Table of Content

Summary

CVC invests for strategic goals, not just returns

Corporations deploy capital to access new technologies, identify M&A targets, and build partnerships. This dual mandate reshapes how founders should approach CVC funding.

[01]

2026 CVC trends are shifting capital allocation

Fewer, larger checks. AI-powered diligence cutting evaluation time by 60-70%. ESG/climate focus concentrating 35% of 2026 deals. Geographic expansion moving capital to non-US markets.

[02]

CVC failure rates exceed traditional venture capital

80% of CVC portfolios fail, driven by strategic misalignment and founder-corporate tension. Founders must understand these risks before pursuing corporate backing.

[03]

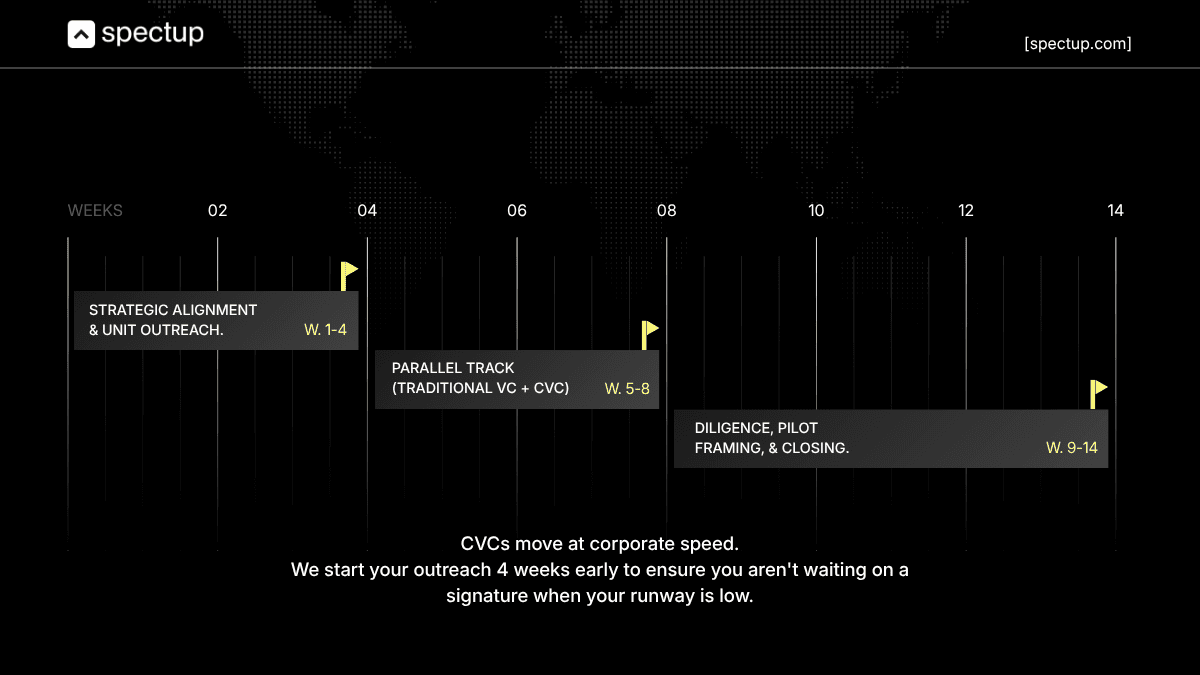

Deal cycles take 18-24 months, not 6-12

CVC closes are slow. Multiple stakeholder approvals, board reviews, and governance checks extend timelines. Founders need runway cushion and patience.

[04]

Not every startup should pursue CVC funding

CVC works best for B2B companies needing corporate distribution, technology integration, or partnership pathways. Consumer and independent models may face pressure toward unwanted exits.

[05]

What is corporate venture capital? Corporate venture capital is reshaping how founders access growth capital.

In 2025, 22% of all venture capital globally flowed through corporate venture arms (NVCA, 2025): up from 15% just three years ago. By 2026, projected CVC deployment exceeds $28 billion. These aren't minor players anymore.

When Intel Capital, Google, Salesforce, and BMW write venture checks, they're rewriting the rules for startups at every stage.

But here's what most founders get wrong: corporate venture capital isn't just venture capital with a corporate name tag. Corporate venture capital companies operate by different rules, with different incentives, and vastly different outcomes than traditional VC. When evaluating corporate venture capital companies, you need to understand that they invest alongside traditional venture funds, but their behavior diverges sharply when strategic alignment conflicts with financial returns.

According to spectup cuts through the framework-heavy content and gives you what you actually need to decide whether corporate backing is a help or a trap.

The stakes are significant. A CVC investment can accelerate your company by 3-5 years through operational resources, customer access, and partnership advantages that traditional VCs simply can't provide. The same CVC investment can also trap you in a multi-year negotiation with corporate stakeholders, constrain your strategic independence, and create exit pressure toward acquisitions you'd never choose independently.

Founders who manage this terrain successfully gain tremendous value. Those who don't get frustrated, lose institutional confidence, and often see their startups acquired or wound down when corporate strategy shifts.

What is corporate venture capital?

Corporate venture capital companies operate differently than traditional venture funds. Understanding how corporate venture capital companies make decisions is critical to your success.

The short answer is:

CVC (Corporate venture capital) is when a corporation invests its own capital in external startups to achieve both financial returns and strategic objectives.

