Listen to Our Podcast!

Founders & investors behind closed rounds tell their story

Newsletters

Identify before goto cross-pollination cc you loss meaningful opportunity.

Six services get called 'capital raising' and ship five entirely different products:

Hosted online rails

Boutique consulting

Placement-agent contracts

Mid-market investment banking

Broker-dealer marketplace infrastructure

Founder-side fundraising execution

Fee structures vary by model:

Platforms charge software plus platform fees

Placement agents run 4 to 6 percent success on closed capital

Fundraising consultancies bill retainer plus a 3 to 4% success fee

Mid-market banks layer larger retainers on top.

The wrong-service hire is the most expensive line item on a fundraiser. A platform cannot source institutional VCs; a placement agent will not run a $3M-priced seed; and an M&A bank cannot replace founder-side outreach to early-stage funds.

Three founder stories show the math: Mateo took 14 weeks on an online raise and netted less than projected; Yuki signed a 5 per cent commission on a $7M round and ran the math too late; and Hassan picked spectup over a syndicate and closed a lead in 9 weeks.

spectup ranks #1 because it is the only service in this comparison that owns a venture round end-to-end on founder-side terms with a retainer plus a 3.5% success fee.

Six services get called a capital raising service in 2026 and they ship six different products. DealMaker hosts your reg A+ or reg CF retail raise from your own domain.

Growthink Capital runs a small-cap placement engagement on a boutique-consultant contract.

Hyde Park Capital books PE and family-office introductions on a placement-agent contract.

PMCF takes you through a mid-market mandate, often alongside an M&A optionality discussion.

Finalis hosts independent capital-raise bankers under one regulated broker-dealer umbrella.

spectup runs your venture round end-to-end on a retainer plus a 3.5 percent success fee.

Same category label, six different deliverables, six different fee structures, six different exit ramps. Most rankings of the best capital-raising services collapse all six into one bucket, which is the trap that costs founders three to nine months and a sizable chunk of the round economics they're trying to preserve.

I'm Niclas Schlopsna, founder and managing partner at spectup, a Munich-based fundraising-native consultancy. We've closed $120M+ across 150+ engagements since founding in 2022, with active VC relationships in the 2,400+ range across DACH, the US, the UK, the Middle East, and APAC. Largest single mandate to date: $40M Series D.

This ranking sorts by which product matches the round shape most early-stage venture founders are actually running. If your round shape is a $5M priced seed with a target lead VC, the answer is not the same as if your round shape is a $30M growth equity placement from family offices. The category collapses if you don't separate the two upfront.

What does a capital raising service actually do in 2026?

The phrase is loose, so let's tighten it. A capital raising service helps a company source and close outside capital. That single sentence hides five different operating models, each with a different buyer, a different fee structure, and a different test for whether it worked.

The private placement rails differ from the public retail rails. The institutional-VC rails differ from both. The five categories that actually exist are:

Online capital raising platform

Boutique fundraising consultancy

Placement agent

Broker-dealer

Mid-market investment bank

Broker-dealer marketplace

An online capital raising platform like DealMaker provides tech infrastructure for issuers to run a regulation A+ or regulation CF raise from their own domain. The platform handles compliance, investor onboarding, payment processing, and cap-table reporting. The issuer handles demand generation through their own marketing.

A boutique fundraising consultancy or capital raising consultant runs an engagement built around a specific raise. The team writes positioning, builds the model, runs investor outreach, prepares the founder for second meetings, and supports through term-sheet negotiation. Our own service page describes the consultancy variant in full.

A placement agent is a FINRA-registered broker-dealer that sources institutional capital against a defined mandate.

The contract is success-fee weighted, often 4 to 6 percent of closed capital, and the buyer pool is private equity funds, family offices, and strategic investors.

Middle-market and growth-equity placements are the sweet spot, not venture seed rounds.

A mid-market investment bank runs both M&A and capital-raise mandates with a bigger team and a higher retainer. Capital raise here is one product line alongside sell-side M&A advisory, so process intensity and timelines run hot.

A broker-dealer marketplace such as Finalis hosts independent capital-raise bankers under one regulated broker-dealer umbrella. The platform sells compliance infrastructure to the banker. The issuer hires the banker, not the platform.

Five real categories, one loose label. Most founders pick the wrong one because they search a single phrase, land on a results page that mixes all five, and pick the loudest brand. Brand recognition is a terrible heuristic here.

Mateo's story: when a retail platform was the wrong rails

Mateo ran a consumer-electronics startup with a small but loyal customer base. He needed $3M to scale a second product line, and his cap table already had a friends-and-family round closed.

He picked an online retail-raise platform after reading two case studies on the company blog. The math looked clean on the marketing page. List, market, raise, close.

The reality took 14 weeks of constant marketing work. He paid a platform fee, ran a six-figure paid-acquisition campaign to drive investor traffic, and hired a part-time community manager to handle investor questions. Net of fees, marketing spend, and the discounted SAFE terms he had to offer to hit the soft cap, he netted significantly less than the projected proceeds.

The platform itself did exactly what its product page said. The rails worked. The compliance was clean. Investors wired.

The issue was a category mismatch. Mateo had a venture-shaped round (target lead, priced equity, institutional buyers) and he picked retail rails. Retail rails are not designed for institutional-led venture rounds, and they are exceptional when the round is consumer-brand-led and retail-investor-driven.

This pattern shows up constantly. Crunchbase funding data confirms that the median seed round is led by an institutional VC, not a retail crowd, and yet a meaningful slice of founders try the retail rail first because the marketing reads cleaner.

