in the LPA at all: the GP carries fiduciary duties that the LP simply doesn't.

Sophisticated LPs sometimes try to walk right up to the limited partner vs general partner line by inserting consent rights into side letters. Done badly, this collapses the general vs limited partner shield the moment the LP exercises one of those rights.

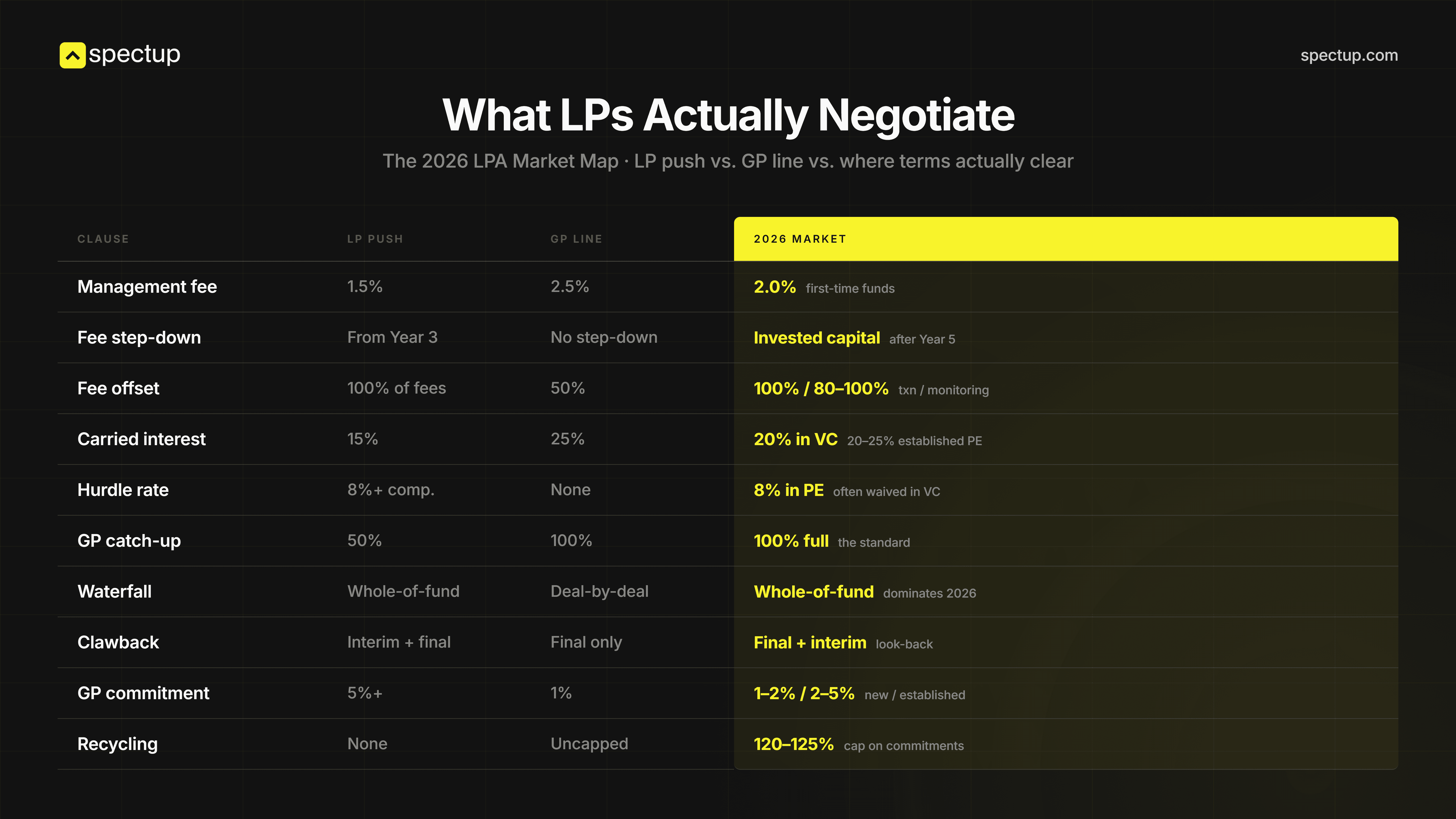

Which economics does an LP always negotiate, and where can a GP hold the line?

