Table of Content

Summary

Understand the four pillars of VC evaluation

VCs assess every startup through four lenses: founder team, product-market fit, total addressable market, and traction metrics. These pillars form the universal evaluation framework across all funding stages.

[01]

Know that team strength outweighs early metrics

Founder quality and team composition consistently rank as VCs' top priority. A strong team with domain expertise can overcome product shortcomings in early stages. Execution capability matters more than perfection at seed.

[02]

Hit stage-specific metric benchmarks accurately

Seed requires user growth and retention signals; Series A expects $10K–$50K MRR with CAC/LTV ratios; Series B targets $100K+ MRR with payback period under 12 months. Wrong metrics for your stage signal inexperience.

[03]

Validate market size with bottom-up customer evidence

VCs want $1B+ total addressable markets backed by customer conversations, not just analyst reports. Market timing and competitive positioning within the TAM matter as much as absolute size estimates.

[04]

Avoid cap table and due diligence red flags

Common deal-killers include unclear founder equity splits, undisclosed convertible notes, option pool issues, and unresolved IP ownership. Clean cap tables and transparent legal documentation accelerate due diligence dramatically.

[05]

After working with over 150 founders and tracking $120M+ in capital raised, we've seen one consistent pattern: founders spend months perfecting pitch decks but miss what VCs actually evaluate. Venture investors follow a systematic framework to assess startups, not intuition or gut feel. Understanding this framework, the specific criteria, weights, and thresholds, is your competitive edge.

This post is specifically about the evaluation criteria:

What VCs score you on\

How they weight each pillar

What the stage-specific benchmarks look like.

If you want the internal VC decision process, how a deal moves from submission to IC vote, that's covered in our separate post on how VCs make investment decisions.

The most successful founders we've advised don't try to impress investors with hype. Instead, they align their materials and metrics to what VCs systematically evaluate. They know the four pillars and stage-specific benchmarks, and they anticipate due diligence questions before they're asked.

The difference between a ten-minute courtesy meeting and a term sheet often comes down to this alignment.

For latest market data on founder concerns and investor behavior, see CB Insights research on VC investment outcomes.