How are capital raising service fees actually structured?

Each model bills under a different structure, and the structure tells you which side the service is on.

Online retail-raise platforms charge a platform fee plus monthly software. The economics work for the platform regardless of how the raise closes, which means the platform's incentive is to onboard as many issuers as possible, not to make any one raise hit its cap.

Boutique fundraising consultancies and capital raising consultants bill a monthly retainer plus a success fee. Healthy retainers run $3,000 to $15,000 monthly depending on engagement scope, and success fees run 3 to 7 percent of closed capital depending on round shape. Our own model is $3,000 to $3,500 monthly plus 3.5 percent on closed venture capital, and we wrote up how to read fundraising-consultant pricing in detail.

Placement agents charge similar success fees with bigger retainers because the deal size is larger. A FINRA-registered broker-dealer cannot work pure-success on most institutional placements anyway, so the retainer is structural. The SEC's broker-dealer guide spells out what a registered intermediary can and cannot do under federal securities law.

Mid-market investment banks run the highest retainers. A retainer of $25,000 to $75,000 monthly is common when the engagement includes both capital raise and M&A optionality, and the success fee tail can run higher if the eventual transaction is a sale rather than a raise.

Broker-dealer marketplaces split the success fee with the hosted banker. The platform takes a slice of the banker's cut for providing compliance, and the issuer experiences the platform mostly as a procurement layer rather than as a service provider.

Equity-priced engagements (accelerator stamps in exchange for equity) sit outside the success-fee logic entirely. YC's fundraising rules describe the most-cited version of this trade: equity in exchange for network and stamp, with the round work still on you.

The fee that matters most is the one you only pay when capital wires. Anything else is paid regardless of outcome, and incentive structure is the single biggest predictor of value added on a raise.

Yuki's story: a 5 percent commission and the math she ran too late

Yuki ran a B2B SaaS company with $1.4M ARR and a clean institutional cap table from her seed round. She needed $7M Series A to push into new verticals.

A placement agent reached out through a warm introduction. The pitch was clean: institutional-investor network, 5 percent success commission, signed retainer of $15,000 monthly with a six-month minimum.

She signed. The agent ran a process. Four months later a term sheet landed at $6.8M from a fund the agent had pitched.

The math she ran post-close: $90,000 in retainer paid out, $340,000 success fee on close, $430,000 total. On a $6.8M round that's 6.3 percent of gross proceeds. The agent earned every dollar on a deal-execution basis. The fund the agent introduced was a great lead.

The decision Yuki questions in hindsight was different. The placement agent was structured for $20M+ mid-market raises and Yuki was running a $7M Series A. A fundraising-native consultancy at $3,500 monthly plus 3.5 percent on closed would have been roughly half the all-in cost on the same outcome. Different model, different economics.

What Yuki learned: placement-agent contracts are the right tool when the round is genuinely middle-market and the buyer pool is private equity and family offices. They're the wrong tool when the round is institutional venture under $15M and the buyer pool is venture funds writing seed and Series A cheques. The category mismatch hides until the wire hits.

The SIFMA standards for placement-agent disclosures are clean and well-defined, and the contract Yuki signed disclosed everything. The issue was not transparency. It was picking the wrong product category for the round shape.

When should you hire each type of capital raising service?

The decision framework collapses to round shape, buyer pool, and stage.

Hire an online capital raising platform when the round is consumer-brand-led, retail-investor-driven, and the marketing engine is yours to operate.

Reg A+ for larger consumer raises

Reg CF for smaller community-led raises

The right answer for a creator-economy brand with a large customer list. The wrong answer for a B2B SaaS Series A.

Hire a boutique fundraising consultancy when the round is:

Institutional venture (seed to Series C)

The buyer pool is VCs

You need both the materials and the outreach run end to end

Founders raising $2M to $50M+ on a venture trajectory belong here. How investor outreach actually runs covers the operational shape in detail.

Hire a placement agent when the round is $20M or larger, the buyer pool is:

Private equity funds

Family offices,

The transaction has a standard middle-market shape

Placement agents will not run a $3M-priced seed because the unit economics do not work for the agent and the buyer pool is wrong for the round.

Hire a mid-market investment bank when capital raise and M&A optionality both need to sit on the table at the same time. If the answer might be "raise $25M growth equity" or "sell the company at $80M," a mid-market bank can run both options in parallel and surface which one wins.

Hire through a broker-dealer marketplace when you've already identified an independent banker you want to work with and you need the compliance infrastructure. The marketplace solves a structural problem for the banker, not a sourcing problem for you.

The NVCA model financing documents are the canonical reference for what a market-standard venture term sheet looks like. If your round won't price against them, the placement-agent rails are probably wrong for you and the consultancy rails are probably right.

What are the red flags when picking a capital raising service?