Of the seven to eight clauses LPs actually push in the limited partner agreement, all but one or two sit on the economics. Here is the negotiation map I run through with first-time fund managers, often alongside the financial modeling consultant on the deal, before they open the markup.

Clause | LP standard push | GP hold the line. | 2026 market midpoint |

|---|---|---|---|

Management fee rate | 1.5% | 2.5% | 2.0% for first-time funds; 1.75% for established |

Fee base step-down | Invested capital after Year 4 | Committed capital through Year 6 | Invested capital after Year 5 |

Management fee offset | 100% of transaction/monitoring fees | 80% | 100% on transaction; 80-100% on monitoring |

Carried interest | 15-20% | 20-25% | 20% (venture); 20-25% (established PE) |

Preferred return / hurdle | 8% compounding | None (venture) or 6% | 8% compounding for PE; often waived for venture |

Catch-up | 50% partial catch-up | 100% full catch-up | 100% full catch-up is standard |

Waterfall | Whole-of-fund (European) | Deal-by-deal (American) with strong clawback | Whole-of-fund dominates new institutional funds in 2026 |

Clawback | Full, joint-and-several, interim true-ups every 3 years | Full at fund end, individual | Full at fund end + interim look-back; joint-and-several rare |

GP commit | 2-5% | 1% | 1-2% for first-time funds; 2-5% for established |

Recycling cap | 110% of commitments | 125% | 120-125%, often limited to first 4 years |

The fee step-down is where I see the most heat in first-time LPA negotiations. The Munich GP who called me at 11pm? His anchor LP had pushed the step-down to invested capital after Year 5 and demanded a 100% transaction-fee offset.

From our experience on that mandate, both were in the 2026 market range. He couldn't push back on either without giving up something else. We traded the step-down for a slightly higher GP commit and held the management-fee rate at 2.0%.

The whole exchange closed in a single LPAC call.

The bigger fight in 2026 isn't the rate.

It is the waterfall. SVB's emerging-manager guide still describes deal-by-deal as a viable option for venture, but institutional LPs are increasingly insisting on whole-of-fund even for venture. EBAD law's note on GP-LP negotiations traces the same shift: by 2026, the deal-by-deal waterfall is mostly a debut-fund concession, not a market default.

"The carry rate gets the attention. The waterfall and clawback structure determine what the GP actually takes home. Trade rate for structure if you have to choose."

For the hurdle, venture LPs are still mostly willing to waive an 8% preferred return on technology funds. PE LPs aren't. The Hamilton Lane PE fee primer walks through why 8% has survived 25 years of fee compression: it's the line below which institutional LPs can earn comparable risk-adjusted returns in public credit.

Anything beneath it doesn't justify the lock-up.

Key person, GP removal, and the governance clauses an LP uses for bargaining power

The economics are the loudest fight. The governance clauses of the LPA are the structural ones. If a deal blows up, this is the section that determines what happens to the fund.

Start with the key person. A key person clause names two to four individuals whose departure or reduced commitment to the fund triggers an automatic event:

Most commonly a 90-day suspension of the investment period

A written cure or replacement plan during a 90-180 day window

A vote of LPs (usually 66.7-75%) to either reinstate the investment period or terminate it early

Adam Schwab's note on key person clauses walks through the trigger language LPs actually accept.

The narrower the key-person definition, the more diligence risk a Fund I GP carries. I had a debut fund last year, "GP-Beta-3", where the anchor LP's first markup pulled the named key persons from two to four. The GP pushed back: two of the four were Partners hired in the last 18 months without a track record.

After three calls, we landed on three named key persons (the founder, the senior partner, and the head of platform) with a "lookback" provision that converted the original two into "originally named key persons" with a separate trigger. The compromise cost an extra fortnight of legal time. It also let the GP hire a fourth partner the next year without triggering an LP vote.

GP removal is the other governance lever. The modern market splits removal into two paths.

For-cause removal (fraud, criminal conviction, material LPA breach) requires a simple majority of LPs and is functionally automatic if proven.

No-fault removal (the "no-fault divorce") requires a supermajority, typically 66.7% to 75% of LP commitments.

The for-cause path is non-negotiable. The no-fault threshold is.

66.7% threshold: The institutional baseline. Standard for established GPs raising Fund III+.