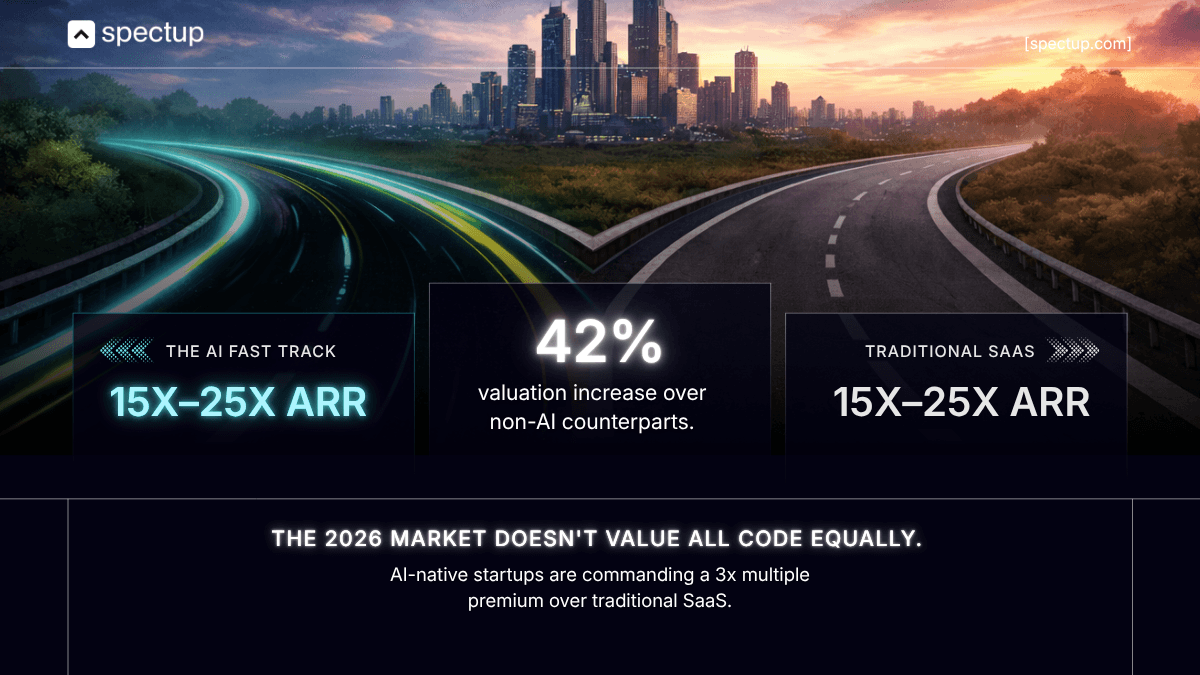

In 2026, this matters more than ever. With 80% of venture capital concentrated in AI funding (according to recent market analysis), non-AI founders face a tighter market and higher bars on team quality and unit economics. This post breaks down the exact framework top-tier investors use and how to position yourself across every stage.

The four pillars: What every VC evaluates:

Whether you're pitching a $500K seed round or a $25M Series B, every VC applies the same foundational evaluation lens: Team, Product, Market, and Traction. These four pillars form the universal language of venture investment and represent the core VC evaluation criteria investors use systematically.

The best early-stage investors evaluate founders and teams first because they know the product, market, and metrics will change. But founder capability is the one constant that determines whether the company pivots, scales, or fails under pressure.

The research is clear on this: Harvard Business Review's analysis of VC myths reinforces that team evaluation dominates early-stage decisions. Here's how VCs weight each pillar:

Pillar | What VCs Evaluate | Weight at Seed | Weight at Series A |

|---|---|---|---|

Team | Founder domain expertise, execution track record, cofounder fit, resilience | 40–50% | 30–40% |

Product | Product-market fit signals, differentiation, customer feedback, retention | 20–25% | 25–35% |

Market | TAM sizing, addressable segments, competitive positioning, timing | 15–20% | 20–25% |

Traction | Revenue, user growth, customer acquisition, unit economics | 15–20% | 20–30% |

Notice the shift:

At seed, team dominates because VCs are betting on founders to handle uncertainty.

By Series A, traction and product-market fit carry more weight because you've had time to prove execution.

But team quality never drops below 30% because VCs know that strong founders course-correct when data changes.

Why team matters more than product (and why vcs fund people first)?

This is where most founders get it wrong: they assume a better product means a better funding outcome. In reality, VCs will fund a great team with a mediocre product before they fund a mediocre team with a great product.

Team strength dominates every investment decision. Here is the breakdown of how your team slide in the pitch can change whole fundraising trajectory within seconds:

Here's why this matters:

Product changes but team doesn't. Market dynamics shift, customer needs evolve, and initial hypotheses get disproven regularly.

But the founders who can learn, adapt, and execute through those changes? That capability is rare and irreplaceable.

We worked with a SaaS founder who had built a feature-rich product but was being rejected by investors. The initial pitch was product-centric, all feature comparisons, technical architecture, and benchmarks. The conversations went nowhere.

When we repositioned the pitch around the founder's 12 years of experience scaling operations at two previous companies, plus her cofounder's track record shipping enterprise software, the narrative shifted entirely. Investors suddenly wanted to meet.

Within four weeks, she had a term sheet from a Series A lead, closing at a $7M pre-money valuation, double what she'd been pitched in her previous round. Same product, same metrics, but the founder story changed everything. That's the power of repositioning around team strength.

VCs look for specifics that YC's essential startup advice also emphasizes:

Domain expertise:

Have you worked in this market before?

Do you understand the customer pain viscerally, or are you solving a theoretical problem?

Execution track record:

Have you shipped before?

What did you build?

Did it grow?

What did you learn from failures?

Cofounder dynamics:

Do your cofounders complement each other?

Who owns product, who owns operations, who owns growth?

Is there clarity or turf wars?