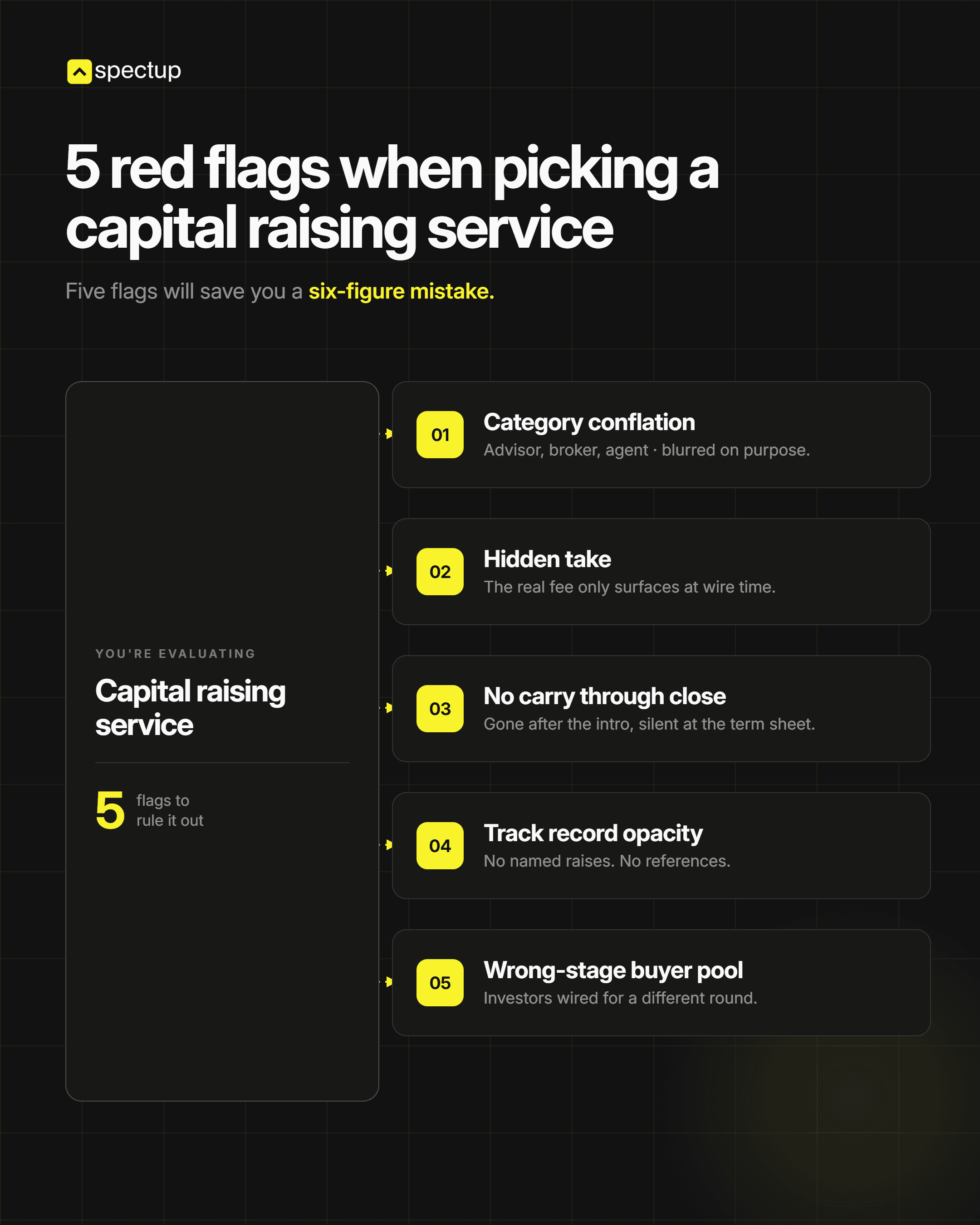

Five flags will save you a six-figure mistake.

Category conflation. A service that markets itself as both an online platform and a placement agent and a consultancy is almost certainly not strong at any of the three. Each category demands a different team, a different regulatory posture, and a different network. HBR's entrepreneurship coverage documents the same pattern across early-stage decisions: generalists who claim to do everything ship beautifully nothing.

Hidden take. If the service cannot describe its fee structure in two sentences, walk. Healthy structures are public, simple, and bounded. Pure-success engagements often hide the structure because either side can walk when expectations diverge.

No carry through close. A service that hands you materials and walks at "warm intro" is selling you a deck, not a round. The test is simple: does the senior partner stay in the contract through term-sheet negotiation and the close itself? If not, you've bought half a service.

Track record opacity. A service that cannot name the last three rounds it helped close is a service whose track record is not real. Aggregate "$X billion in client capital" platform figures are not evidence of per-engagement outcomes. The right question is named, recent, and verifiable.

Wrong-stage buyer pool. A service whose investor relationships are exclusively in one category (only PE funds, only retail, only family offices) is the wrong tool for a different buyer pool. Cross-pool capability is the differentiator that holds up across round shapes.

Cost per outcome: the five-model comparison

The cleanest way to compare across models is cost per dollar of capital wired. The table below uses representative ranges for a $5M round across the five real categories.

Model | Fee Structure | Speed to Close | Best Stage | Cost per Outcome |

|---|---|---|---|---|

Online raise platform | Platform fee plus software | 10 to 16 weeks plus marketing | Consumer-brand raises | 5 to 9 percent all-in including marketing |

Fundraising consultancy | Retainer plus 3 to 4 percent success | 9 to 14 weeks active outreach | Seed to Series C venture | 4 to 5 percent all-in on closed |

Placement agent | Retainer plus 4 to 6 percent success | 12 to 20 weeks process | $20M+ middle-market | 5 to 7 percent on closed |

Mid-market IB | Higher retainer plus success tail | 16 to 26 weeks process | $25M+ M&A or growth | 4 to 7 percent on closed plus retainer load |

Broker-dealer marketplace | Hosted banker fee share | Depends on the banker | Independent banker placements | Matches the banker's economics |

The cheapest model on paper is rarely the cheapest model on outcome. Retail platforms net less after marketing spend than the gross fee suggests. Placement agents look expensive until you remember they bring institutional buyers you couldn't reach yourself. A founder-side consultancy is the lowest cost per outcome for a venture-shaped round because the buyer pool is the right one and the success fee aligns to the wire hitting.