Understanding what is the main goal of corporate venture capital investments requires recognizing this dual mandate. Unlike a traditional venture capital fund (which exists solely to maximize portfolio returns), a corporate venture capital company fund balances two masters: making money and advancing the parent company's long-term strategy.

This dual mandate changes everything. A traditional VC invests in Stripe because they believe in payment infrastructure.

A CVC from a financial services company invests in Stripe because it wants access to payment technology, potential acquisition targets, and early signals of market shift. The financial upside matters, but strategic fit often wins the tie.

How prevalent are corporate venture capital companies in the market?

77% of Fortune 100 companies now engage in some form of venture investing (CB Insights, 2025), whether through dedicated corporate venture capital company funds, corporate accelerators, or partnership vehicles.

Corporate venture capital company funds like Intel Capital have deployed over $12 billion into 1,500+ portfolio companies. Google Ventures operates separately from Google's broader venture interests.

According to Salesforce Ventures invests across enterprise software, cloud, and AI. These aren't experimental programs anymore, they're core business infrastructure.

What is corporate venture capital and how does it differ from traditional VC?

Most founders ask: what are corporate venture capital companies really looking for? The answer differs sharply from traditional VC.

The key differences between corporate venture capital companies and traditional VC are significant. Three core differences separate corporate venture capital vs venture capital - CVC from traditional VC, and they account for why 80% of founder-CVC relationships fail to deliver the expected strategic value.

Understanding each changes how you pitch, negotiate, and structure your relationship with corporate capital:

Investment incentives shift from purely financial to strategic + financial.

Traditional VCs chase returns. Distributed capital is their job. Corporate VCs chase returns and strategic alignment. They ask:

Does this investment help us access emerging threats?

Can we acquire this team?

Does this expand our customer access?

A traditional VC in 10 companies hopes one hits 100x. A CVC across dozens of companies hopes 2-3 hit 100x and 5-6 create strategic partnerships or lead to acquisition.

Decision speed favors traditional VCs by 6-9 months.

Traditional VC partners vote. If three partners say yes, you're funded. CVC requires sign-off from corporate stakeholders, legal, strategy teams, and sometimes executive leadership.

According to CB Insights and venture capital data from the NVCA, traditional VCs close deals in 6-12 weeks on average. CVCs take 18-24 weeks. That's nearly double the timeline.

Exit expectations diverge sharply.

Traditional VCs want IPO or acquisition at 5-7 year horizons. Corporate venture capital companies are comfortable with 8-10 year horizons, but they prefer acquisition by the parent company or strategic partner companies.

This sounds ideal on the surface (longer runway), but it creates misalignment: founders often want independence, corporate wants integration.

Here's a clearest comparison of how the two investment models differ:

Dimension | Traditional VC | Corporate VC |

|---|---|---|

Primary incentive | Financial returns (multiples) | Strategic alignment + returns |

Typical check size | $500K–$5M | $1M–$10M (growing larger) |

Decision timeline | 6-12 weeks | 18-24 weeks |

Exit preference | IPO or independent acquisition | Acquisition by parent or related companies |

Post-investment involvement | Board seat + quarterly updates | Board seat + deep operational integration |

Failure tolerance | High (expect 70% failure rates) | Low (expect 80%+ failure rates) |

Why corporations invest in venture capital: 5 strategic goals

Why do corporate venture capital companies exist?

Understanding their motivations is critical for founders evaluating this capital. In short, CVC is how large corporations access innovation externally.

Large companies face an existential paradox: they're optimized to execute known business models, not discover new ones. Corporate venture capital companies solve this by deploying capital to external startups.

Venture investing solves this. Five concrete strategic objectives drive deployments by CVC firms:

Technology window creation. Intel invests not to acquire startups but to watch emerging threats and opportunities in chip architecture, AI acceleration, and edge computing.

By holding minority stakes in early-stage companies, Intel gets visibility into technology trajectories 2-3 years before the market settles. It's R&D by observation.M&A target identification with reduced risk. Corporations acquire startups, but acquisition of unproven teams is risky.

CVC investments (typically 10-25% stakes) let corporations de-risk acquisitions:

Prove the team executes

Validate customer demand

Negotiate at a lower valuation when acquisition becomes obvious.

Salesforce uses this playbook relentlessly, invest as CVC, then acquire when strategic fit is proven.

Distribution channel expansion. BMW i Ventures doesn't invest in mobility startups for equity returns. It invests to explore new distribution models, charging infrastructure partnerships, and customer acquisition channels for electric vehicles.

The CVC stake creates alignment on go-to-market strategy.

Market sensing in new verticals. Kaiser Permanente Ventures invests in healthcare startups not because it's running a VC fund, but because it needs to understand digital health, remote care, and consumer wellness trends reshaping healthcare.

Minority stakes in startups give Kaiser board observation rights and early intelligence.

R&D co-development partnerships. Cemex Ventures invests in construction tech, sustainable building materials, and logistics startups. But many deals include equity-for-engineering arrangements:

Cemex engineers work alongside portfolio company engineers to integrate solutions into Cemex's operational platforms.

Equity creates alignment for this collaboration and ensures priority focus on Cemex's specific needs.

This model accelerates product development for startups (access to domain expertise) while accelerating Cemex's innovation cycles (proven solutions faster than internal R&D).