Founder resilience:

How do you respond when your initial hypothesis is wrong?

Can you pivot without ego getting in the way?

A founder with all four of these signals can raise capital on a prototype. A founder with one signal will struggle even with $500K MRR. That's the weight of team evaluation in VC decision-making.

Can domain expertise be built, or do you need it from day one?

Domain expertise accelerates learning but isn't a dealbreaker for exceptional founders. Learning velocity matters more than prior experience.

That said, if you're entering biotech or enterprise SaaS, prior domain work significantly de-risks your pitch, accelerates customer conversations, and can cut fundraising time by several months. New founders entering technical verticals face additional skepticism that relevant domain expertise helps overcome effectively.

Do investors care more about founder experience or market opportunity?

Market opportunity sets the ceiling for returns, but team strength determines whether you capture it. A strong team with a medium market beats a weak team with a huge market.

How VCs assess market opportunity?

Market size is the envelope that determines how big your exit can be. VCs use it as a filter to decide whether a company is worth the effort to build. Most VCs won't fund companies unless the addressable market is $1 billion or larger.

For deeper market sizing techniques, check NFX's guide to founder-market fit, which breaks down how to size markets credibly.

But here's where founders go wrong:

They confuse total addressable market (TAM) with serviceable addressable market (SAM) and serviceable obtainable market (SOM). VCs care about all three, but in different ways.

Market Type | Definition | VC Lens |

|---|---|---|

TAM | Total addressable market, everyone globally who has the problem | Must be $1B+. Is the problem big enough to justify venture returns? |

SAM | Serviceable addressable market, the segment you can realistically serve | Must be defensible. Can you own a meaningful portion of this segment? |

SOM | Serviceable obtainable market, market share you can capture in 5 years | Must be achievable. Is 5-10% penetration realistic given competition? |

VCs verify market size through two methods:

Top-down (analyst reports, market research)

Bottom-up (customer conversations).

Top-down alone isn't credible. A founder we advised landed a Series A by documenting 30+ customer discovery conversations that independently confirmed market demand.

Bottom-up validation was worth more than any analyst report. Market timing matters enormously:

Is this market inflection point here now, or three years away?

A founder pitching enterprise cloud security in 2020 had enormous tailwinds.

Learning how to validate your startup idea before you approach VCs is essential.

The same pitch in 2015 would have struggled because the market wasn't ready. You need timing working for you, not against you. Early customer adoption and third-party market research matter enormously to investors.

What traction metrics VCs actually want?

Traction is how you prove your pitch is real. VCs evaluate different metrics at different stages, and many founders report metrics that signal inexperience. Stage-specific metrics matter more than raw numbers.

A founder reporting monthly active users at seed looks like they don't understand VC priorities. The same founder reporting 30% month-over-month retention and unit economics signals experience.

For a thorough breakdown on which metrics matter most, Andreessen Horowitz's startup guide remains a foundational reference for investors and founders alike.

At seed stage: VCs want to see early signals of product-market fit, user growth rate (month-over-month), retention cohorts showing users coming back, and early revenue if you have it.

Even zero revenue is fine if you're growing users 30%+ month-over-month with strong retention.

At Series A: Investors expect revenue and repeatable customer acquisition with predictable unit economics. The key metrics are customer acquisition cost (CAC), lifetime value (LTV), and the magic number ((Current Quarter ARR - Previous Quarter ARR) × 4 / Previous Quarter S&M Spend). VCs want LTV at least 3x your CAC.

At Series B: The bar is dramatically higher. You need $100K+ monthly recurring revenue, a net revenue retention (NRR) rate above 100% (showing existing customers expand), and a payback period under 12 months. These metrics prove the business model scales profitably.

Here's a common mistake: founders at seed report Monthly active users or signups, when they should emphasize retention and revenue per user. Early metrics that matter to VCs include:

Month-over-month growth rate: 10% MoM is industry-standard expectation. Below that suggests product is not resonating.

Day-30 retention: The percentage of users who return after 30 days. For consumer apps, retention targets vary by business model. For B2B SaaS, 70%+ is typical expectation.

