Table of Content

Summary

Secondaries are the third exit channel now

2025 volume hit $233-240B, up 48-53% year on year. The private equity secondary market is no longer a backup. It is a planned route.

[01]

LP-led and GP-led split the market roughly in half

LP-led ran $117B, GP-led $115-116B. Continuation vehicles drove 89% of GP-led activity. Different initiator, different conflict surface, different price.

[02]

Discount to NAV depends on deal type

Top-quartile buyout pools clear at 92-94% of NAV. Venture and tail-end pools clear at 20-35% off. Single-asset CVs cluster near 99.5%.

[03]

In a CV, the binding economic is the reset

The headline price gets the press. The new carry, new hurdle, and cost-bearing rules decide who actually wins. LPs who only read the cover lose ground.

[04]

Selling is rarely about distress

Pension funds, insurance balance sheets, and family offices use secondaries to rebalance. Most of the 2025 LP-led volume is portfolio management, not a fund in trouble.

[05]

The private equity secondary market closed 2025 at roughly $240B, up 48% year on year, according to the Jefferies 2025 Global Secondary Market Review. GP-led volume was $115B, almost exactly half of the total. Continuation vehicles drove 89% of that GP-led number.

None of that is a footnote anymore.

I run this from the inside. At spectup we've placed LP-secondary interests and structured continuation funds for European mid-market GPs. I also see the buy-side flow as a venture scout for Flashpoint, which runs a late-stage secondary fund alongside its primary vehicles.

The pattern I want to put on the page is the one that the explainer articles keep skipping:

How different deal types in the secondary market for private equity actually clear

Where the discount really sits

Which line in a continuation-vehicle term sheet decides who wins.

This piece is for LPs deciding whether to sell or roll, GPs weighing a CV process versus holding to exit, and CFOs at portfolio companies watching the cap table change around them. It's long because pricing in the secondary market for private equity changes by deal type, by vintage, and by which side of the table you sit on.

The short answer: the market doubled; the diligence didn't.

What is the private equity secondary market?

Strip out the jargon and you're left with one idea: someone wants out of a PE position before the fund ends, and someone else is willing to step in. The secondary market for private equity is where existing positions in PE funds and PE-owned assets change hands before the fund reaches its natural end of life.

So when someone asks what secondary private equity is in one sentence: it's the trade of an existing LP interest or sponsor-owned asset before the fund's natural end of life. A pension fund sells a fund interest to free up capital. A buyout sponsor moves a portfolio company into a new vehicle so it can hold it longer.

A venture LP cashes out of a 2017 vintage at a discount. Same plumbing, three flavours.

The three buckets you should keep in mind:

LP-led secondary transaction.

An existing limited partner sells its interest in one or more funds, the textbook lp-led secondary transaction. The GP consents, and that's usually it.

Mechanics: tender, auction, or bilateral sale to a secondary fund.

GP-led secondary transaction.

The sponsor initiates the deal, a gp-led secondary transaction, most commonly a continuation vehicle that buys one or more assets out of the existing fund, with new LPs writing the cheque and existing LPs offered a cash-or-roll election.

Other GP-led shapes: tender offers, strip sales, stapled deals.

Direct secondaries.

A direct stake in a portfolio company, usually a venture, changes hands between holders. Mostly common in late-stage ventures; less common in classical buyouts.

The secondary market private equity investors' track has scaled fast.

According to the Lazard 2025 Secondary Market Report, the secondary market grew 53% in 2025 to $233B, with LP-led at $117B and GP-led at $116B. That's bigger than the global IPO market in most quarters and trending toward $250-300B in 2026.

For the founder or CFO reading this from the operating side: secondary private equity isn't just a fund manager's concern. If your cap table includes a PE sponsor whose fund is past year seven, you're likely living inside a future secondary, whether it gets called LP-led or GP-led. For founders eyeing public-market liquidity in parallel, the same dynamics shape the startup exit menu now in front of growth-stage boards.

The acronyms, before we go further

Half the disagreements I see on secondary deals start with two people using NAV, CV, and tender to mean different things. So here's the gloss before we go further.