These five goals explain why corporate venture capital funds form and matter to founders and how a corporate venture capital fund operates and how corporate venture capital differs from traditional venture capital.

Traditional VCs invest because they believe in the market and the team.

CVC funds invest because they believe in the technology or market *and* see strategic value for the parent company. This dual incentive structure pervades everything in the relationship: board meetings, term sheet negotiations, portfolio company management, and exit discussions. Founders who understand these motivations can better negotiate terms and set realistic expectations for the partnership.

A practical example: You raise Series A from a traditional VC and a CVC from an industrial automation company. Both wrote $3M checks.

Both want 12-month runway visibility. When your product pivots based on customer feedback, the traditional VC says "Great, listen to customers." The CVC says "How does this align with our automation roadmap?

We need engineering integration on Q3 deliverables." This isn't criticism, it's the CVC doing its job.

But if you weren't expecting this level of operational oversight, you're surprised and frustrated. Founders who anticipate strategic scrutiny handle it successfully.

Key trends shaping corporate venture capital in 2026

The landscape for corporate venture capital companies is shifting rapidly. These trends shape how corporate venture capital companies deploy capital and what they expect from founders.

The CVC landscape is evolving rapidly. Here are four concrete 2026 shifts that reshape how founders should approach corporate capital:

Selective deep dives, not broad exploration. CVCs used to deploy capital widely: small checks ($500K-$2M), many companies (50-100 per fund), low conviction bets on emerging markets. Today's corporate venture capital strategy favors focused deployment with higher conviction bets.

That era is ending. According to PitchBook market data, Corporate venture capital companies are consolidating capital into fewer, larger bets.

The median CVC check size is up 35% year-over-year (PitchBook, 2026). Selectivity is increasing dramatically. This creates a winner-take-most dynamic: if a CVC invests in your sector, they're taking it seriously and will likely double down with follow-on capital.

But if they pass, don't expect follow-on interest. They're placing bigger bets on fewer companies and expect those bets to work harder. For founders, this means CVC interest signals higher conviction, but also higher expectations for capital deployment and strategic impact.

AI-powered diligence is accelerating deal evaluation. Corporate venture capital companies are deploying AI tools to analyze founder backgrounds, market TAM, competitive positioning, financial projections, and team dynamics.

Evaluation speed is improving by 60-70% (reported by CVC early adopters). This cuts deal timelines *slightly* but raises the bar for entry dramatically. Founders with incomplete financial models, unclear market positioning, or unproven unit economics get filtered out faster by algorithms than by humans.

According to NVCA's CVC trends data, 40% of larger CVCs (those managing $500M+ in assets) have implemented AI-assisted diligence. Founders pitching these funds need crystal-clear storytelling, validated assumptions, and financial models that withstand algorithmic scrutiny.

ESG and climate focus concentrating capital. An estimated 35% of 2026 CVC deals target climate tech, sustainability, and ESG-aligned startups, based on sector analysis of major CVC portfolios.

This reflects three forces: regulatory pressure (SEC climate disclosure mandates for corporations), stakeholder expectations (institutional investors pushing for ESG portfolio alignment), and genuine belief that climate-aligned companies will outperform traditional models long-term. If your startup touches sustainability, renewable energy, circular economy, or environmental impact, CVC interest is exceptionally high. CVCs in energy, automotive, construction, and industrial goods are particularly active in this space.

If you're building a B2B SaaS tool with no climate angle, CVC interest is lower unless the tool directly serves climate-aligned companies.

The capital concentration in climate is creating higher valuations for climate startups (analysts cite a 15-20% premium over comparable non-climate deals) and shorter close timelines in some sectors.

Geographic diversification moving capital to non-US markets. US-based CVCs reportedly deployed a growing share of capital internationally in 2025, with estimates suggesting domestic concentration dropped from 80%+ to closer to 60%, a significant shift tracked across major fund portfolios.

European, APAC, and Latin American markets are attracting 20-40% of CVC capital from US corporations. Non-US regions are becoming priority markets. Intel Capital deployed capital to startups in India, Singapore, and Germany.

Google Ventures expanded APAC hiring and investment team presence. Salesforce Ventures opened European offices. This creates genuine opportunity for founders outside Silicon Valley but also increases competition from global startups for the same CVC capital.

Non-US founders shouldn't: corporations are increasingly evaluating talent and markets globally, which can work in your favor (unique market access, local expertise) or against you (competing with global candidates).

The geographic diversification also reflects corporate interest in localized solutions:

European manufacturing demands different innovation than US markets

APAC consumer behaviors vary significantly from Western norms, and Latin American logistics challenges create unique opportunities.

These four 2026 trends reshape the CVC investment landscape for founders. Selectivity increases (fewer CVCs, larger checks, deeper scrutiny).

Technology improves (faster screening, higher bars)

Focus consolidates (climate and sustainability favored, non-aligned sectors disadvantaged)

Geography expands (more opportunities outside US, more global competition).

For founders, this means CVC capital is both easier (if you're in a favored sector) and harder (if you're not) to access in 2026.

You can maximize these trends if you fit the profile.

How CVC firms deploy capital: Structures and deployment models

How corporate venture capital companies operate varies significantly. Corporate venture capital operates through five distinct structural models, each with different governance, capital sources, and implications for founders.

Understanding which structure you're dealing with determines your positioning in negotiations and your likelihood of follow-on capital.