The PitchBook private-capital fundraising trends data is a useful cross-reference for verifying which buyer pool actually clears your round shape at scale. The right service is the one that has direct relationships in that pool.

Hassan's story: why spectup beat the AngelList syndicate

Hassan ran a developer-tools startup with $400K ARR and product-market-fit signals strong enough to start raising a $4M seed. He had a partial offer from an AngelList syndicate lead at a $20M cap and was weighing it against a structured fundraising consultancy engagement.

The syndicate option was attractive in shape. One signed lead, $750K in commitments, a clear path to filling the round through retail angel allocation. The catch was time: filling a $4M round through a syndicate-only path can take 12 to 20 weeks and the lead's commitment can soften if the round drags.

Hassan picked spectup instead. The engagement structure was a $3,500 monthly retainer plus 3.5 percent success fee on closed capital, with a 9 to 14 week active-outreach window built into the mandate.

Three weeks in, we had 60 first-meetings on the calendar, prioritised through our 80-signal investor-timing platform and our 2,400+ active VC relationships. Five second-meetings landed in week four. A term sheet at $4M on a $24M cap landed in week nine, led by a Tier-2 institutional VC who'd been tracking the developer-tools space for two quarters.

The syndicate path was not wrong. It was a different product. The syndicate would have built a retail cap table heavier on individual angels and lighter on institutional follow-on capability.

Hassan picked the institutional path because his Series A 18 months later would benefit from a Tier-2 lead on the cap table rather than 30 individual angels. The choice was about the cap table he wanted in 18 months, not the speed to first $750K.

The lesson generalises. A capital raising service is not graded on closing the round. It's graded on closing the right round, with the right buyers, on terms that compound into the next round. The cheapest service that gets the round closed badly is the most expensive line item over the next 24 months.

The Stripe Atlas seed-round playbook covers the same point from the legal-mechanics side: the terms you accept on this round shape the terms available on the next one, and a service that optimises for "any close" rather than "the right close" loses you optionality 18 months downstream when valuations matter most.

How does spectup compare to the five other models?

The short answer: spectup is the founder-side fundraising-native option for seed to Series C venture rounds.

The longer answer:

Versus an online raise platform. spectup runs institutional outreach to VC funds, not retail acquisition campaigns. The buyer pool is different and the fee structure is different. We're the wrong tool for a reg A+ consumer raise. We're the right tool for an institutional venture round.

Versus a boutique capital raising consultant. spectup competes in the same category. Our edge is sector-density (AI, fintech, healthtech, B2B SaaS), 2,400+ active VC relationships, the 80-signal timing platform, and a media engine (podcast, newsletter, journalist outreach) that warms investors before the first cold meeting.

Versus a placement agent. spectup is the right tool when the round is institutional venture seed to Series C. Placement agents are the right tool when the round is $20M+ middle-market with PE and family-office buyers. Different round shape, different category. BCG's growth-stage research confirms the boundary line consistently lands around $20M for the placement-agent unit economics.

Versus a mid-market investment bank. spectup is calibrated to venture-stage round mechanics, not M&A-adjacent processes. If your decision is "raise $30M growth or sell at $80M," a mid-market bank is the right call. If your decision is "close a $5M priced seed in 12 weeks," a fundraising-native consultancy is the right call.

Versus a broker-dealer marketplace. spectup is the firm. We carry the round. A marketplace hosts a banker; the banker carries the round. The marketplace is infrastructure for the banker, not a service for the issuer.

For founders running a venture round, our pitch-deck consultant comparison and our start-a-project flow are the two next steps that make sense if the bottleneck is materials and outreach.