Term | What it means |

|---|---|

NAV | Net asset value. The reported mark of a fund or asset, usually struck quarterly and lagging public comps. |

Discount to NAV | The gap between the cleared secondary price and the most recent NAV mark, quoted as a percentage. |

LP-led | A secondary transaction initiated by an existing limited partner selling its fund interest. |

GP-led | A secondary transaction initiated by the sponsor, usually to extend hold on existing assets. |

Continuation vehicle (CV) | A new fund that buys one or more assets from an existing fund, with new LPs and a cash-or-roll election for the old ones. |

Single-asset CV (SACV) | A continuation vehicle holding one trophy asset, sized large. |

Multi-asset CV | A continuation vehicle holding a basket of two to five assets from the original fund. |

Strip sale | The sponsor sells a slice across multiple portfolio companies, cash distributed pro-rata to current LPs. |

Tender offer | A GP-facilitated process offering all LPs a single price to sell some or all of their interest. |

Stapled transaction | A secondary purchase tied to a fresh primary commitment in the GP's next fund. |

LPAC | Limited Partner Advisory Committee. The LP consent body inside a fund that votes on conflicts. |

Fairness opinion | Independent valuation review used to validate the CV price and demonstrate process. |

If you're reading this from the LP side, the two terms that matter most are 'reset hurdle' and 'cost-bearing'. Hold them. We'll come back to them.

LP secondaries: who sells, who buys, and why do discounts widen?

An LP-led secondary transaction is mostly a portfolio decision, not a fund-quality decision. A pension fund hits its private markets allocation ceiling. Most LP-led volume in the secondary market for private equity is rebalancing, not panic.

An insurance balance sheet runs into a Solvency II treatment shift. The line item moves before the fund does.

A family office wants cash for next-fund commitments. None of that's distress. It's the denominator effect doing its quiet work on every institutional book.

Why do investors care about LP-led discounts? Because the discount is now mostly a markdown calibration, not a credit signal.

The reported NAV from the GP lagged the public comps by one or two quarters. The secondary buyer needs a cushion for that lag plus the J-curve cost plus illiquidity. The math then varies wildly by strategy and vintage.

Here is what I see clearing in 2025 and early 2026 across the LP-led market. The numbers are consistent with the Jefferies and Lazard reviews and with what I observe on the buy-side through Flashpoint.

Strategy | Vintage tier | Discount to NAV (typical clearing range) |

|---|---|---|

Buyout (top-quartile) | 2019-2022 | 6-8% off (cleared 92-94% of NAV) |

Buyout (broad market) | 2017-2021 | 10-15% off |

Growth equity | 2018-2022 | 15-25% off |

Venture | 2017-2021 | 20-35% off |

Tail-end (vintage >10 years) | 2010-2015 | 25-45% off |

The top of that table, the headline discount to nav private equity secondaries chart everyone quotes, looks tight to anyone reading the LP press.

According to Hamilton Lane's secondary market work, around two-thirds of secondary returns historically come from post-purchase appreciation, not the discount captured at entry.

So the entry price was never the whole story. It still isn't.

What the LP press gets wrong about the discount?

I sat across from a Munich family office on a rainy Thursday a few months ago, term sheets on the conference table. They wanted to sell a position in a 2018-vintage European buyout fund. NAV around €11M.

Their first instinct was to anchor on the 15% discount they'd read about for buyout secondaries broadly. The actual clearing print was a discount under 7%, because the fund was top-quartile and the assets were food-and-beverage cash flow with stable EBITDA marks.

The discount narrowed against expectation. They were ready to leave money on the table because the press they'd absorbed described a different market than the one they were actually in.

The reason discounts widen is rarely about how good the fund is. It's about how much mark-drift the buyer has to absorb and how thin the buyer pool is for that strategy. Buyout is deep, tail-end venture isn't.

The buy-side of the private equity secondary market has gotten institutional. Ardian closed a €30B 9th secondaries fund in January 2025, the largest of the dedicated secondary funds private equity has produced.

That kind of dry powder compresses LP-led discounts on quality assets. It also widens the spread between the top quartile and the rest, because the new money is selective. The structural inflow of private equity secondary investments from insurance, sovereign, and pension capital has changed how the top of the LP-led market clears.