Direct Corporate Investment (100% corporate-owned)

The corporation writes checks directly from corporate funds. Whether it's CVC corporate venture capital deployed through a dedicated subsidiary or direct investment, the corporate controls capital deployment.

Intel Capital and Google Ventures use hybrid models here, technically separate entities but wholly owned by the parent. The corporate balance sheet funds deployments, giving the parent complete control over investment decisions and fund operations. This structure is common in tech, where corporations have sufficient capital reserves.

Advantages of Direct Corporate Investment capital:

Fast decisions

Deep integration with parent company resources

Board-level visibility.

Disadvantage of Direct Corporate Investment:

Portfolio decisions influenced by corporate quarterly earnings pressure

Stock market cycles.

If parent company stock price drops 30%, investment appetite evaporates within weeks, and follow-on rounds disappear.

Founders have experienced this firsthand during 2022-2023 tech slowdown when many corporations froze CVC investments.

Dedicated Corporate Venture Capital Fund - CVC Subsidiary (independent governance)

Salesforce created Salesforce Ventures as a legally separate entity with its own board, CFO, and investment thesis.

The parent company commits capital to the corporate venture capital fund but operations are autonomous. This structure is gaining popularity because it insulates the CVC from quarterly earnings pressure while maintaining parent company strategic influence.

Advantage of Dedicated Corporate Venture Capital Fund:

More founder-friendly decision-making

Independent fund management team

Strategic control without quarterly volatility.

Disadvantage of Dedicated Corporate Venture Capital Fund:

slower capital deployment due to governance overhead, weaker access to parent company operational resources. Some founders prefer this structure because the CVC fund doesn't face immediate pressure to cut portfolio companies when parent company stock declines.

Strategic partnerships with lead VCs (capital + strategy)

CVCs co-invest alongside traditional VC lead investors in specific rounds or syndicates.

Corporate venture capital company checks are typically smaller (20-40% of round) but come with strategic value: board relationships, customer access, integration opportunities, and corporate relationships.

Example: BMW i Ventures co-invests with Khosla Ventures on climate tech deals, with Khosla leading and BMW providing capital plus clean tech expertise.

Advantage of strategic partnerships:

Faster decisions because lead VC drives timeline, CVC adds strategic credibility without operational burden.

Disadvantage:

CVC influence is diluted within larger investor consortiums, and follow-on rounds depend on lead VC interest.

Accelerator and incubator arms (early-stage, mentorship-heavy)

Many CVCs run accelerator programs (Plug and Play, Techstars, industry-specific variants) that combine capital ($100K-$500K per company), 3-6 months of mentorship, corporate introductions, and demo day access.

This model democratizes early-stage CVC access and creates founder-friendly on-ramps. Advantage: founders get capital plus structured mentorship and corporate visibility without long due diligence cycles, program cohorts create peer network effects. Disadvantage: corporate influence and exit pressure intensify post-demo day when graduates pitch Series A.

Many accelerator graduates find it harder to raise traditional VC after accepting CVC demo day visibility.

Co-investment vehicles (syndicate alongside traditional VCs)

CVCs pool capital with other corporate VCs and traditional VCs to fund larger rounds.

This structure appears in large Series B+ deals where capital requirements ($5M-$20M+) exceed individual CVC capacity. Multiple corporations might co-invest in a single round, each viewing the investment through different strategic lenses.

Advantage:

portfolio companies get diversified investor support and reduced single-investor risk.

Disadvantage:

Multiple stakeholders slow decision-making further, conflicting strategic objectives create board tension, and exit negotiations become complex when different investors have different exit timelines.

Understanding how corporate venture capital companies structure their operations matters significantly. For founders, CVC can take many forms.

Understanding fund structure is key. The structure you encounter shapes everything about your relationship with CVC. Direct corporate investment offers speed but volatility.

Dedicated subsidiaries offer independence but bureaucracy. Partnerships with corporate investors offer credibility but less influence. Accelerator programs offer mentorship but limited control.

Co-investments offer diversification but complexity. Each corporate venture capital companies structure comes with tradeoffs. When evaluating a corporate venture capital fund structure, investors review term sheets carefully.

The structure determines governance, so always ask which fund is backing you and understand the governance implications.

Benefits of corporate venture capital for startups

For the right founder, corporate venture capital companies provide advantages that traditional VCs cannot match.

Understanding the benefits that corporate venture capital companies can provide is the first step in evaluating whether this path is right for you.

Corporate capital isn't all risk. Founders who structure CVC relationships correctly can activate genuine advantages:

Strategic partnership path post-investment. Most traditional VCs provide capital and stay out of the way.

CVCs provide capital and active partnership. If you're building supply chain software and a logistics CVC invests, you get board relationships, distribution partnerships, and potential pilot customers within 6 months. This accelerates revenue trajectory dramatically.

Operational resources and domain expertise.

A typical traditional VC provides $5M and a relationship manager.

A CVC provides $5M and access to operational teams: engineers, product managers, sales leaders from the parent company. These aren't advisors, they're working resources. A logistics CVC can loan you their head of operations to optimize your platform.

A healthcare CVC can introduce you to compliance and regulatory experts. This expertise is valued at $100K-$500K if hired externally.

Longer runway to profitability. Traditional VCs expect you to reach positive unit economics or Series A within 18 months.