75% threshold: The default starting position for emerging managers. LPs accept higher thresholds when the GP has less of a track record to fall back on.

80% threshold: Rare in 2026. A first-time GP can occasionally get here if the anchor LP is itself strategic.

The LPAC sits underneath both. It's the body the GP consults on conflicts, valuations, key-person events, and certain related-party transactions. Composition is usually:

Three to seven LPs (anchor plus large institutional commitments)

Quorum is typically a majority of LPAC members holding more than 50% of LPAC commitments

LPAC votes are usually non-binding on the GP except where the LPA explicitly says otherwise.

The trap for first-time GPs is consenting to a binding LPAC vote on too wide a range of decisions. Keep the binding scope narrow: conflicts, related-party deals, and key-person reinstatement only. The same principle applies to founder boards (see our breakdown on startup term sheets).

Side letters: where the real LPA actually lives

The on-page limited partner agreement is becoming the public-facing skeleton. The side-letter regime is the real economic deal. If you only read one section of this post, read this one.

Six categories cover the vast majority of side-letter requests against the LPA I see in 2026:

Fee discounts tied to commitment size or anchor status (10-50 bps off the management fee; rarely off carry)

Enhanced reporting beyond the standard ILPA template (custom cuts, monthly NAV, look-through to portfolio detail)

Excuse rights from specific investments (sin sectors, sanctions overlap, regulated industries)

Regulatory accommodations (ERISA plan asset, FOIA, non-US tax treaty, sovereign immunity, public pension reporting)

Co-invest priority on deals above a certain size (right of first offer, allocation formula tied to commitment)

Transfer and withdrawal rights beyond the LPA default (assignability to affiliates, secondary sale rights)

Then the Fifth Circuit changed everything. On June 5, 2024, the US Court of Appeals for the Fifth Circuit vacated the SEC Private Fund Advisers Rule in its entirety, including the Preferential Treatment Rule that would have forced disclosure of side-letter terms to all LPs. Two years later, the practical effect is paradoxical.

The prescriptive disclosure mandates went away. The institutional LP demand for the rights those rules would have guaranteed didn't. As Sidley flagged in their June 2024 alert, LPs immediately started rebuilding the same protections contractually inside side letters.

One placement-process file in our pipeline last quarter, "GP-Delta-2", received an LP markup that added fourteen pages of side-letter requests. The bulk of them were enhanced reporting and preferential redemption rights. Read line by line, they mirrored the now-vacated Preferential Treatment Rule almost verbatim.

The LP's counsel was rebuilding the SEC rule inside the contract. We had to triage every request against MFN exposure. We refused some, negotiated others, and accepted the ones tied to the LP's specific regulatory status with MFN carve-outs to prevent propagation.

That triage step is what most first-time GPs miss. Without a triage framework, the easiest thing to do is grant everything to close the round. Six months later, when the next LP elects MFN, the GP discovers the cost.

First-time managers assume that granting a side-letter concession to close the anchor is free money. In practice, the cost shows up eighteen months later as MFN propagation across half the LP base, and by then it isn't renegotiable.

Our team handles this work in parallel with the LP roadshow and investor outreach service for the fund, typically spanning 8 to 14 weeks of LP counsel back-and-forth on a debut fund.