If you're an LP weighing a sale:

Read your most recent NAV mark

Run a backtest against listed comps

Stop quoting "the discount" as a single number.

There isn't one. There's a discount for your fund, your strategy, your vintage.

GP secondaries: continuation vehicles, strip sales, and the new normal exit

A GP-led secondary transaction now drives nearly half the market. GP-led activity reached $115-116B in 2025, just under half of all secondary market private equity activity. Sponsors aren't reaching for this as a workaround anymore.

Most of the GP-led print is a continuation vehicle private equity sponsors treat as a default tool, with the LPAC bringing the friction the regulator used to.

Continuation vehicles drove 89% of that according to Jefferies, with an average CV size of around $900M and 29 transactions north of $1B. Per Bain's 2026 Global Private Equity Report, GP-led CV activity has grown at a 37% compound rate since 2022.

The simple explanation: M&A windows opened and closed three times in 2023-2025, IPOs were thin, and the sponsor sitting on a quality asset at year 5 of a 10-year fund had two choices. Force a sub-optimal exit and disappoint LPs on multiple occasions. Or build a continuation vehicle, get the seller LPs cash, get the rollover LPs more time, and keep the asset working.

The four GP-led shapes you need to keep straight:

Structure | What transfers | LP election | Typical size | Pricing reference |

|---|---|---|---|---|

Full CV | Entire portfolio of an old fund into a new vehicle | Cash or roll, on all assets | $500M-$3B | Aggregate fund NAV, basket discount |

Single-asset CV (SACV) | One trophy asset, sponsor stays as GP | Cash or roll, on the single asset | $300M-$5.6B | Reference transaction or DCF cross-check |

Multi-asset CV | 2-5 selected assets, the others stay in the old fund | Cash or roll, on the selected basket | $500M-$2B | Asset-by-asset mark; modest discount |

Strip sale | A pro-rata slice across multiple companies | Pro-rata cash, no roll choice | $200M-$1B | Each asset's mark, basket discount |

Named deals worth pinning. Vista Equity Partners ran a $5.6B single-asset continuation fund for Cloud Software Group in 2025, the largest SACV by total transaction size on record. That single-asset continuation fund cleared at a roughly 99% mark, with a reset 7% pref and a 25% catch-up.

Leonard Green ran a twin-CV process across five assets the same year. Insight Partners closed a ~$1.5B multi-asset CV in 2024. Dechert reports that 46% of GPs are now using GP-led tools to manage the fundraising environment, roughly double the prior-year share.

How GPs actually pick a structure (a real 2025 example)

I worked with a European mid-market buyout sponsor on a CV question in 2025, sketching options on a whiteboard in their Frankfurt office. They had a portfolio company they wanted to hold three more years, mostly because the founder-CEO had a clear platform-acquisition plan running into 2027.

The sponsor's first instinct was a full CV. We pushed back. The right structure was a single-asset CV, because the rest of the portfolio was at or near natural exit anyway, and the LPs in the old fund had a different appetite to roll.

A full CV would've forced an all-or-nothing election across mixed assets. A single-asset CV let each LP make a clean call on the one company they actually had a view on.

The structure follows the LP election you can defend, not the structure that looks tidy on paper.

The new normal also has a Bain footnote that matters. Per their report, LPs tolerate roughly one CV per year per GP.

Two in a year and the conversation stops being about deal mechanics and starts being about whether the GP is structurally unable to exit. Once the LPAC pings on that, the next primary fund gets harder. The GPs that get sloppy here usually don't notice until they're 14 months into a fundraise that should've closed in eight.

How a continuation vehicle actually gets priced

Most LPs I sit with read the cleared CV price and stop. That's the mistake the private equity secondary market explainer pages keep encouraging.

If you've ever asked what a secondary transaction private equity actually clears at, the honest answer is not at one number. The price of a continuation vehicle isn't a single number. It's a stack of decisions where each one moves both the headline and the binding economics.

The waterfall, step by step, in the deals I've seen up close:

Starting NAV mark. The most recent reported NAV from the GP. This anchors the conversation.