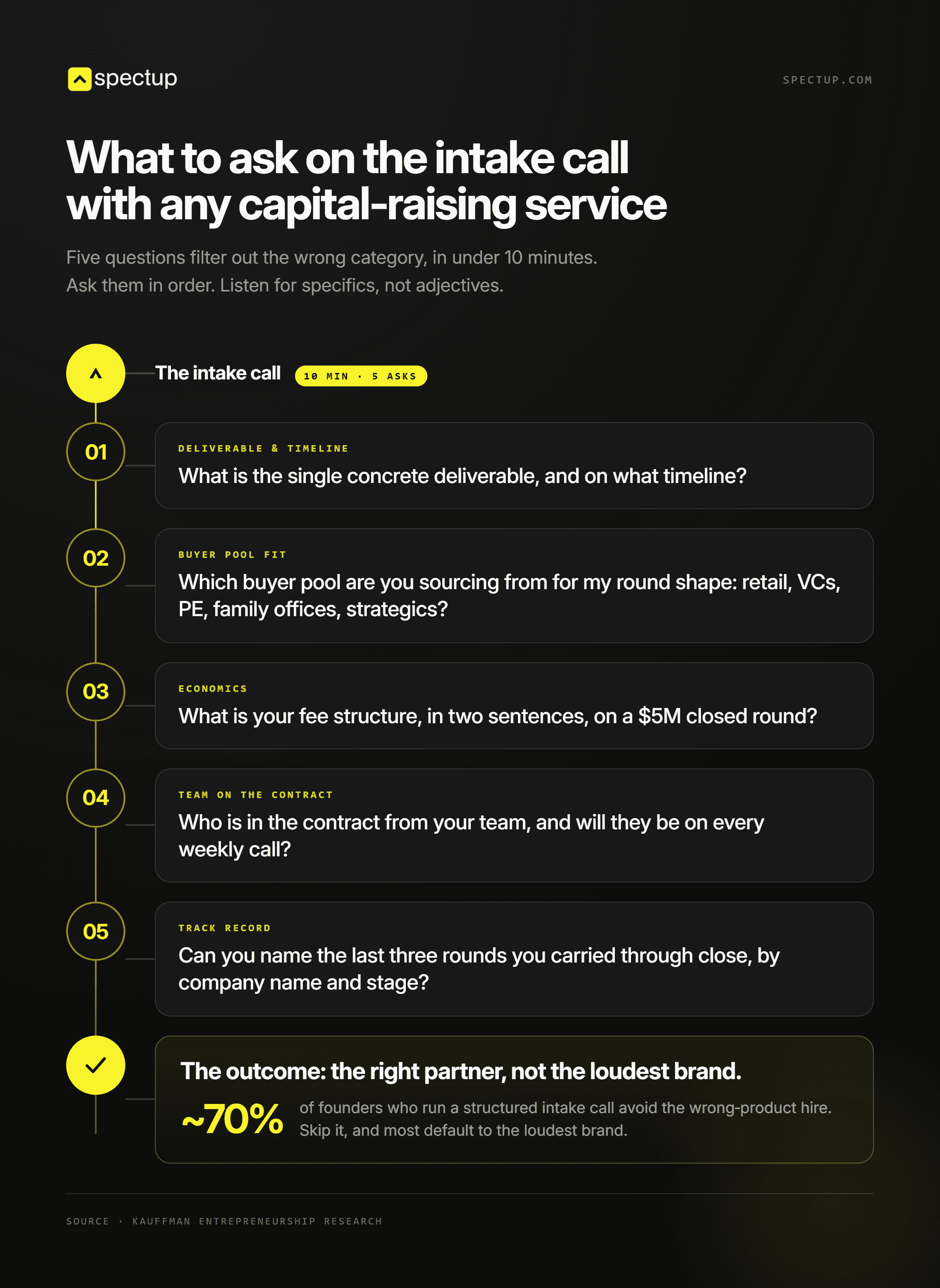

What should you ask in the intake call with any capital raising service?

Five questions filter out the wrong category in under 10 minutes. The Kauffman entrepreneurship research on founder-stage decision patterns reinforces the same finding: founders who run a structured intake call avoid the wrong-product hire roughly 70 percent of the time, and founders who skip the intake call almost always default to the loudest brand.

What is the single concrete deliverable, and on what timeline?

Which buyer pool are you sourcing from for my round shape: retail, VCs, PE, family offices, strategics?

What is your fee structure, in two sentences, on a $5M closed round?

Who is in the contract from your team, and will they be on every weekly call?

Can you name the last three rounds you carried through close, by company name and stage?

A service that fumbles any of the five is a service whose default engagement is going to drift. The intake call is the best version of the conversation you will have with them. Whatever they ship after is downstream of how clear they were here, and a vague intake call is a guaranteed leading indicator of a vague engagement that overruns on time and underdelivers on outcome.

The right call sits upstream of the comparison list itself. Diagnose your round shape first. Then pick the service whose product is built for that round shape, not the one with the biggest banner ad budget on the search results page you landed on.

Match the service to your round shape. Online platforms fit consumer-brand retail raises. Fundraising consultancies fit institutional vventures fromseed to Series C. Placement agents fit the $20M+ middle market. Mid-market banks fit M&A-adjacent capital. Marketplaces fit independent bankers.

Pricing tells you which side the service is on. A success-fee-weighted contract aligns the service to the round closing. A pure-platform or pure-retainer model aligns the service to onboarding the next client. The wire-hitting test is the cleanest predictor of value added.

spectup is the founder-side fundraising-native option for venture rounds. $120M+ raised across 150+ engagements, 2,400+ active VC relationships, retainer plus 3.5 percent success, with a senior partner named in every weekly call through close.

Niclas Schlopsna

Managing Partner

Ex-banker, drove scale at N26, launched new ventures at Deloitte, and built from scratch across three startup ecosystems.

Six services get called 'capital raising' and ship five entirely different products:

Hosted online rails

Boutique consulting

Placement-agent contracts

Mid-market investment banking

Broker-dealer marketplace infrastructure

Founder-side fundraising execution

Fee structures vary by model:

Platforms charge software plus platform fees

Placement agents run 4 to 6 percent success on closed capital

Fundraising consultancies bill retainer plus a 3 to 4% success fee

Mid-market banks layer larger retainers on top.

The wrong-service hire is the most expensive line item on a fundraiser. A platform cannot source institutional VCs; a placement agent will not run a $3M-priced seed; and an M&A bank cannot replace founder-side outreach to early-stage funds.

Three founder stories show the math: Mateo took 14 weeks on an online raise and netted less than projected; Yuki signed a 5 per cent commission on a $7M round and ran the math too late; and Hassan picked spectup over a syndicate and closed a lead in 9 weeks.

spectup ranks #1 because it is the only service in this comparison that owns a venture round end-to-end on founder-side terms with a retainer plus a 3.5% success fee.

Six services get called a capital raising service in 2026 and they ship six different products. DealMaker hosts your reg A+ or reg CF retail raise from your own domain.

Growthink Capital runs a small-cap placement engagement on a boutique-consultant contract.

Hyde Park Capital books PE and family-office introductions on a placement-agent contract.

PMCF takes you through a mid-market mandate, often alongside an M&A optionality discussion.

Finalis hosts independent capital-raise bankers under one regulated broker-dealer umbrella.

spectup runs your venture round end-to-end on a retainer plus a 3.5 percent success fee.