CAC payback period: How many months until you recover the cost of acquiring a customer. Under six months is excellent; 9-12 months is acceptable.

Burn rate: How fast you're spending cash. Burning $50K/month with $20K MRR means you have about 18 months of runway. VCs want to see clear path to profitability or next funding milestone within that window.

The mistake many founders make is reporting metrics that flatter the business without addressing what VCs actually need to validate. Honesty about metrics builds credibility far more than inflated numbers.

VCs don't fund ideas, they fund people they believe will execute on ideas, even as the idea changes. Show us you can learn, adapt, and do what it takes to build something meaningful. That matters more than your initial thesis being perfect.

Due diligence red flags VCs watch for

VCs have seen enough deal failures to know which early signals predict problems later. These raise friction and slow due diligence, though they're not automatic deal-killers. Strong competitive defenses help mitigate risk (see NFX's analysis of defensibility in startups).

Here are the eight biggest red flags:

Unclear founder equity splits:

If cofounders can't articulate who owns what and why, it signals they haven't discussed what happens if someone leaves or performance diverges. Messy equity creates conflict when times get hard.

Undisclosed convertible notes or debt:

Founders who bury existing notes or debt obligations damage trust immediately. VCs will find these in diligence, and the discovery signals you're hiding problems.

Inflated option pools:

Promising 20% of the company in options means either severe dilution later or angry employees.

VCs expect 10-15% pools and will push back hard on anything above 20%.

Unresolved IP ownership:

If your core technology was built with university resources, or a cofounder did initial work before the startup was formed, IP ownership must be crystal clear with legal agreements in place. VCs will not fund ambiguous IP.

Vague revenue recognition:

If your revenue model is confusing:

Are contracts signed?

Has cash been received?

Are there refunds?

VCs assume you're hiding something. Transparent revenue means auditable revenue.

Founder references who don't endorse:

VCs will call your references. If people who worked with you historically give tepid or negative feedback, red flag. Your past behavior predicts future execution.

Inconsistencies between pitch and cap table:

If your pitch says you have a pair of founders but your cap table shows 5 early equity holders with unclear roles, questions immediately arise about decision-making and governance.

No documentation of customer contracts:

If you claim $500K annual revenue but can't produce signed customer contracts or clear delivery evidence, VCs will assume the revenue is not real or not guaranteed to renew.

The best founders we advise clean their cap tables before pitching. They get lawyer letters documenting IP ownership.

They prepare reference lists of customers and past colleagues who can vouch for execution. These moves signal professionalism and accelerate the due diligence process by weeks.

How VCs size return expectations?

VCs don't think in terms of "how profitable is this company?" They think in terms of "what multiple return can we get?" This determines which startups fit their investment strategy.

The venture return thesis is simple:

A 10-year investment needs 10x+ returns to account for risk. Most VC funds expect a portfolio average of 3x returns, knowing that some companies fail while a few outliers return 100x+. To hit 3x portfolio average, individual winners must return much more.

Understanding how to raise venture capital helps founders align their exit expectations with investor incentives.

Expected exit multiples vary by stage and sector:

Seed investors: Expect 10-20x returns over 7-10 years. They're taking maximum risk and need maximum upside.

Series A investors: Expect 5-10x returns. Risk is lower (product proven), but duration is shorter (5-7 year horizon).

Series B and later: Expect 3-5x returns. Exit timelines are 3-5 years, and risk is lower (market validation clear).

For a company to deliver 10x to a seed investor, the exit value must be massive relative to the seed investment. A $2M seed needs a $200M+ exit. That's why VCs obsess over TAM, they're working backward from exit value targets.

This also explains why geographic VCs vary their expectations. A Series A VC in the US expects $100M+ exits.

A Series A VC in Southeast Asia might target $20-30M exits because of different market sizes and exit liquidity. Your geography influences the investor pool that fits your company.

Stage-specific expectations: What do vcs look for by funding round

What VCs evaluate changes dramatically as your company matures. Early-stage VCs weight founder quality and vision heavily, while late-stage VCs focus on unit economics and predictable scaling.