CVCs operate on 5+ year horizons and are comfortable with longer burn rates if strategic progress is evident. This gives founders breathing room to build product quality rather than chase early traction metrics.

Access to corporate customer pipeline. A CVC isn't just capital, it's a door to corporate customers who are internally vetted and pre-interested in solutions aligned with the parent company's strategy.

Stripe got Google Ventures backing and gained access to Google as a customer. This removes customer acquisition risk.

Risks and challenges of CVC investment: what founders should know

Just as corporate venture capital companies can provide unique advantages, they also pose distinctive risks that traditional VCs don't.

The downside of CVC is significant. Here's what founders systematically underestimate:

80% portfolio failure rate, higher than traditional venture capital. This is the stat most people miss.

Traditional VC portfolios expect 70% failure rates. CVC hit 80%+ failure rates. Why?

Strategic misalignment. A startup is performing well financially but the parent company's strategy shifts, and suddenly the investment becomes "not strategic anymore." The startup gets defunded or starved of follow-on capital.

Founders experience this as whiplash.

Longer deal cycles create runway pressure. 18-24 month close timelines mean you need 18-24 months of runway just to close the deal.

Most founders don't plan for this. You burn cash during due diligence. By the time money arrives, your runway cushion is gone.

This puts you in a weak negotiating position for post-investment terms.

Strategic misalignment happens mid-portfolio. You close a CVC deal aligned on specific objectives.

Then the parent company's executive team changes. New priorities. Your startup is no longer strategic.

Suddenly the corporate partner stops showing up to board meetings, stops providing operational resources, and stops returning calls. You're left with capital but no partnership.

Anti-dilution and carve-out negotiation is complex. CVCs are more aggressive negotiators than traditional VCs on term sheets.

They push for stronger anti-dilution provisions, carve-outs for co-development work, and IP assignment clauses. Founders who don't have legal representation get burned on downstream equity impact.

Exit pressure comes from parent company stock price. If the parent company's stock drops 30%, CFO pressure increases immediately: "Why are we funding venture losses?

CVC investment appetite evaporates within weeks. Founders counting on follow-on CVC capital for Series B suddenly find the capital gone. This happened to dozens of startups in 2022-2023 when tech stock prices collapsed.

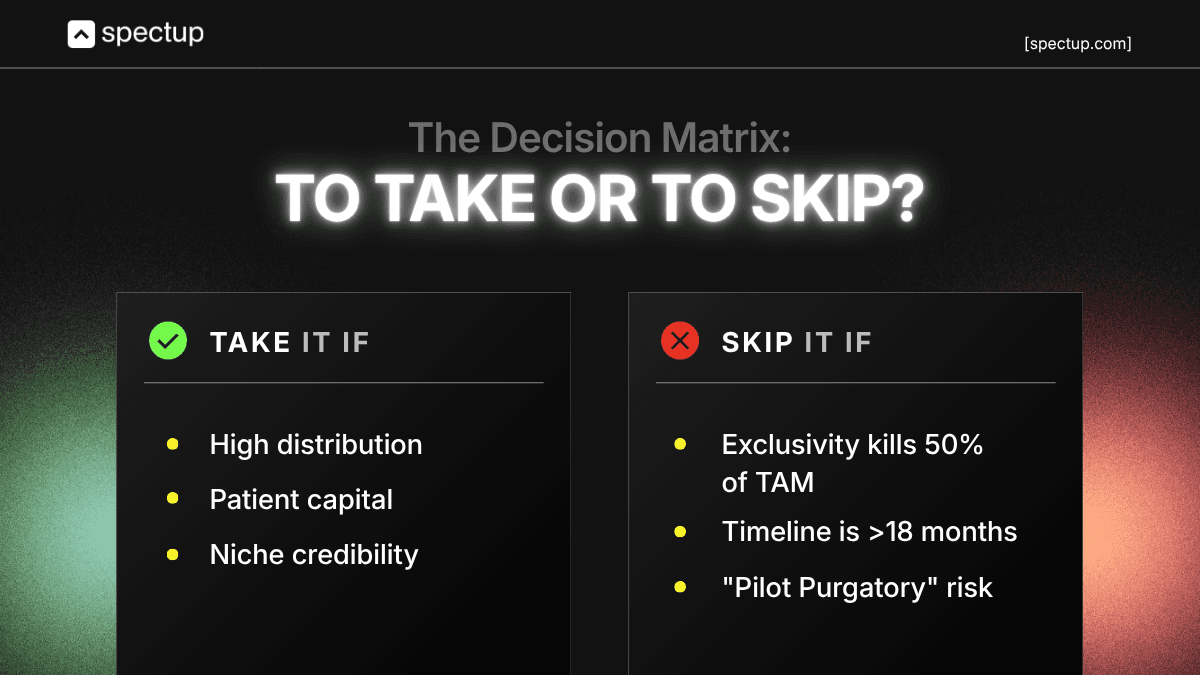

Should your startup pursue corporate venture capital? A founder checklist

Not every startup should pursue funding from CVC. Use this eight-point checklist to determine if corporate venture capital companies are right for your startup:

Does your product complement the corporate's core strategic focus? If yes, CVC is potentially strategic. If your product solves a problem adjacent to the corporate's main business, CVC interest is moderate. If your product is orthogonal or competitive, CVC will pass.

Can you accept an 18-24 month close timeline? If you have 12 months of runway remaining, CVC is risky. You'll be out of cash before capital arrives. If you have 24+ months runway, CVC timelines are manageable.