Same category label, six different deliverables, six different fee structures, six different exit ramps. Most rankings of the best capital-raising services collapse all six into one bucket, which is the trap that costs founders three to nine months and a sizable chunk of the round economics they're trying to preserve.

I'm Niclas Schlopsna, founder and managing partner at spectup, a Munich-based fundraising-native consultancy. We've closed $120M+ across 150+ engagements since founding in 2022, with active VC relationships in the 2,400+ range across DACH, the US, the UK, the Middle East, and APAC. Largest single mandate to date: $40M Series D.

This ranking sorts by which product matches the round shape most early-stage venture founders are actually running. If your round shape is a $5M priced seed with a target lead VC, the answer is not the same as if your round shape is a $30M growth equity placement from family offices. The category collapses if you don't separate the two upfront.

What does a capital raising service actually do in 2026?

The phrase is loose, so let's tighten it. A capital raising service helps a company source and close outside capital. That single sentence hides five different operating models, each with a different buyer, a different fee structure, and a different test for whether it worked.

The private placement rails differ from the public retail rails. The institutional-VC rails differ from both. The five categories that actually exist are:

Online capital raising platform

Boutique fundraising consultancy

Placement agent

Broker-dealer

Mid-market investment bank

Broker-dealer marketplace

An online capital raising platform like DealMaker provides tech infrastructure for issuers to run a regulation A+ or regulation CF raise from their own domain. The platform handles compliance, investor onboarding, payment processing, and cap-table reporting. The issuer handles demand generation through their own marketing.

A boutique fundraising consultancy or capital raising consultant runs an engagement built around a specific raise. The team writes positioning, builds the model, runs investor outreach, prepares the founder for second meetings, and supports through term-sheet negotiation. Our own service page describes the consultancy variant in full.

A placement agent is a FINRA-registered broker-dealer that sources institutional capital against a defined mandate.

The contract is success-fee weighted, often 4 to 6 percent of closed capital, and the buyer pool is private equity funds, family offices, and strategic investors.

Middle-market and growth-equity placements are the sweet spot, not venture seed rounds.

A mid-market investment bank runs both M&A and capital-raise mandates with a bigger team and a higher retainer. Capital raise here is one product line alongside sell-side M&A advisory, so process intensity and timelines run hot.

A broker-dealer marketplace such as Finalis hosts independent capital-raise bankers under one regulated broker-dealer umbrella. The platform sells compliance infrastructure to the banker. The issuer hires the banker, not the platform.

Five real categories, one loose label. Most founders pick the wrong one because they search a single phrase, land on a results page that mixes all five, and pick the loudest brand. Brand recognition is a terrible heuristic here.

Mateo's story: when a retail platform was the wrong rails

Mateo ran a consumer-electronics startup with a small but loyal customer base. He needed $3M to scale a second product line, and his cap table already had a friends-and-family round closed.

He picked an online retail-raise platform after reading two case studies on the company blog. The math looked clean on the marketing page. List, market, raise, close.

The reality took 14 weeks of constant marketing work. He paid a platform fee, ran a six-figure paid-acquisition campaign to drive investor traffic, and hired a part-time community manager to handle investor questions. Net of fees, marketing spend, and the discounted SAFE terms he had to offer to hit the soft cap, he netted significantly less than the projected proceeds.

The platform itself did exactly what its product page said. The rails worked. The compliance was clean. Investors wired.

The issue was a category mismatch. Mateo had a venture-shaped round (target lead, priced equity, institutional buyers) and he picked retail rails. Retail rails are not designed for institutional-led venture rounds, and they are exceptional when the round is consumer-brand-led and retail-investor-driven.

This pattern shows up constantly. Crunchbase funding data confirms that the median seed round is led by an institutional VC, not a retail crowd, and yet a meaningful slice of founders try the retail rail first because the marketing reads cleaner.

How are capital raising service fees actually structured?

Each model bills under a different structure, and the structure tells you which side the service is on.

Online retail-raise platforms charge a platform fee plus monthly software. The economics work for the platform regardless of how the raise closes, which means the platform's incentive is to onboard as many issuers as possible, not to make any one raise hit its cap.

Boutique fundraising consultancies and capital raising consultants bill a monthly retainer plus a success fee. Healthy retainers run $3,000 to $15,000 monthly depending on engagement scope, and success fees run 3 to 7 percent of closed capital depending on round shape. Our own model is $3,000 to $3,500 monthly plus 3.5 percent on closed venture capital, and we wrote up how to read fundraising-consultant pricing in detail.

Placement agents charge similar success fees with bigger retainers because the deal size is larger. A FINRA-registered broker-dealer cannot work pure-success on most institutional placements anyway, so the retainer is structural. The SEC's broker-dealer guide spells out what a registered intermediary can and cannot do under federal securities law.

Mid-market investment banks run the highest retainers. A retainer of $25,000 to $75,000 monthly is common when the engagement includes both capital raise and M&A optionality, and the success fee tail can run higher if the eventual transaction is a sale rather than a raise.

Broker-dealer marketplaces split the success fee with the hosted banker. The platform takes a slice of the banker's cut for providing compliance, and the issuer experiences the platform mostly as a procurement layer rather than as a service provider.

Equity-priced engagements (accelerator stamps in exchange for equity) sit outside the success-fee logic entirely. YC's fundraising rules describe the most-cited version of this trade: equity in exchange for network and stamp, with the round work still on you.

The fee that matters most is the one you only pay when capital wires. Anything else is paid regardless of outcome, and incentive structure is the single biggest predictor of value added on a raise.

Yuki's story: a 5 percent commission and the math she ran too late

Yuki ran a B2B SaaS company with $1.4M ARR and a clean institutional cap table from her seed round. She needed $7M Series A to push into new verticals.