Understanding stage-specific expectations is critical to positioning yourself correctly.

Evaluation Factor | Seed Stage | Series A | Series B |

|---|---|---|---|

Revenue expectation | $0–$25K MRR (nice-to-have) | $10K–$50K MRR (required) | $100K+ MRR (required) |

Growth rate | 20–30% MoM acceptable | 15–20% MoM expected | 10% MoM+ expected |

Unit economics | Not yet required | LTV:CAC ratio 3x+ | Payback under 12 months |

Customer validation | 10–50 engaged users | 20–100 paying customers | 200+ paying customers |

TAM requirement | $500M+ (lower threshold) | $1B+ (standard threshold) | $2B+ (high-growth threshold) |

Team requirement | 1-2 founders, domain expertise | 2-3 co-founders, proven operator at least one | Full leadership team (CEO, COO, VP Engineering, VP Sales) |

Never approach Series A investors with seed-stage metrics. If you raise seed with $5K MRR and stay at that level, you're not ready for Series A. You must demonstrate clear momentum, typically $25K-$50K MRR, before graduating to the next stage.

Geographic and sector variations in VC expectations

Not all VCs evaluate companies the same way. Industry and geography create variance in what's considered "good" metrics and how investors assess startups across different markets.

SaaS founders are evaluated on CAC, LTV, and NRR because recurring revenue is predictable.

Enterprise SaaS VCs expect longer sales cycles (3-9 months) and lower churn.

Horizontal SaaS (tools serving all industries) must show faster adoption and higher expansion revenue to compensate for dilute focus.

Marketplace founders are evaluated on gross merchandise volume (GMV), take rate, and supply-demand balance. VCs know that a chicken-and-egg problem makes marketplaces slow to scale, so they accept lower early revenue if supply and demand metrics are healthy.

Hardware founders face the highest capital requirements and longest time to revenue. VCs expect detailed unit economics, manufacturing timelines, and clear go-to-market channels. Hardware VCs also want to see founder experience scaling manufacturing, this is not the place to learn on the job.

Biotech and DeepTech founders are evaluated on IP moats, team scientific credibility, and regulatory pathway clarity. Revenue comes later; these investors fund moonshots with long timelines. They want to see publication track records, patent portfolios, and strategic partnerships with credible institutions.

Geographically, US VCs expect larger exits ($100M+) because they're writing bigger checks.

European VCs accept smaller exit targets ($30-50M) and focus more on unit economics and profitability.

Asian VCs evaluate market timing and competitive density heavily because tech markets move faster.

We advised a European hardware founder whose product was technically superior to competitors but whose team narrative was weak. The founding team had zero hardware scaling experience. By repositioning around strategic EMEA distribution partnerships they'd already built and bringing in an operations co-founder with manufacturing experience, investor perception shifted dramatically.

Three VCs moved to term sheet within six weeks. Market timing didn't change, the product didn't improve. The team story did.

The lesson: research the investor's thesis and geographic focus before pitching. A founder using US metrics to pitch a European fund with tech-for-good expectations won't land the meeting.

Building a pitch that aligns with VC evaluation criteria

Now that you understand what VCs evaluate, here's how to structure your pitch to address each pillar systematically. Your pitch deck should move through these sections in this order:

The problem: Introduce the founder story and why you're uniquely positioned to solve this problem. This addresses team.

The market: Show TAM, your serviceable market, and why it's growing. Bottom-up validation matters more than top-down estimates.

The solution: Describe your product and differentiation. Focus on customer validation and early metrics, not technical features.

The traction: Show revenue, growth rate, retention, and whatever metric proves product-market fit. Be honest about stage-appropriate metrics.

The ask: Specify how much you're raising and how it advances a clear milestone (e.g., "This capital gets us to $100K MRR and Series A readiness").

The team: End strong with founder and team bios, emphasizing relevant experience and complementary skills.