Independent fairness opinion. A third-party valuation firm validates the mark, usually with a DCF cross-check and a public-company sanity check. The opinion is now market-standard even with the SEC adviser-led rule vacated.

Reference transaction or pricing range. The GP commissions an indicative bid round from 4-8 secondary buyers, anchored on the NAV mark.

Auction or pre-emption. A lead buyer either pre-empts the process at a stated price or wins a narrow auction. Single-asset CVs often pre-empt; multi-asset CVs auction harder.

LPAC consent. The fund's LP advisory committee reviews the conflict and signs off on terms, fee structure, and cost-bearing.

LP election window. Existing LPs choose one of the following: take cash at the cleared price or roll it into the new vehicle. The election window is usually 20-30 business days.

Closing and rebalancing. Sellers receive cash; rollers move into the new vehicle with reset economics.

The headline result: per HarbourVest's analysis, median single-asset CV pricing has clustered around 99.5% of NAV between Q4 2022 and Q2 2025. Practically zero discount on the trophy asset.

But the cleared price is only half of the economics. The reset is the other half.

When an LP rolls into a CV, the new vehicle resets the carry waterfall (usually 20% over an 8% preferred return), resets the cost-bearing for the new fund's expenses, and often imposes a hard cap on how much of the original interest can roll.

From my LP-side work, the LPs who only read the headline 99.5% of NAV print and ignored the reset terms ended up materially worse off than the LPs who took cash and redeployed.

In a continuation vehicle, what gets priced is the asset. What gets reset is the LP's economics. Most LPs only read one of those two documents.

The CFA Institute's 2025 report on continuation funds documents the fiduciary tension precisely: the GP sits on both sides of the trade. Without a hard fairness process and an active LPAC, the CV becomes a fundraise extension dressed as a liquidity solution. That's a structural problem, not a moral one, and pretending otherwise is how LPs get rolled.

What is a stapled secondary, and why sponsors love them

A stapled secondary is a continuation vehicle (or LP buyout) where the secondary buyer commits to a fresh primary check in the GP's next fund. The two pieces are stapled together. It's one of the most negotiated structures in the secondary market private equity dealmakers see today.

Same buyer takes out the old LPs and writes a primary into the new vehicle.

From the GP's perspective the math is excellent. A staple turns a liquidity event into a guaranteed primary commitment.

In a market where new primary fundraises take 18-24 months and 30-40% of GPs miss their target, a $300M staple is the cheapest dollar a sponsor can raise. The secondary side functions as a sweetener for the primary.

From the LP's side, the conflict is structural. The GP wants the primary, so the GP is incentivised to give the secondary buyer terms that favor the buyer at the expense of the rolling LPs.

ILPA's guidance on this is clear. Per the ILPA continuation funds guidance, GPs should treat themselves as fiduciaries on both sides of the trade, with full LPAC consent and independent fairness work.

After the Fifth Circuit vacated the SEC's adviser-led rule in June 2024, the formal regulatory requirement disappeared. The market practice hasn't. Williams Marston has documented that fairness opinions remain the default even without the rule.