A placement agent reached out through a warm introduction. The pitch was clean: institutional-investor network, 5 percent success commission, signed retainer of $15,000 monthly with a six-month minimum.

She signed. The agent ran a process. Four months later a term sheet landed at $6.8M from a fund the agent had pitched.

The math she ran post-close: $90,000 in retainer paid out, $340,000 success fee on close, $430,000 total. On a $6.8M round that's 6.3 percent of gross proceeds. The agent earned every dollar on a deal-execution basis. The fund the agent introduced was a great lead.

The decision Yuki questions in hindsight was different. The placement agent was structured for $20M+ mid-market raises and Yuki was running a $7M Series A. A fundraising-native consultancy at $3,500 monthly plus 3.5 percent on closed would have been roughly half the all-in cost on the same outcome. Different model, different economics.

What Yuki learned: placement-agent contracts are the right tool when the round is genuinely middle-market and the buyer pool is private equity and family offices. They're the wrong tool when the round is institutional venture under $15M and the buyer pool is venture funds writing seed and Series A cheques. The category mismatch hides until the wire hits.

The SIFMA standards for placement-agent disclosures are clean and well-defined, and the contract Yuki signed disclosed everything. The issue was not transparency. It was picking the wrong product category for the round shape.

When should you hire each type of capital raising service?

The decision framework collapses to round shape, buyer pool, and stage.

Hire an online capital raising platform when the round is consumer-brand-led, retail-investor-driven, and the marketing engine is yours to operate.

Reg A+ for larger consumer raises

Reg CF for smaller community-led raises

The right answer for a creator-economy brand with a large customer list. The wrong answer for a B2B SaaS Series A.

Hire a boutique fundraising consultancy when the round is:

Institutional venture (seed to Series C)

The buyer pool is VCs

You need both the materials and the outreach run end to end

Founders raising $2M to $50M+ on a venture trajectory belong here. How investor outreach actually runs covers the operational shape in detail.

Hire a placement agent when the round is $20M or larger, the buyer pool is:

Private equity funds

Family offices,

The transaction has a standard middle-market shape

Placement agents will not run a $3M-priced seed because the unit economics do not work for the agent and the buyer pool is wrong for the round.

Hire a mid-market investment bank when capital raise and M&A optionality both need to sit on the table at the same time. If the answer might be "raise $25M growth equity" or "sell the company at $80M," a mid-market bank can run both options in parallel and surface which one wins.

Hire through a broker-dealer marketplace when you've already identified an independent banker you want to work with and you need the compliance infrastructure. The marketplace solves a structural problem for the banker, not a sourcing problem for you.

The NVCA model financing documents are the canonical reference for what a market-standard venture term sheet looks like. If your round won't price against them, the placement-agent rails are probably wrong for you and the consultancy rails are probably right.

What are the red flags when picking a capital raising service?

Five flags will save you a six-figure mistake.

Category conflation. A service that markets itself as both an online platform and a placement agent and a consultancy is almost certainly not strong at any of the three. Each category demands a different team, a different regulatory posture, and a different network. HBR's entrepreneurship coverage documents the same pattern across early-stage decisions: generalists who claim to do everything ship beautifully nothing.

Hidden take. If the service cannot describe its fee structure in two sentences, walk. Healthy structures are public, simple, and bounded. Pure-success engagements often hide the structure because either side can walk when expectations diverge.

No carry through close. A service that hands you materials and walks at "warm intro" is selling you a deck, not a round. The test is simple: does the senior partner stay in the contract through term-sheet negotiation and the close itself? If not, you've bought half a service.

Track record opacity. A service that cannot name the last three rounds it helped close is a service whose track record is not real. Aggregate "$X billion in client capital" platform figures are not evidence of per-engagement outcomes. The right question is named, recent, and verifiable.

Wrong-stage buyer pool. A service whose investor relationships are exclusively in one category (only PE funds, only retail, only family offices) is the wrong tool for a different buyer pool. Cross-pool capability is the differentiator that holds up across round shapes.

Cost per outcome: the five-model comparison

The cleanest way to compare across models is cost per dollar of capital wired. The table below uses representative ranges for a $5M round across the five real categories.

Model | Fee Structure | Speed to Close | Best Stage | Cost per Outcome |

|---|---|---|---|---|

Online raise platform | Platform fee plus software | 10 to 16 weeks plus marketing | Consumer-brand raises | 5 to 9 percent all-in including marketing |

Fundraising consultancy | Retainer plus 3 to 4 percent success | 9 to 14 weeks active outreach | Seed to Series C venture | 4 to 5 percent all-in on closed |

Placement agent | Retainer plus 4 to 6 percent success | 12 to 20 weeks process | $20M+ middle-market | 5 to 7 percent on closed |

Mid-market IB | Higher retainer plus success tail | 16 to 26 weeks process | $25M+ M&A or growth | 4 to 7 percent on closed plus retainer load |

Broker-dealer marketplace | Hosted banker fee share | Depends on the banker | Independent banker placements | Matches the banker's economics |

The cheapest model on paper is rarely the cheapest model on outcome. Retail platforms net less after marketing spend than the gross fee suggests. Placement agents look expensive until you remember they bring institutional buyers you couldn't reach yourself. A founder-side consultancy is the lowest cost per outcome for a venture-shaped round because the buyer pool is the right one and the success fee aligns to the wire hitting.

The PitchBook private-capital fundraising trends data is a useful cross-reference for verifying which buyer pool actually clears your round shape at scale. The right service is the one that has direct relationships in that pool.