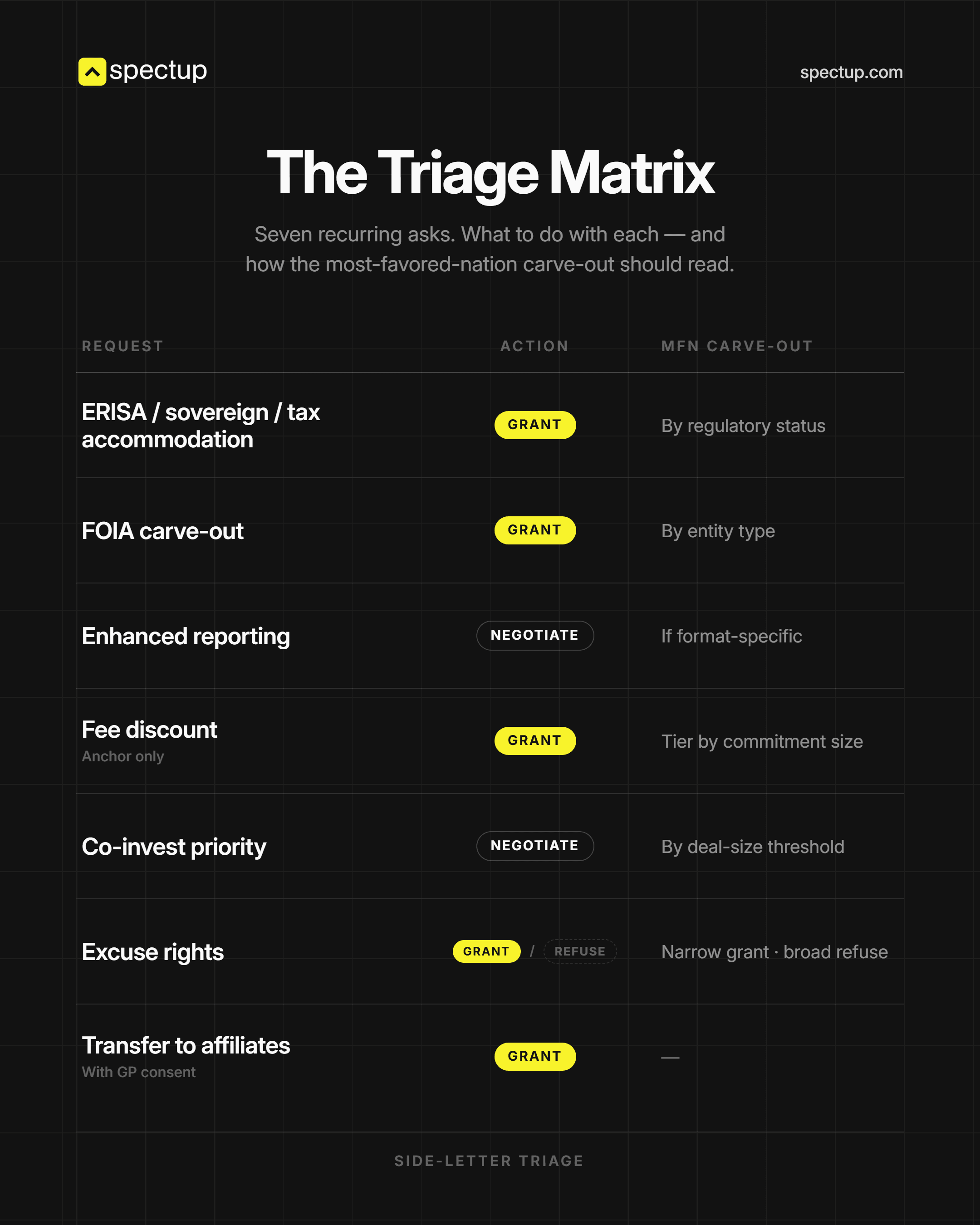

Request type | Default action | MFN carve-out? |

|---|---|---|

ERISA / sovereign / tax-treaty accommodation | Grant | Yes, tied to LP regulatory status |

FOIA / public-records carve-out | Grant | Yes, tied to LP entity type |

Enhanced reporting (custom cuts) | Negotiate | Yes if format-specific; No if substantive |

Fee discount (anchor-tied) | Grant for anchor, refuse for follow-ons | Yes, explicit commitment-size tier |

Co-invest priority | Negotiate scope (deal size threshold) | No if framework-level; Yes if commitment-tied |

Excuse rights (single sector) | Grant if narrow, refuse if broad | No, substantive, MFN-shareable |

Transfer rights to affiliates | Grant with GP consent backstop | No, standard market |

Most-favored-nations election itself | Grant in tiers | N/A, this IS the MFN |

The framework isn't the value. The triage discipline is. A GP who walks into an LP-counsel call knowing which bucket each request falls into closes a side-letter round in two weeks.

"The post-vacatur side-letter regime is more LP-friendly than the SEC rule it replaced. Institutional LPs got contractually what the regulator tried to give them by mandate. The GPs who acted like the vacatur was a win lost six months of bargaining position they didn't know they had."

A GP who treats every request as a one-off takes four.

MFN clauses: how one side letter reshapes the whole fund

Most-favoured-nations clauses inside the limited partner agreement are the mechanism that turns a single concession into a structural reset. The math gets ugly fast.