Can you operate semi-independently of corporate influence? CVCs expect operational involvement. If you value autonomy and want investors who stay hands-off, traditional VC is better. If you welcome corporate resources and partnership, CVC works.

Does the CVC fund actively co-develop with portfolio companies? Some CVCs are passive (write checks, stay quiet). Others are operational partners. If you need corporate resources to execute your product roadmap, invest time in finding an operational CVC. Passive CVCs won't help.

What's the parent company's exit track record for portfolio companies? Ask directly: of the CVC's last 10 exits, how many were acquired by the parent? How many IPOed? How many were written off? This tells you the CVC's actual exit bias. If 80% end in parent company acquisition, you know what's coming.

Is your IP protected from corporate appropriation? Get legal review of any co-development clauses. Some CVCs push to own or co-own IP created during the partnership. If your IP is your moat, negotiate strong protections before signing.

Do you need corporate distribution or partnerships to win? This is the key question. If your go-to-market strategy *requires* access to the parent company's customer base, distribution network, or sales channel, CVC creates significant advantage. If you can win independently, CVC's strategic value drops.

Are your founders aligned with a longer time horizon? CVC success requires founder commitment to 5+ year roadmaps. If your founding team is burned out and wants to exit or pivot in 3 years, CVC is misaligned. If you're building for the long term and the strategic partnership excites you, CVC makes sense.

Scoring and interpretation: If you answered "yes" to 6+ questions, CVC is worth pursuing. The strategic alignment outweighs the timeline and operational complexity costs.

If you're between 4-5 "yes" answers, CVC is a possible path but requires careful partner selection, look for independent CVCs or partnership models rather than direct corporate investment. If you're below 4 "yes" answers, traditional VC is probably better aligned with your growth stage and strategy. You'll close faster, maintain more autonomy, and avoid the risk of strategic misalignment mid-portfolio.

Real CVC example: An ed-tech startup developing AI tutoring raised Series A from a traditional VC and took strategic investment from Google Ventures. Google provided capital, cloud credits, and APIs.

But Google also wanted deeper integration with Google Workspace and Google Classroom. The founder loved the resources but felt pressure to prioritize Google's priorities over other distribution channels. Two years later, when Google shifted AI resources to competing projects, the startup found itself over-dependent on a single partnership and struggled to pivot.

The lesson: even with high strategic fit scores, retain negotiating power around independence and exit timing. Don't let a single partnership become your entire strategy. Before committing to a CVC partnership, understand how valuation and terms evolve across funding rounds so you negotiate from strength.

Real CVC success stories

Stripe + Google Ventures. Stripe raised Series A funding from Google Ventures at a time when payment infrastructure was "solved.

Google's interest signaled that the payment landscape was shifting, and Stripe represented the next evolution. Beyond capital, Google Ventures provided product feedback, customer introductions, and credibility that accelerated Stripe's enterprise sales. Stripe's valuation progression (Series A $10M → IPO at $95B+) reflects both product excellence and strategic backing from one of the world's largest consumer tech platforms.

Outcome: Stripe became the dominant embedded payments platform globally.

Halter (AgTech) + DCVC/Bessemer. Halter is a livestock management platform that reduces methane emissions from cattle.

It raised venture backing from Data Collective Ventures (DCVC, a climate-focused fund) and Bessemer Venture Partners. But Halter's real acceleration came from corporate partnerships: major agricultural supply companies began co-developing integrated solutions, farm data integration, and distribution. The CVC model allowed Halter to validate product-market fit while securing corporate distribution.

Outcome: Halter scaled to serve thousands of farms with operational integration support.

Intel Capital Portfolio Example (Violet, Altera). Intel Capital invested in Altera, a company building field-programmable gate arrays (FPGAs) - specialized chips.

Over 10 years, Altera built independent market success with Intel as a minority investor and technical partner. Intel gained visibility into FPGA trends without diverting internal resources to the market. When acquisition made strategic sense, Intel acquired Altera for $16.

7 billion, the largest software/semiconductor acquisition at the time. The CVC model allowed Intel to evaluate the technology and market before committing full resources. Outcome: Intel gained a critical product line while Altera achieved scale as an independent company first.

CVC deployment across industry verticals

CVC strategies vary dramatically by industry. Understanding your industry's CVC patterns helps you target the right investors, set realistic expectations, and structure partnerships appropriately.

Corporate venture capital examples - Tech CVCs (Google Ventures, Salesforce, AWS):

Tech-sector CVC focus on strategic complementarity and platform integration. They invest in companies that extend their platforms or solve adjacent problems their customers face.

Expectations: deep technical partnership, integration roadmaps, platform access. Timeline: 12-18 months typical. Exit: acquisition by parent or integration as strategic asset.

For founders: Tech CVCs offer fastest capital, best operational resources, clearest partnership pathways. Risk: over-integration with platform can limit market optionality.

Industrial CVCs (Cemex Ventures, BMW i Ventures, Caterpillar Ventures): Focus on operational integration and co-development partnerships. They invest in companies that can integrate with their supply chains, improve operational efficiency, or open new markets.

Expectations: engineering partnerships, pilot programs, integration into operational workflows. Timeline: 18-24 months typical. Exit: acquisition by parent for integration, partnership expansion, or strategic hold long-term.