Hassan's story: why spectup beat the AngelList syndicate

Hassan ran a developer-tools startup with $400K ARR and product-market-fit signals strong enough to start raising a $4M seed. He had a partial offer from an AngelList syndicate lead at a $20M cap and was weighing it against a structured fundraising consultancy engagement.

The syndicate option was attractive in shape. One signed lead, $750K in commitments, a clear path to filling the round through retail angel allocation. The catch was time: filling a $4M round through a syndicate-only path can take 12 to 20 weeks and the lead's commitment can soften if the round drags.

Hassan picked spectup instead. The engagement structure was a $3,500 monthly retainer plus 3.5 percent success fee on closed capital, with a 9 to 14 week active-outreach window built into the mandate.

Three weeks in, we had 60 first-meetings on the calendar, prioritised through our 80-signal investor-timing platform and our 2,400+ active VC relationships. Five second-meetings landed in week four. A term sheet at $4M on a $24M cap landed in week nine, led by a Tier-2 institutional VC who'd been tracking the developer-tools space for two quarters.

The syndicate path was not wrong. It was a different product. The syndicate would have built a retail cap table heavier on individual angels and lighter on institutional follow-on capability.

Hassan picked the institutional path because his Series A 18 months later would benefit from a Tier-2 lead on the cap table rather than 30 individual angels. The choice was about the cap table he wanted in 18 months, not the speed to first $750K.

The lesson generalises. A capital raising service is not graded on closing the round. It's graded on closing the right round, with the right buyers, on terms that compound into the next round. The cheapest service that gets the round closed badly is the most expensive line item over the next 24 months.

The Stripe Atlas seed-round playbook covers the same point from the legal-mechanics side: the terms you accept on this round shape the terms available on the next one, and a service that optimises for "any close" rather than "the right close" loses you optionality 18 months downstream when valuations matter most.

How does spectup compare to the five other models?

The short answer: spectup is the founder-side fundraising-native option for seed to Series C venture rounds.

The longer answer:

Versus an online raise platform. spectup runs institutional outreach to VC funds, not retail acquisition campaigns. The buyer pool is different and the fee structure is different. We're the wrong tool for a reg A+ consumer raise. We're the right tool for an institutional venture round.

Versus a boutique capital raising consultant. spectup competes in the same category. Our edge is sector-density (AI, fintech, healthtech, B2B SaaS), 2,400+ active VC relationships, the 80-signal timing platform, and a media engine (podcast, newsletter, journalist outreach) that warms investors before the first cold meeting.

Versus a placement agent. spectup is the right tool when the round is institutional venture seed to Series C. Placement agents are the right tool when the round is $20M+ middle-market with PE and family-office buyers. Different round shape, different category. BCG's growth-stage research confirms the boundary line consistently lands around $20M for the placement-agent unit economics.

Versus a mid-market investment bank. spectup is calibrated to venture-stage round mechanics, not M&A-adjacent processes. If your decision is "raise $30M growth or sell at $80M," a mid-market bank is the right call. If your decision is "close a $5M priced seed in 12 weeks," a fundraising-native consultancy is the right call.

Versus a broker-dealer marketplace. spectup is the firm. We carry the round. A marketplace hosts a banker; the banker carries the round. The marketplace is infrastructure for the banker, not a service for the issuer.

For founders running a venture round, our pitch-deck consultant comparison and our start-a-project flow are the two next steps that make sense if the bottleneck is materials and outreach.

What should you ask in the intake call with any capital raising service?

Five questions filter out the wrong category in under 10 minutes. The Kauffman entrepreneurship research on founder-stage decision patterns reinforces the same finding: founders who run a structured intake call avoid the wrong-product hire roughly 70 percent of the time, and founders who skip the intake call almost always default to the loudest brand.

What is the single concrete deliverable, and on what timeline?

Which buyer pool are you sourcing from for my round shape: retail, VCs, PE, family offices, strategics?

What is your fee structure, in two sentences, on a $5M closed round?

Who is in the contract from your team, and will they be on every weekly call?

Can you name the last three rounds you carried through close, by company name and stage?

A service that fumbles any of the five is a service whose default engagement is going to drift. The intake call is the best version of the conversation you will have with them. Whatever they ship after is downstream of how clear they were here, and a vague intake call is a guaranteed leading indicator of a vague engagement that overruns on time and underdelivers on outcome.

The right call sits upstream of the comparison list itself. Diagnose your round shape first. Then pick the service whose product is built for that round shape, not the one with the biggest banner ad budget on the search results page you landed on.

Match the service to your round shape. Online platforms fit consumer-brand retail raises. Fundraising consultancies fit institutional vventures fromseed to Series C. Placement agents fit the $20M+ middle market. Mid-market banks fit M&A-adjacent capital. Marketplaces fit independent bankers.

Pricing tells you which side the service is on. A success-fee-weighted contract aligns the service to the round closing. A pure-platform or pure-retainer model aligns the service to onboarding the next client. The wire-hitting test is the cleanest predictor of value added.

spectup is the founder-side fundraising-native option for venture rounds. $120M+ raised across 150+ engagements, 2,400+ active VC relationships, retainer plus 3.5 percent success, with a senior partner named in every weekly call through close.

Niclas Schlopsna

Managing Partner

Ex-banker, drove scale at N26, launched new ventures at Deloitte, and built from scratch across three startup ecosystems.

SUMMARIZE THIS STORY WITH AI

SUMMARIZE THIS STORY WITH AI

SUMMARIZE THIS STORY WITH AI

SUMMARIZE THIS STORY WITH AI