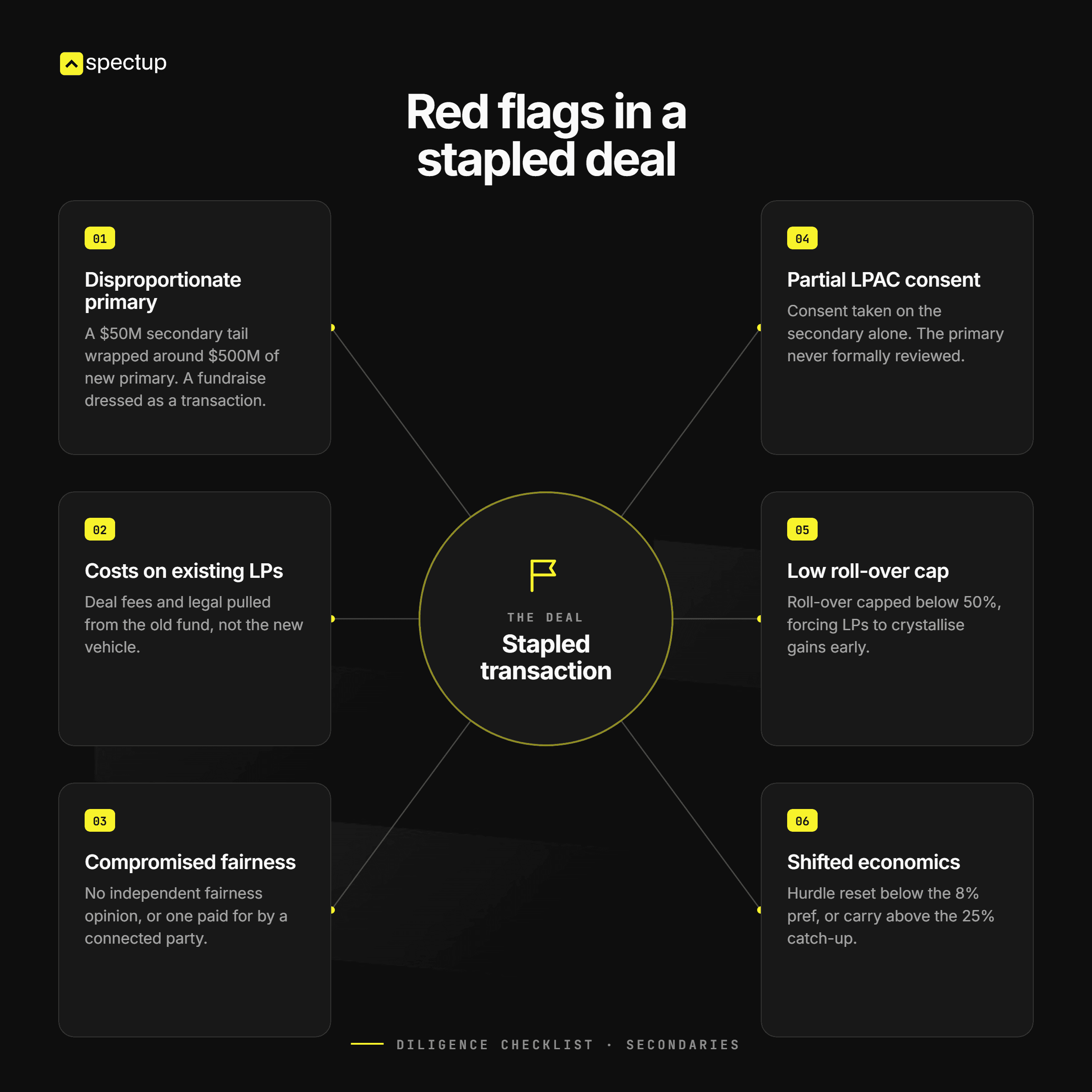

Red flags in a stapled deal, in the order they actually matter:

Primary commitment size out of proportion to the secondary purchase (a tail of $50M of secondaries with $500M of new primary is a fundraise dressed as a transaction).

Cost-bearing skewed to existing LPs (transaction fees and legal pulled from the old fund, not the new vehicle).

No independent fairness opinion or a fairness opinion paid for by a connected party.

LPAC consent obtained on the secondary alone, with the primary not formally reviewed.

Roll-over cap below 50% (forces existing LPs to crystallise gains they would have preferred to defer).

Reset the hurdle below the standard 8% pref or carry above the 25% catch-up.

None of those are theoretical. We've walked LPs through deals with two or three of these red flags inside a single staple. The right answer is sometimes still to roll, but it should be the LP's eyes-open call, not the path of least resistance.

Tender offers and strip sales: the per-LP liquidity play

Tender offers and strip sales are the under-discussed end of the GP-led market and the most overlooked corner of the secondary market for private equity. Both are still GP-led, but neither moves an asset into a new vehicle. They are pure liquidity plays for current LPs.

A tender offer is a GP-facilitated process where a single secondary buyer or pool of buyers offers a single price to all LPs. Each LP elects how much of its interest to sell. Per Private Equity International, tenders have become an industry staple, especially in venture and growth where individual LP positions are smaller and the LP base is more diffuse.

A strip sale is different. The GP sells a pro-rata slice across multiple portfolio companies to a secondary buyer. The cash gets distributed to current LPs pro-rata, with no choice on which assets.