From our experience modelling these scenarios for GPs, consider a hypothetical $300M fund with twelve institutional LPs. The anchor commits $75M (25% of the fund) and negotiates a 25 basis-point management-fee discount on its commitment. Stand-alone, that's a $187,500 annual fee reduction.

Then the other eleven LPs elect MFN. From our experience modelling this, if six of them have MFN rights that include fee terms and they all elect, the discount applies to roughly 60% of the fund. The annual revenue hit to the manager moves to around $450,000.

Over a ten-year fund life, that's $4.5 million of fee revenue the GP didn't budget for off a single anchor concession.

That's the propagation problem in one paragraph. Foley's October 2025 NVCA model document update flagged the same issue in their commentary on the latest model docs: more institutional LPs in 2025-2026 are demanding broader MFN scope, and the standard structural fix is tighter carve-outs.

Five carve-outs handle most of the propagation risk:

Commitment-size tiers. The most powerful structural fix. MFN elections are limited to terms granted to LPs with commitments equal to or smaller than the electing LP's commitment. A $10M LP can't elect into a $75M anchor's fee tier.

Regulatory and legal status carve-outs. Terms granted because of a specific LP's regulatory status (ERISA, public pension, sovereign, non-US tax) are explicitly excluded from MFN. The electing LP would have to actually be in that regulatory category to claim those rights.

Strategic-relationship carve-outs. Terms granted to a strategic LP (corporate, sponsor, fund-of-funds with a separate commercial agreement) are excluded. The carve-out has to be narrow or it becomes a loophole.

Election windows. MFN elections must be made within a defined period after each closing (usually 30-60 days). Outside the window, the right lapses on terms granted in that closing.

Substantive vs. format carve-outs. The distinction between substantive terms (economics, governance) which are MFN-shareable and format terms (reporting cadence, custom cuts) which are LP-specific.

The discipline a GP needs is to write the MFN carve-outs into the LPA itself, not just into individual side letters. If you carve out only in the side letters and not in the LPA's MFN clause, the carve-out is contestable. Morgan Lewis's deskbook on the NVCA model documents walks through the LPA-level language.

Worth the read before the first closing.

What did the 2026 ILPA template changes reopen (and what didn't)?

The Institutional Limited Partners Association released its Reporting Template 2.0 in January 2025. The new template is effective for funds in their investment period as of 1Q 2026 and for all new funds with first closings after January 1, 2026. The headline change is the expansion of fee and expense disclosure from nine to twenty-two categories, with new line items for subscription-facility interest, placement fees, partner transfer costs, and internal chargebacks.

Reporting Template 1.x (pre-2026) | Reporting Template 2.0 (1Q 2026+) |

|---|---|

9 fee and expense categories | 22 fee and expense categories |

Subscription-line interest aggravated | Subscription-line interest broken out |

Placement fees often netted | Placement fees disclosed gross |

Internal chargebacks not specified | Internal chargebacks disclosed separately |

Carry calculation methodology static | Methodology unchanged; only reporting expanded |

Quarterly cadence (most funds) | Quarterly cadence preserved |

For LPs that adopted Template 2.0 in their side-letter reporting clauses (a "then-current ILPA reporting template" reference is standard), the new template reopens negotiations on the limited partner agreement itself. RSM's essential insights piece on the new standards walks through the implementation timing.

I had a Fund III GP, "GP-Gamma-12", receive a Template-2.0 side-letter amendment request from a US public pension LP in late January 2026. The request was three pages. Two of those pages were chargeback disclosures (internal allocations from the manager's platform team to the fund).

The GP had never disclosed those allocations because the prior template didn't require it. The negotiation took six weeks. The GP eventually agreed to disclose chargebacks above a $50,000-per-quarter threshold, with the LP accepting that minor allocations would remain aggregated.

The compromise let the GP avoid an expensive re-platforming of the fund's internal accounting.

What Template 2.0 did not reopen:

Carry calculation

Management fee rate and hurdle.

The template is about transparency, not economics. LPs that thought the new template would give them a lever to renegotiate carry were quickly corrected by counsel.

Most GPs assume the post-Fifth Circuit vacatur made their lives easier because the SEC mandates disappeared. In reality, institutional LPs immediately rebuilt the same protections inside side letters, and the contractual version is harder to push back on than the regulatory one was.