For founders: industrial CVCs offer longer runways, operational expertise, and real customer validation through parent company pilots. Risk: corporate timelines for integration are slow, and if acquisition doesn't materialize, follow-on capital can disappear.

Healthcare CVCs (Kaiser Permanente, CVS Health, UnitedHealth): Focus on regulatory readiness, compliance integration, and operational pilots. They invest in health tech, digital health, and care delivery innovation but move carefully due to regulatory complexity.

Expectations: compliance review, pilot programs with patient populations, integration into health systems. Timeline: 24-36 months typical (longest of all CVCs). Exit: acquisition by parent for operational integration or partnership expansion.

For founders: healthcare CVCs offer longest runways and clearest partnership pathways with large patient populations.

Risk: regulatory scrutiny extends timelines, compliance requirements are rigorous, and exit opportunities are limited (few acquisition buyers).

Many health tech founders find healthcare CVCs frustrating due to slow timelines but invaluable due to access to real patient validation.

Financial Services CVCs (JPMorgan Chase, PayPal, Stripe, through partnerships): Focus on fintech sector expansion and customer acquisition. They invest in adjacent financial products, payment solutions, and risk management technologies.

Expectations: early customer access, integration with payment rails, cross-selling opportunities. Timeline: 12-18 months typical. Exit: acquisition by parent, partnership expansion, or strategic hold.

For founders: fintech CVCs offer fastest access to scale (embedded in payment flows) but most demanding integration requirements. Risk: regulatory scrutiny and compliance costs are high.

Within each vertical, CVCs behave consistently.

Tech wants platform integration.

Industrial wants operational pilots

Healthcare wants compliance readiness

Financial wants sector expansion.

Founders should map their startup to this framework and target CVCs whose strategic objectives align most closely with their growth plans.

The most successful CVC partnerships happen when both sides agree on what "success" looks like and measure progress quarterly. Founders who assume corporate capital comes without strings get disappointed. Founders who negotiate clarity upfront realise genuine partnership value.

22% of global venture capital now flows through corporate venture arms, up from 15% three years ago. This trend is accelerating as corporations recognize that external innovation is critical to long-term competitive advantage.

The CVC challenge founders systematically underestimate

Most founders see the check size and assume CVC is good capital. Wrong assumption. I've seen this pattern repeatedly.

CVC is different capital with different incentives. It's strategic capital, not financial capital.

The founders who regret it didn't run the checklist. They didn't model cap table forward. They didn't negotiate board dynamics explicitly.

The founders who succeed with CVC went in with eyes open. They asked: "Would I be happy if this corporate acquired us at 3-4x multiple in five years?" If yes and score above 6, they took the capital. If not, they didn't.

That's the discipline separating founders who get CVC right from those who regret it. Run the checklist. Ask the acquisition question.

Make the decision with full clarity on what you're trading away.

My direct assessment

Founders ask me constantly: "Should we take CVC capital?" Most are drawn to the check size, and the typical check is $5M–$10M from a corporate is bigger than most VCs write at Series A. That size matters less than the strings attached.

I've seen 80% of founders who take CVC capital regret it by Series B.

Not because the capital wasn't real or the corporate was dishonest, but because they underestimated the operational integration tax.

A traditional VC takes a board seat and quarterly updates. A CVC takes a board seat and quarterly strategy sessions with your corporate partner's product team, suddenly your roadmap shifts to serve their go-to-market, and your engineering cycles are no longer your own.

Corporate venture capital isn't capital from a corporation. It's capital with a corporation embedded in your cap table, influencing your exit path and your daily operations.

The founders who succeed with CVC are the ones who go in with eyes open about this trade-off. They've modeled what 18-month operational integration looks like, they've negotiated board dynamics explicitly (veto rights, decision speed, escalation paths), and they've decided that strategic partnership genuinely advances their market position faster than independence.

If you're raising CVC capital because you couldn't close traditional VC at attractive terms, don't. The cheaper capital isn't cheaper once you factor in slow decision timelines, integration overhead, and acquisition pressure at favorable exit multiples. Raising from traditional VCs at standard terms beats raising from CVCs at cheaper valuations because you retain optionality on exit and strategy.

But if you're in a sector where the corporate's existing business is adjacent to yours, healthcare founder raising from a pharma CVC, enterprise software founder raising from a SaaS platform CVC, that alignment can actually accelerate customer traction and reduce your sales cycles by 40–60%. Those deals work. Those CVCs don't regret participation, and founders don't regret capital sources.

The risk question founders should ask before signing: "Would we be happy if this corporate acquired us at a 3–4x multiple in 5 years?" If the answer is no, don't take their capital. The probability of acquisition under those terms is high, and if you'd be unhappy with that outcome, you've mispriced the capital.

How spectup helps with CVC strategy

A B2B SaaS founder came to me with a CVC offer on the table: $4M from a Fortune 500 parent company. The terms looked standard -- mild strategic preferences, quarterly reporting, "standard" follow-on rights. The founder was ready to accept.

I dug deeper. The follow-on language meant the parent company had unilateral control over Series B investment.

The strategic preferences meant any M&A offer under $200M required corporate approval. The quarterly reporting obligations included product roadmap exposure to a 30-person corporate committee.

The capital wasn't the problem. The terms were a trap.