Strip sales are the mid-life recap of the buyout world. The sponsor returns capital, the asset stays in the fund, and the secondary buyer gets diversified exposure across a known portfolio.

The key contrast:

Mechanic | Tender offer | Strip sale |

|---|---|---|

Initiator | GP, on LP request or fundraise prep | GP, mid-life |

What transfers | Selected LP interests in the fund | Slice of selected portfolio companies |

LP election | Each LP chooses how much to sell | None; cash distributed pro-rata |

Common use case | Venture/growth fund liquidity | Buyout mid-life recap |

Pricing reference | Single price across all LPs | Asset-by-asset NAV, basket discount |

I posted on X recently about how late-stage liquidity is migrating away from the traditional IPO window. The same logic applies to mid-life private positions and to the rest of the private equity secondary market.

A tender or a strip sale gives a GP a way to distribute capital without forcing an exit on assets that are still compounding. The market has built tools for this. It hasn't built much patience for explaining them.

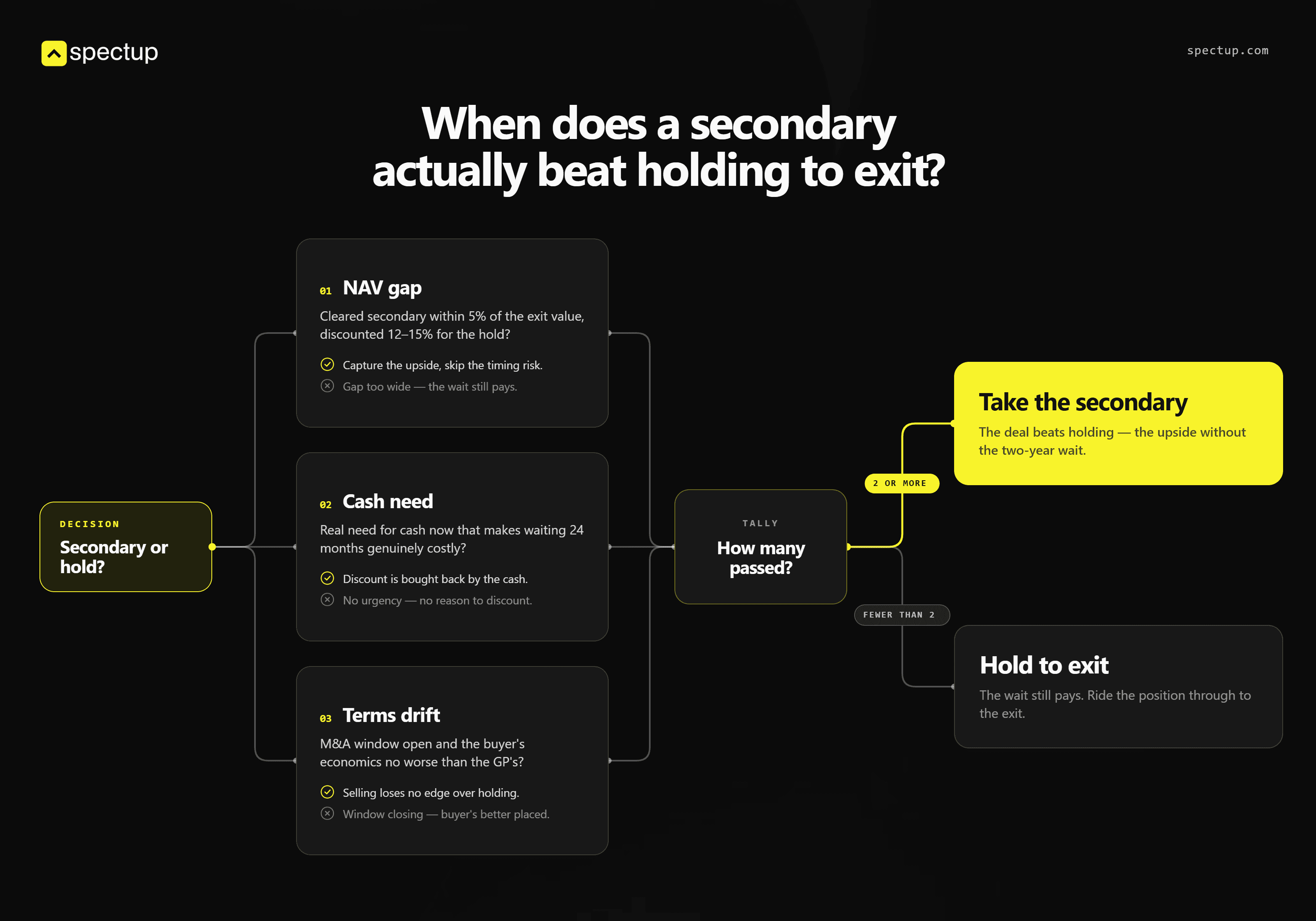

When does a secondary actually beat holding to exit?

Nine times out of ten, a GP or LP shows up with a continuation vehicle proposal or a tender and asks the wrong question. The real one isn't "should I do this deal?" It's "does this beat holding for 24 more months and running a natural process?"

That's the question the secondary market private equity explainer pages never answer. I run what I call the NAV-Cash-Terms check. Three filters.

If two or more pass, the deal usually beats holding. If fewer than two pass, hold. That's the practical filter we run on every private equity secondary market mandate that comes through the door.

NAV gap.

Is the cleared secondary price within 5% of the GP's expected exit price discounted at 12-15% for the holding period?

If yes, the secondary captures most of the upside without the timing risk.

Cash need.

Does the LP or GP need cash now for a specific purpose (unfunded commitments, denominator rebalancing, new primary cheque, founder estate planning) where 24 months of waiting actually has a real cost?

If yes, the discount is partly bought back by the value of the cash.

Terms drift.

Is the M&A window for the asset's sector still open, and is the secondary buyer's role-economic at least no worse than the GP's expected economics over the next two years?

If yes, holding gives no advantage. If no, the secondary buyer's structurally better positioned than the seller.