This structure addresses all four pillars sequentially. Many founders reverse this order, starting with product and ending with a weak team slide. That's the inverse of how VCs weight evaluation.

If you're preparing your pitch materials, a targeted pitch deck review can pinpoint which pillar needs sharpening before investor conversations begin.

Key investor expectations in 2026 and beyond

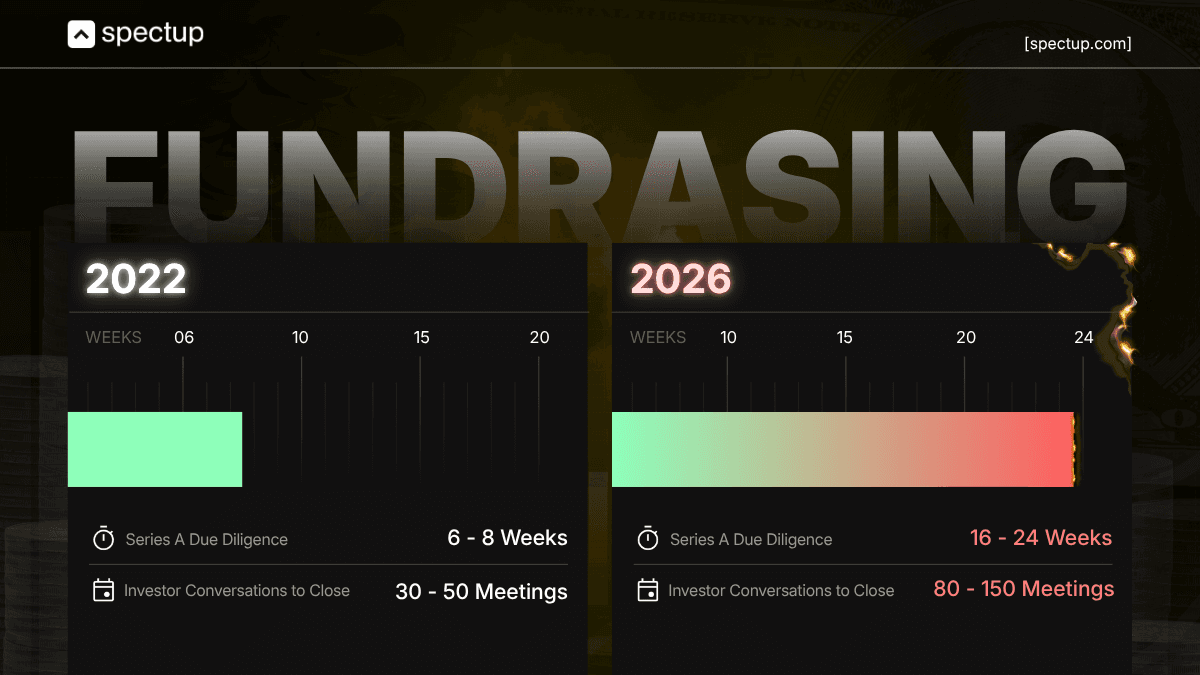

The fundraising landscape in 2026 is tighter than 2023-2024. 80% of venture capital is now concentrated in AI-related companies. This means non-AI founders face higher competitive density and harder questions on team quality, unit economics, and defensibility.

Recent analysis from TechCrunch on the rising Series A bar confirms that bar expectations are increasing across stages.

What's changed in 2026:

Founder quality scrutiny is higher.

With less capital available, VCs invest in lower-risk founders, those with prior exits, operator track records, or domain expertise. New founders without these signals face longer fundraising timelines.

Metrics must be auditable.

VCs have been burned by founders massaging numbers in 2023-2024. Today, revenue must be documented through contracts and cash received. Growth rates must be conservative and repeatable.

Market timing alignment is more important.

VCs are more skeptical of "market inflection" stories. You need to show that the inflection is happening now, not in 2-3 years. Evidence from customer conversations, market data, and competitive moves all matter.

Path to profitability matters.

Even venture-scale companies are expected to show a clear path to sustainable unit economics within the funding horizon. Infinite burn rates are no longer accepted.