The lever is real, but it only reaches reporting.

The 2026 inflection compounds with two other shifts. The ILPA Model LPA (whole-of-fund and deal-by-deal) remains the institutional reference template. The NVCA model documents were updated in October 2025 and now include refreshed language on side-letter MFN scope.

And the post-Fifth-Circuit side-letter practice has consolidated around contractual reconstruction of the vacated SEC protections. For an LP with sophisticated counsel, 2026 is the moment to reopen every clause that referenced "then-current" anything. For a GP, it's the moment to harden every cross-reference.

How spectup advises a GP through limited partner agreement negotiation?

I've been on the GP side of more than a dozen first-time LPA negotiations in the last 24 months, and the moments where a debut manager loses the deal are nearly identical every time. It's rarely the rate. It's the absence of a triage system going into the LPAC call.

The GP who walks in with seven clauses pre-decided closes faster than the GP who walks in trying to defend forty.

Our work as a fundraising consultant on fund formation runs in three phases. Pre-LPA, we align with the anchor LP on the economics term sheet before counsel drafts the LPA. The goal is to walk into the drafting with the rate, carry, hurdle, and waterfall already agreed.

The LPA draft and side letter triage run through the roadshow: every LP-counsel markup gets routed through a single triage framework so the GP isn't making isolated trade-offs. Post-close MFN management is the unglamorous part that prevents the propagation problem from showing up in Year 3.

None of this replaces a good fund-formation lawyer (Morgan Lewis, Sidley, or your equivalent). It sits alongside one. For founders who want adjacent context, our piece on silent partner vs investor walks through the entity layers behind the LPA.

If you're an emerging GP raising your first institutional vehicle and your anchor LP just returned a 40-page markup with 7 clauses already pre-decided, that's the moment to call.

Where would I actually focus if I were closing an LPA in 2026?

Honestly, after enough of these fund-formation calls, I've stopped pretending the LPA is an even fight. It isn't. The document is opaque on purpose; fund counsel is paid by the page, and the institutional LP across the table has done this a hundred times more than the debut GP.

What I tell every emerging manager who walks in with a 40-page redline is this: don't try to win the whole document. You can't. Pick the seven or eight clauses that actually move money in your 10-year fund life, decide your line on each, and walk in before counsel opens its laptop.

If I were sitting in the GP seat today, I'd spend the bulk of my prep on three things and nothing else.

One, the waterfall.

Trade rate for structure every time. A whole-of-fund waterfall with full clawback is worth more than 25 basis points on carry, and most first-time GPs get this exactly backwards.

Two, the MFN carve-outs in your LPA

Write them into the agreement itself, not into side letters. I've watched that surprise cost a manager $4M on a single anchor concession when the next LP was elected.

Three, the key-person definition

Narrow lists protect the GP; wide lists protect the LP. The compromise is a tiered structure that lets the GP grow the firm without triggering a vote, and most debut managers concede this without realising they've capped their own hiring for a decade.

Everything else is settled on paper. Stop negotiating it.

The 2026 inflection, ILPA Template 2.0 plus the post-vacatur side-letter regime, doesn't change the map. It just raises the cost of getting it wrong.

The GP who treats every clause as a one-off takes a year to close. The one who walks in with seven decisions already made closes in months.

That's the entire difference, and it's the only part of this job I'd actually call learnable.

Concise Recap: Key Insights

LPs negotiate a known core, not the whole document

Of 100+ pages in an LPA, seven or eight clauses are actually in play. Pre-decide the line on each before opening the markup.

Side-letter triage is the new fund-formation skill

Without a grant/negotiate/refuse/MFN-carve-out framework, GPs grant everything to close the round and pay the cost six months later when LPs elect.

The 2026 inflection re-opens settled clauses

ILPA Template 2.0 plus the post-Fifth-Circuit side-letter regime mean reporting and preferential-treatment clauses are back on the table this year.

Frequently Asked Questions

What is a limited partner agreement?

It's the constitution of a private fund. The LPA is the contract between the general partner that runs the fund and the limited partners who commit capital, governing economics, governance, and what happens when the fund or a key person fails. Most LPAs run 50 to 150 pages and govern a fund life of 10 to 12 years.