The Bain 2026 outlook frames this from the other side. Around 25% of GPs have run a CV recently and around 40% expect to in the next one to two years.

According to White & Case, CVs already account for around 19% of sponsor-backed exit volume. Add the LP-led market on top, and the secondary route covers a meaningful slice of every private equity exit channel.

Two patterns worth naming. In a venture, the secondary almost always beats holding once an asset has crossed its inflection.

Bolt was repriced to roughly $2B via secondaries off an $11B peak in a market where insiders were selling and outsiders were buying. Canva ran a $26B secondary in 2024 because the IPO window was closed and high-quality late-stage demand was sitting on the sidelines.

In buyout, the call is closer. M&A still beats secondaries when the window is open and the asset has a strategic acquirer in view.

Where is the secondary market for private equity heading next?

Three forces are about to reshape this market, and most LPs aren't priced for any of them yet. Three threads to watch in 2026.

Volume. Lazard and Jefferies both project $250-300B in 2026 if M&A windows stay narrow. If a primary fundraise market opens up, GP-led volume may compress as fewer GPs need CVs to bridge funding gaps.

If M&A stays slow, GP-led continues to compound. Either way, LP-led is structural now and isn't going back down.

Structure. Credit and infrastructure secondaries are scaling fast. Semi-liquid and evergreen vehicles are increasing buy-side competition for secondary funds private equity LPs allocate to, which compresses discounts on the high-quality LP-led pools and creates a sharper spread between top-quartile and the rest.

Private equity secondary investments are also showing up inside semi-liquid retail wrappers.

Single-asset CVs will continue to be the dominant trophy-asset structure; expect more first-time CVs from European mid-market sponsors as the playbook becomes routine.

Risk. The more capital chases secondaries, the more secondaries become a fundraise-extension product rather than a true liquidity solution.

The CAIA Association published a critical piece on whether the CV boom is a structural shift or a liquidity patch. The honest answer is both, depending on whose CV you are looking at.

I wrote on X two weeks ago that the Long Crossover is dead; long live the Vertical IPO, with Cerebras's compressed S-1 to pricing path as the template for late-stage liquidity. The same compression is reshaping how secondaries function.