For founders navigating this market, the advantage goes to those who understand what VCs evaluate and align their materials accordingly. You can't change your product overnight or rewrite your market.

But you can change how you frame your team strength, validate your market systematically, and report metrics that build credibility.

For specific timeline and tactical guidance, Mark Suster's VC due diligence checklist is still essential reading.

Understanding what VCs look for isn't about gaming the system. It's about meeting investors where they are and giving them the information they need to make confident decisions. The best founders know the four pillars, they know their stage-specific expectations, and they present their company through that lens.

At spectup, we help founders translate this framework into positioning that resonates with investors.

My direct assessment: what the best-funded founders do differently

After working with hundreds of founders, I've noticed something most startup advice misses: the fastest capital raisers aren't always those with the best products or biggest markets. They understand what investors evaluate and present their company accordingly.

The best-funded founders spend as much energy on clarity and positioning as they do on building. They don't hide metrics; they contextualize them. They recognize that every stage requires a different conversation.

The competitive advantage isn't knowledge, it's execution. The founders closing rounds today translate these principles into practice, methodically building materials that meet investors where they are.

How spectup helps

One founder we worked with had every mechanical checkbox filled: right TAM, right metrics, right structure. Investors still passed.

When we repositioned around her team's deep EMEA market experience and customer relationships she'd built across three countries, three VCs moved to term sheet within six weeks. The company didn't change. The frame did.

That's what we do. We take the four-pillar framework from this post and translate it into your positioning strategy. Your pitch materials get audited against what VCs systematically evaluate:

Where is your team story strongest

Which metrics prove stage-readiness

Where does your market positioning create defensibility.

We stress-test all of this against investor decision criteria before you walk into rooms.

We've guided dozens of founders through capital raises totaling $120M+. The pattern is consistent: founders who align their positioning to VC evaluation frameworks close 30-40% faster with better terms. Whether you're preparing for seed, Series A, or Series B, fundraising consulting helps translate these principles into positioning strategy, stress-testing your materials against investor decision criteria before you walk into rooms.

Why founders who prepare close rounds faster?

The difference between founders who close rounds in 90 days and those who take 18 months isn't luck. It's one thing: they know what VCs are evaluating before they walk into the room.

Most founders think preparation means perfecting their product. It doesn't. It means understanding investor evaluation criteria and aligning your story to it.

From working with 150+ founders, here's what separates the fastest closers: they build their pitch around the four pillars systematically, not around what they think sounds impressive. They know their stage-specific benchmarks cold.

They validate market size bottom-up before first meetings. They clean their cap table before pitching. They anticipate due diligence questions and have answers ready.

Most founders think they don't need this framework until they're already in the room with a VC. By then, it's too late.

The real advantage builds in the 60 days before your first pitch. That's when you audit your team story, benchmark your metrics against expectations, and identify which of the four pillars needs reinforcement. That's when you reduce the noise and let investors see what actually matters.

Concise Recap: Key Insights

Team quality outweighs product in early stages

VCs invest in people first because exceptional founders adapt when assumptions change. Domain expertise, execution track record, and cofounder fit are evaluated more heavily at seed than traction metrics.

Know your stage-specific benchmarks before pitching

Seed requires user growth signals and retention metrics. Series A expects $10K-$50K MRR with 3x LTV:CAC ratio and predictable acquisition. Series B demands $100K+ MRR with payback under 12 months and sustainable unit economics. Wrong metrics signal inexperience.

Validate market size bottom-up, not just top-down

TAM must be $1B+ but VCs verify through customer conversations, not just analyst reports. Clean cap tables and honest metrics build investor confidence faster than any pitch deck.

Frequently Asked Questions

What is the most important factor venture capitalists look for?

Team quality consistently ranks as the #1 factor VCs evaluate because strong founding teams with domain expertise and a track record of execution outperform better-funded teams with weaker founders. VCs know founders adapt and pivot; a weak team with a great product rarely scales to exit. Execution ability, resilience under pressure, and the power to recruit top talent matter more than day-one product perfection.