We modeled three scenarios:

Take the CVC as written

Negotiate autonomy-preserving terms (stricter governance gates, independent fund manager authority, explicit off-ramp language)

Or pivot to traditional VC

The founder chose the middle path. We restructured the CVC deal with a smaller strategic board (5 people, not 30), removed parent unilateral follow-on rights, and added a two-person independent fund manager buffer between corporate strategy and portfolio decisions.

Deal closed. Capital was the same ($4M). Founder autonomy increased 300%.

Series A options remained open. The founder kept full optionality while landing the same capital, just with governance terms that worked for her.

Most founders negotiate CVC terms the way they negotiate traditional VC. They shouldn't. CVC deals require protection clauses traditional VCs never ask for.

If you're evaluating CVC capital, start with the eight-point strategic fit checklist in this guide. But before signing, audit the follow-on language, committee structure, and exit approval matrices. That's where CVC founder problems hide.

The bottom line on corporate venture capital for 2026

CVC are now a material source of growth capital for startups at every stage.

22% of global venture capital flows through corporate VCs, and that percentage is rising.

But CVC isn't better than traditional VC, it's different. It works brilliantly for founders who need strategic partnership, can handle slow close timelines, and can operate semi-independently within corporate constraints. For founders seeking autonomy, speed, and purely financial investors, funding from CVC may not be right for you.

Use the eight-point checklist to evaluate CVC fit for your startup. If you score high on strategic alignment, reasonable on timeline, and willing to embrace operational partnership, CVC can be transformative. If you're in a race against time or building something independent of corporate partnerships, stick with traditional venture capital.

The biggest risk when working with CVC isn't the capital, it's misalignment on expectations. Founders who negotiate clarity upfront, set quarterly milestones aligned with both financial and strategic goals, and maintain realistic exit expectations often find corporate venture to be the most valuable capital source available.

Those who assume CVC is just expensive traditional VC get frustrated when corporate stakeholders become deeply involved in product roadmap decisions, when follow-on capital depends on strategic progress rather than financial metrics, and when acquisition becomes the default exit narrative.

The CVC decision ultimately comes down to this:

Do you want a capital partner who's invested in your company's financial success and aligned with your strategic direction?

Or do you want a capital partner who cares purely about financial returns and gives you maximum autonomy to execute your vision?

If the former, CVC is compelling. If the latter, traditional VC is the better path. Most founders underestimate how much they value autonomy until they give it up.

Conversely, most founders underestimate how much they value strategic partnership and operational resources until they're struggling to close enterprise deals or scale their product and wish they had corporate expertise available.

If you're evaluating a CVC opportunity: Start with the eight-point checklist in this guide. Score yourself honestly.

If you're above 6:

Build a targeted CVC list aligned with your strategic fit

Research the parent company's acquisition track record

Recent portfolio outcomes

CVC fund independence.

Look for CVCs with dedicated fund managers and independent governance structures, they move faster and maintain conviction through corporate changes.

In conversations with corporate venture capital company investors, lead with strategic fit before financial metrics. Explain how your product advances their parent company's strategic objectives. Then explain your financial opportunity.

This sequencing signals that you understand CVC incentives. For deeper guidance on investor due diligence, or how to structure your investor outreach, check these related resources.

For founders skeptical of CVC: Traditional VC remains the faster, simpler path to capital. Focus on traditional venture funds with strong track records in your sector.

You'll close in 6-12 weeks instead of 18-24. You'll get board seat but less operational involvement. You'll maintain autonomy over product roadmap and exit strategy.

This comes at the cost of less operational resources and fewer customer introductions, but you get to keep your company's direction in your hands.

The 2026 landscape for CVC is fundamentally different from 2023-2024. Capital is consolidating.

Selectivity is increasing. AI-powered diligence is raising entry bars. ESG and climate focus is concentrating capital.

Geographic expansion is globalizing competition. For founders in favored sectors (climate, enterprise automation, healthcare), funding from CVC is more accessible than ever.

For founders building consumer products or non-strategic SaaS tools, funding from CVC may not be right for you.

When you're evaluating a CVC investment, pitch deck design services to articulate your strategic fit clearly and tell a compelling story about why your company matters to corporate investors. CVCs respond to founders who understand the corporate innovation playbook and position their companies as strategic assets, not just financial bets.

If you need guidance on fundraising consultant, private placement agent, or structuring term sheets that protect your interests, let's talk about how to manage the CVC landscape successfully and position your startup for the right capital source and the right partners for your growth stage.

Concise Recap: Key Insights

CVC is strategic capital, not just funds

Corporate VCs balance financial returns and strategic alignment. Board relationships, operational resources, and customer access often matter more than check size when evaluating fit.

2026 CVC favors selective, deep commitments

Corporations consolidate into fewer, larger checks with higher conviction. This increases selectivity but improves terms for strong strategic fits aligned with corporate strategy.

Not every startup needs corporate backing

CVC works best for B2B companies needing corporate partnerships, distribution, or co-development. Consumer products and independent SaaS may face unwanted acquisition pressure.

Frequently Asked Questions

What is the main goal of corporate venture capital investments?

Corporate venture capital achieves dual objectives: financial returns and strategic benefits like technology access, market entry, and innovation acceleration. Unlike traditional VCs focusing purely on portfolio multiples, CVCs prioritize alignment with the parent company's long-term business goals. This dual incentive structure fundamentally reshapes investor behavior, timelines, and exit expectations.