The line between a Series H, a stapled secondary, a continuation vehicle, and an IPO is now fuzzier than at any point in the last decade. The broader venture capital trends 2025 reporting shows the same compression on the venture side.

My direct read for LPs and GPs sitting on a 2026 secondary decision

If you only take three things from this piece, take these. The private equity secondary market is no longer the back-door route. It is the third real exit, on roughly equal footing with M&A and IPO when measured by sponsor-backed exit volume.

I sat with a Munich LP last quarter who had the cover terms memorised and had not read the new-fund LPA. That's the most common mistake I see right now.

If you can't defend the reset economics of the CV at the LPAC line by line, you don't understand the deal you're rolling into. Cover price is the easy part.

If you're an LP, the deal that matters isn't the one with the smallest discount to NAV.

It's the one where the reset economics inside the continuation vehicle leave you better off than taking cash and redeploying.

Different fund, different answer. Read both documents, not one.

If you're a GP, the constraint isn't pricing. It's a sequence. LPs tolerate one CV a year.

Two and the next primary gets hard. Pick the structure that lets each LP make a clean election on the asset they actually have a view on.

And don't staple a primary onto a secondary unless you can defend the conflict line-by-line at the LPAC.

Where spectup fits on LP secondaries and continuation funds

I've placed private placement agent mandates inside the private equity secondary market for LP secondaries and structured continuation vehicles for European mid-market GPs. The pattern that keeps showing up: the LPs who read the reset terms in addition to the price end up materially ahead of the LPs who only signed the cover. The GPs who can defend their CV structure at the LPAC raise their next primary on time; the ones who can't don't.

If you're a GP weighing a CV process or an LP staring at a tender election, the work is brief and structural. We've done both sides.

We can help on fundraising consultant mandates that include CV structuring, and we can model the roll-versus-cash math for individual LPs in advance of an election deadline. That's exactly the kind of work spectup runs on every continuation vehicle mandate, and we're happy to be a second pair of eyes on a term sheet before the LP election window closes.

What I would tell you if you asked me directly

Most people writing about secondary private equity right now treat the volume number as the whole story. It isn't.

The interesting question for 2026 isn't whether the market keeps growing. It's whether the new capital flowing into secondaries is doing the work it advertises.

Some of it is. A lot of it is buying yesterday's risk at today's NAV.

I would push back on one piece of conventional wisdom about secondary funds private equity LPs now back at scale: the idea that GP-led secondaries are now a "mature" product. They aren't. Most private equity secondary investments today still buy yesterday's risk at today's NAV, and the second-largest secondary funds private equity has ever raised closed in the same 18 months.

They are a five-year-old product that scaled faster than the diligence process around it. The LPACs that are doing real work right now are rare. The fairness opinions that actually change a price are rarer.

The default is still rubber-stamp.

If you're sitting on an LP advisory committee in 2026, your job is harder than the job description suggests.

You're the only adult in the room who can say no to a CV that doesn't deserve to clear.

And if you're a GP, don't confuse the speed at which a CV closes with whether it should have been done.

Some of the CVs that closed in 2025 will look indefensible in 2028.

The market doubled. The diligence didn't. Decide which side of that sentence you want to be on, and price your next deal accordingly.

Concise Recap: Key Insights

Secondaries are now a primary exit channel

2025 volume hit $233-240B and GP-led accounts for nearly half. The secondary market is no longer a backup route; it is the third real exit.

Discount to NAV depends on deal type, not market mood

Top-quartile buyout clears at 92-94% of NAV. Venture and tail-end pools clear at 20-35% off. Single-asset CVs cluster near 99.5%.

In a stapled CV, watch the next-fund commitment

The conflict sits in the primary, not the secondary. Roll-over caps, cost-bearing, and reset hurdles decide who actually wins inside a continuation vehicle.

Frequently Asked Questions

What is a secondary in private equity?

A secondary in private equity is the sale of an existing fund position or asset before the fund's natural end of life. The two main flavors are LP-led (an existing LP sells its fund interest) and GP-led (a sponsor moves portfolio companies into a new vehicle and gives existing LPs a choice to sell or roll). Price is usually quoted as a percentage of net asset value